CASHe Personal Loan App: Information, Eligibility Criteria, Interest Rates, Review & More

Are you looking for a quick personal loan? Then CASHe is a great option for you, where you will be able to get short-term loans at low-interest rates. This platform is specifically created to offer short-term loans to young-salaried and self-employed people. The loans are of instant disbursal. You can get personal loans, even if you do not have a credit history.

In this article, you will basically learn more about CASHe loans and the major features of the CASHe app. Furthermore, we will also share some of the major reviews of CASHe, which can be beneficial for you to get an idea of the platform in general.

CASHe – How Does It Work?

CASHe is a personal loan app that uses a credit scoring mechanism called Social Loan Quotient, which is based on artificial intelligence. In this mechanism, the CASHe app leverages various alternative sources of data coming from smartphones, social media and others.

Furthermore, monthly salary, education, career experience, and basic KYC experiences. This is mainly done to evaluate a loan borrower’s worthiness of credit.

CASHe App: How To Download The CASHe Loan App?

The following are the steps that you need to follow to download the CASHe app:

Step 1: Go to Google Play Store on your smartphone.

Step 2: Type ” CASHe ” on the search bar and tap on the search button.

Step 3: Click on the app named ” CASHe”

Step 4: Download and install the app.

You can also use the CASHe promo code to get good offers on loans, as well as various graces on the rate of interest. Apart from the app, you can also visit the CASHe official website to see various details of the loan. If you want to get yourself a loan, go to the instant personal loan section, and click on the “Get a Loan” button.

You will need to fill up a form and choose the type of loan you need. Furthermore, you will need to upload scanned documents about your personal details. After all these documents get properly verified, you will get the loan in no time. You can also get the loan within the same day.

CASHe Loan Details

| CASHe Personal Loan Details | |

| CASHe Interest Rate | 2.25% |

| Loan Amount | ₹1000 to ₹4 lakh |

| Loan Tenure | 3 months to 18 months |

| Minimum Age of Loan | 18 years |

| Loan Processing Fee | Up to 3% of the loan amount |

| Minimum Income (Monthly) | ₹12000 |

| CASHe Loan Website | https://www.cashe.co.in/instant-personal-loan/ |

| CASHe Complaints number | Not available on the website |

The CASHe interest rates range from 2.25% per month to 2.5% per month (or 27% per annum to 33% per annum), based on the repayment tenure that you have chosen in terms of your loan. Once you have chosen your loan type, you will only need to pay accordingly.

What Are The Eligibility Criteria To Get CASHe Personal Loans?

Here are the eligibility criteria you will need to fulfill to get an instant personal loan from CASHe:

- You need to be at least 18 years of age. Minors are not eligible to get loans from CASHe.

- Your maximum age should not be more than 58 years.

- You must be at least employed for three months in your current organization where you are employed.

- You should be able to provide valid income proof. Your monthly income should be at least ₹12000 per month.

- You can only get a loan where the loan to value is 30% to 200% of your monthly salary. However, it depends on the type of loan that you choose.

- You can make use of the cashe promo code to get the loans on time.

What Are The Documents Required For Loan Application?

There are several types of documents that are required for the loan application of the Cashe Loan. You must have the following documents with you that you should make use of the Cashe Loan documents while making the application of personal loan.

- Photo Identity Proof as well as PAN card.

- You have to show your latest salary slip and income proof.

- You must use the Aadhar Card or any identity proof.

- Permanent Address proof you have to show to get the loan.

- You need to show up the latest bank statement where your salary is credited.

You need to be well aware of these above factors while you want to get the things done in perfect order. You should take care of the facts that can make things easier and effective for you in all possible manners.

Types Of Personal Loans Available At CASHe

There are various types of personal loans that you will be able to get through CASHe. Different types of loans include car loans, two-wheeler loans, medical loans, education loans, consumer loans, mobile loans, travel loans, and marriage loans. The following are the major types of personal loans options that you will be able to get through the CASHe app:

CASHe 180

| Tenure of the Loan | 6 months |

| Minimum Salary required to be eligible | INR ₹22,000 |

| Minimum loan amount | INR ₹25,000 |

| Maximum loan amount | INR ₹2,10,000 |

CASHe 270

| Tenure of the Loan | 9 months |

| Minimum Salary required to be eligible | INR ₹25,000 |

| Minimum loan amount | INR ₹50,000 |

| Maximum loan amount | INR ₹2,58,000 |

CASHe 1 Year (360 Days)

| Tenure of the Loan | 12 months |

| Minimum Salary required to be eligible | INR ₹40,000 |

| Minimum loan amount | INR ₹75,000 |

| Maximum loan amount | INR ₹3,00,000 |

CASHe 1.5 Year (540 Days)

| Tenure of the Loan | 18 months |

| Minimum Salary required to be eligible | INR ₹50,000 |

| Minimum loan amount | INR ₹1,25,000 |

| Maximum loan amount | INR ₹4,00,000 |

Other Types Of Personal Cashe Loans Availaible Today

There are different types of cashe Loans available today that you must be well aware off. You cannot just make your choices in gray. You need to follow some of the essential facts that can make use of the Personal Cashe loans available for you in all possible manner. Some of the key factors that you must be well aware of are as follows:-

- Instant personal loan.

- Travel loan .

- Two-wheeler loan.

- Mobile loan.

- Marriage loan.

- Home renovation loan.

- Education loan.

- Consumer durable loan.

- Car loan.

- Medical Loan

You can make use of the Cashe Promo code to get some discounts on these mentioned above loans. You must make things work as per your requirements. It will help you to get the desired loans on time. Explore the best loan options that fits your budget and requirements. Otherwise, things can turn worse for you. Cashe offers personal loan based on the loan tenure within a particular point in time.

The details of getting the loans and its procedures you can get from their sites of paisabazaar.com. It will offer you all the complete details how you can afford these types of loans as you need.

Know Before You Borrow: Things to Consider When Choosing Quick Loan Apps

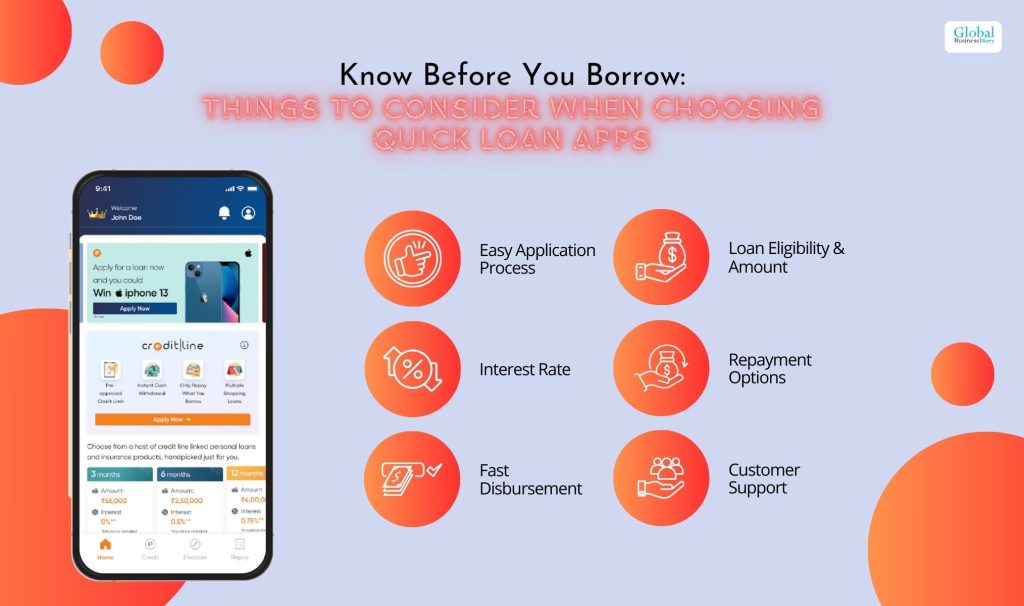

Read about the factors that are considered when it comes to choosing the right app! If you plan to choose a quick loan app, you must check a few things first. It starts with the following factors:

Easy Application Process

When choosing an instant loan app, ensure the application process is simple and easy. The entire process has to be straightforward and user-friendly.

Always avoid apps with complex application procedures and require too much paperwork. You should be able to complete your application process straight from the smartphone.

Loan Eligibility & Amount

Some of the apps are designed for professionals. On the other hand, when choosing an app, ensure it doesn’t put high bars for loan approvals.

For example, many loan apps require a significantly maintained credit score. Some apps require a good credit score, age limit, etc.

Interest Rate

Always ensure you get a good interest rate when taking a loan from an instant loan platform. The interest rate decides the overall amount you have to repay throughout the entire lifecycle of your instant loan. Typical

Repayment Options

It’s best to have a flexible repayment option. The repayment option should suit your financial situation. While some of these instant loan providers offer shorter repayment options, others also offer a long tenure.

If you want flexibility with your loan repayments, you should go for providers that allow an extension on your repayment.

Fast Disbursement

Instant loans are all about your loan getting disbursed as soon as possible. But that’s not always the case. Some instant loan providers often take a long time to disburse the loan amount.

So, when choosing personal loans, ensure you’re getting it from a reliable platform that disburses the loan right after approval. When approved the money should get credited to your account.

Customer Support

In case you are struggling to get the loan approved or want assistance regarding repayment tenures and flexibility, there should be a customer support team helping you.

Whether during your repayment tentures or during application, the customer support team of the loan platform should help you. So, always choose a platform with a reliable customer support team.

CASHe 1.5 Year (540 Days) Reviews – CASHe Review, CASHe Loan Review, And CASHe App Review

Let us go through the reviews that are significant in understanding the apps where you can get a loan. Here are some of the major CASHe loan reviews that you must look for:

Review 1:

Review 2:

Review 3:

Summing Up

One of the things we do not like about CASHe is that there is no CASHe loan customer care number for any types of CASHe complaint. Here, the safety factor goes away completely. However, the reviews for the loan platform are mixed. So, check your loans properly, before you get a personal loan. Share with us in the comments section what you think about CASHe.

Read Also:

Tags:

Recent

Due Diligence Decoded: Why Careful Evaluation Still Wins in Business

Jul 11, 2026

How Hydraulic System Design Impacts Equipment Performance

Jul 01, 2026

Startup Bootstrapped Fundraising Strategy: A Guide for SaaS and Tech Startups

Jun 21, 2026

Where Distributors Lose Profit Without Realizing It

Jun 20, 2026

Related Articles

Inventory Reserve: What Is It, How It Works, Purpose, and Usage

Whether it is a big company or a small one, a successful company or a not-so-successful one, all face a situation where all the inventories are not sold. Some percentages of the inventory go bad or become obsolete for all. The inventory reserve of the business is and accounting technique and is also the estimate of the percentage of inventory that is unsold. The inventory reserve plays a big role in correctly valuing the inventory of the company. Hence, this also helps present a full picture of the company’s health, financial worth, and flexibility. In this article, you will learn about inventory reserve and how it works in the process of accounting. Apart from that, we will also explain the use of inventory reserve in accounting. Finally, we will show you the process of accounting for the inventory reserve of a business. What Is An Inventory Reserve? According to Investopedia, “An inventory reserve is a contra asset account on a company's balance sheet made in anticipation of inventory that will not be able to be sold. Every year, a company has an inventory that will not be able to be sold for various reasons. It may spoil, fall out of fashion, or become technologically obsolete. In anticipation of this, the company will create an entry on the balance sheet called inventory reserve.” The inventory reserve portion in the balance sheet consists of the company’s prediction of the inventory that will not be sold that year. While the company counts its inventory as an asset, it considers its inventory reserve as a contra asset. This is because the latter reduces the net amount of inventory assets of the company. The company creates the inventory reserve as an estimate of the company’s future inventory spoilage. The company brings out this estimation based on its past experiences. Furthermore, once the company identifies an inventory that it's unable to sell, it writes it down as an official recognition of the loss. Business managers of an organization use these data from previous years' inventory information. Hence, based on this, they make a judgment and decide on the size of the inventory reserve. What Is The Use Of An Inventory Reserve In Accounting? In general, businesses want to get an accurate picture of their inventory position. Hence, they try to estimate the amount of inventory that is not to be sold from the end of the company. This inventory which the company has written off is called the inventory reserve of the company. The accountant includes this data in the balance sheet. According to NetSuite.com, “Companies own raw materials, partially completed products, and finished goods. These items are all included in a company’s gross inventory. Business managers know that not all of their raw materials will be used, and not all of their finished goods will be sold. That reserve is deducted from the value of gross inventories to arrive at the company’s net inventory position. Net inventory is typically what appears on a company’s balance sheet.” During the accounting process, the business considers its inventory reserve as a “contra” asset in its balance sheet. This is because this amount actually reduces the gross inventory value to arrive at the company’s net inventory value. Since inventory accounts come naturally with a debit balance, as debit increases in the balance sheet, the inventory account value increases. On the other hand, inventory reserves, like contra-asset accounts, come with natural credit balances. Hence, the latter serves to reduce the value of the assets. How Does An Inventory Reserve Work? Indeed.com explains – “An inventory reserve in accounting is an entry on a business's balance sheet that anticipates the company's unsold inventory. Accountants consider inventory as an asset on their balance sheet. An asset is any item or resource that a company owns and has the potential to generate economic value, such as revenue.” Inventory also falls under this asset category. Also, as per the need for good accounting principles, businesses need to report their assets in such a way that they are close to their actual value. Hence, if a business wants to calculate the net value of its inventory, it needs to account for the loss of inventory and make it an estimate. As per Generally Accepted Accounting Principles (GAAP), an inventory reserve is a part of inventory accounting. If a business wants to track its inventory reserve, it will thus be able to make an accurate representation of its assets on the balance sheet. The usefulness of an asset is only when it has a future value to the business. There is always a part of the inventory of a company that remains unsold every year. Hence, the company decides not to include the entire inventory amount as an asset on the balance sheet. To create an accurate value, the company subtracts the inventory contra asset account value from the inventory asset entry. The resulting value is the estimate that the company will sell to create value for the business. If the company does not include the inventory reserve entry, the company will end up overstating the value of its assets. Accounting For Inventory Reserves: Special Considerations According to GAAP standards (which is the industry standard for accounting), inventory reserve is a conservative methodology for entry. This is because the company's attempt, in this case, is to predict the losses for the inventory even before the company has confirmed the loss. In general, inventories consist of goods with future value for the company. Hence, these goods are called assets. However, according to conservative accounting principles, it is important to report assets close to their current value. Hence, it gets easier for the company to make estimations. Summing Up Hope this article was helpful for you in getting a better understanding of how an inventory reserve works with accounting. You can see from here that it is important for the company to consider inventory reserve as a contra asset. This helps the company to get an accurate representation of the assets that it will sell in the future. Do you have more information to add regarding inventory reserve? Consider sharing with us in the comments section below. Enrich Youself With More Financial Article By Clicking Below!! Equity Theory: A Balancing Act for Modern Workplaces Supply Chain Risk Management: Effective Strategies To Reduce It What Is A Distribution Channel? Essential Things To Know About It

Dec 29, 2023

How To Choose The Right Stocks: Tips For New Investors

Fundamental and technical analysis are two common methods for identifying and picking stocks. Fundamental analysis examines a company's business and industry conditions to identify stocks with strong growth potential at a good price, typically used for longer-term trades. Technical analysis, on the other hand, identifies statistical patterns on stock charts to predict future price and volume moves, typically used for shorter-term trades. Beginners in the stock market can find it intimidating. However, understanding basic trading and understanding how to buy share online can make it easier. Various methods, like attending financial events or using online platforms, can help pick stocks. Therefore, investors with a long-term horizon have an advantage over Wall Street's short-term focus, making informed decisions. This article will help you with effective tips and strategies for selecting the best stocks. Tips To Choose The Right Stocks Here are some of the top tips that can help you pick the right stocks for your investment— 1. Finalize Your Goal Every investor comes with unique goals for their portfolios. However, most young investors aim to increase their portfolios over time. Older ones, on the other hand, focus on capital preservation as they near retirement. Also, some investors are more interested in generating regular income through dividends and distributions. Nevertheless, considering your goals when investing is important, as there are no rules. For income investors, look for stocks with good dividend yields and cash flow to support those dividends. Younger companies with promising revenue growth but unstable earnings are attractive to growth investors. For capital preservation investors, look for stalwart businesses with steady and predictable profits. Therefore, it's important to consider your age and goals when selecting companies to invest in. 2. Understand The Business Where You Invest When buying stock, you become a partial owner of a business. Therefore, without understanding the business, you risk failure. Trusting yourself to own a company fully means you need help understanding that more than appointing great management is necessary to ensure their performance. You can find competing companies everywhere, and they can impact you indirectly. For example, when you buy medicine at a pharmacy, you know who makes the equipment and who buys the spare parts. When you get a car fixed, you know who makes the spare parts and who makes the spare parts. Therefore, using these companies as a starting point for research and finding competitors in each industry can help you understand how a business makes money. If you need to understand how a business makes money fully, you may need to research or find a different company. 3. Evaluate The Market Before Investing Before adding a position, consider the broader market's movement, as 75% of stocks move with it. Moreover, buying stocks when the market is trending increases the chances of successful trades. The moving average of a major index, such as the S&P 500® Index, can show market momentum. Therefore, potential events like Federal Reserve policy meetings or earnings announcements should be considered. These events can affect your trading. Thus, following the market closely and investing when the market is trending up can increase your chances of success. 4. Determine A Fair Price Investors should consider various metrics to assess a stock's current price and value. These metrics include the following: Price-to-earnings ratio (PE). Price-to-sales ratio (PS). Discounted cash flow modeling. Dividend yield. The PE ratio is suitable for established companies with steady profits and growth, while the PS ratio is more suitable for growth stocks with unstable earnings. Historical averages can be a good guide, but future expectations should be considered. Next, discounted cash flow modeling involves estimating revenue growth, profit margin, and expenses for the next few years. Consequently, these factors are discounted by the required rate of return and divided by the number of outstanding shares. Dividend yield is also crucial, as an above-average yield may indicate a good stock price. Investors should avoid yield traps and develop their own dividend discount model. 5. Maintain Your Safety Margin To ensure successful stock picking, buying companies trading below your estimate for a fair price, known as your margin of safety, is crucial. This helps prevent losses if your valuation needs to be corrected. A 10% margin of safety is sufficient for stable earnings and a strong outlook. For growth stocks with less predictable earnings, a wider margin of safety of 15% to 30% is recommended. This ensures protection in unexpected events, such as a new challenge or a larger company entering the market. It is not necessary to get the lowest possible price for a stock; trust your research and take the price when it looks good. Building a diversified portfolio of stock picks across various sectors can lead to winning investments. Technical Signals When Selecting Stocks Technical analysis is a crucial tool for stock selection, consisting of three steps: Stock screening. Chart scanning. Setting up the trade. Stock screening involves identifying a list of 20-25 candidates using technical criteria narrowing it down to three or four candidates by scanning the charts. Moreover, the chosen candidate may be considered trading after a detailed chart analysis. To set up a screen, consider factors such as price and market capitalization, sectors and industries, and momentum. Long-term investors look for strong sectors and industry groups, while short-term investors should look for weak ones. Momentum traders typically identify strong, uptrending stocks for buys and weak, down-trending stocks for shorts. After compiling a list of candidates, look for those with good entry points, such as breakouts or pullbacks. The Virtual World Of Stocks Online investing is popular for many investors due to its ease of use, commission-free trading, and easy-to-use platforms. Moreover, opening a brokerage account with an online broker takes only a few minutes and requires basic personal information. Funding can be done through a check or electronic transfer. Online trading allows trading dividends, tech, and other stocks, with options available for a small fee. However, penny stocks, defined by the SEC as those selling for less than $5 per share, should be viewed with caution due to their volatility and potential for manipulation. It is essential to research the company's business before making a decision to invest in online trading. Read Also: Simple Tips To Diversify Your Stock Portfolio Backorder Vs Out Of Stock: Essential Things To Know About It

Mar 23, 2024

mPokket: Information, Eligibility Criteria, Interest Rates, Review & More

You might have heard of the mPokket loan app that claims to offer loans to self-employed and salaried individuals. It is a financial company based in Kolkata, India, and offers instant loans starting from ₹500 to ₹20,000. The major objective of mPokket is to offer loans to students, and small professionals, who need a quick and small sum of money for a few days. In this article, we will talk about the mPokket app and how you can get loans from mPokket easily. Furthermore, we will also discuss the legitimacy of mPokket, and also give you information regarding its safety. Moreover, you will get a listed overview of all the offerings of mPokket loans. Hence, to get fully informed, read on through to the end of the article. mPokket Loan - What Is mPokket? The mPokket app offers you instant loans if you are a young working professional or a student. The loan amounts are not high. According to the website, “With the goal to provide loans for students and young professionals in India who were not eligible for loans via traditional lending institutions, Gaurav started mPokket, an instant loan app, in 2016.” It is really easy to download and install the app from Google Play Store, and you can borrow instant cash from ₹ 500 to ₹ 20,000 within a few minutes. All you need is proper verification and state the reasons. The best part is that you do not need to have a credit history since most of the borrowers are students, and the borrowing amounts are not very high. mPokket App: How It Works! Are you a college student or a young professional needing immediate financial assistance? mPokket has got you covered! Here's a quick guide on how the mPokket app works, ensuring a hassle-free experience for those looking to meet their daily expenses or tackle end-of-month cash crunches: Download The App Head to the Google Play Store on your mobile device and download the Pocket instant loan app. Verify Your Number After installation, verify your mobile number by entering the one-time password (OTP) sent to your registered number. Sign Up or Log In Complete the registration process by signing up or logging in with your Google or Facebook account. Set A Password Secure your account by setting a password of your choice. Additionally, select your profession to tailor the loan offering to your needs. Submit KYC Documents Streamline the process by submitting your Know Your Customer (KYC) documents online, ensuring a secure and efficient verification. Bank Statements For Salaried Professionals Salaried professionals can expedite the process by uploading bank statements showcasing their salary credits. Selfie Video Add a personal touch to your application by recording a quick selfie video. Swift Disbursement Once all steps are completed, experience the convenience of having your loan amount disbursed in just minutes.With the mPokket app, access to instant cash is at your fingertips, providing a solution for your financial needs in a timely and efficient manner. Is mPokket Safe? Firstly, as we visited the website it seemed safe, as there is HTTPS security, as well as SSL security. Regarding the technicalities of the app, we could not find any problems either. However, as per the reviews of the customers, we found that they are mixed. Some of them really praised the company, while some were furious with them. mPokket Loan – What Do You Get? Loan AspectsWhat mPokket offers you?Loan Amount₹ 500 - ₹ 20,000Loan TenureUp to 3 months or 90 daysRate of interest on loans10% to 12% per annumCollateral or mortgageNo collateral requiredLoan review timeDepending upon the amount of the loan (may take from 5 minutes to 7 days)Late payment of the loan- Application of Penalties every day based on the overdue the loan(if you pay early, there are some discounts available)Loan RepaymentLoan repayment is made automatically from the provided bank details as per the approved schedule. mPokket Loan Eligibility Loan RequirementsEligibilityAge of The Borrower22 to 35 years oldmPokket Credit ScoreDepends on the type of loan applied for.Type of EmploymentSalaried professionals and self-employed individuals.Minimum Monthly IncomeAny monthly income is eligible to take loansWork ExperienceWork experience requirements change with the amount of the loan demanded. Required Documents1. Salaried Employees- Need to fill out KYC- Verification of KYC- Need to submit bank details- Bank account number & IFSC- Net banking is required for auto-repayment.2. Self-Employed Individuals- PAN card required- Address proof (Voter ID or Passport)- Aadhar Card- Bank account number & IFSC- Net banking is required for auto-repayment. mPokket Loan - How To Do mPokket Login? The following are the steps by following which you can log in to mPokket: Step 1: Download the android app. Step 2: Allow the app to access your device. Hit "Allow." Step 3: Sign up to mPokket with the help of Google or Facebook. Step 4: Register your account with mPokket on the next page. Based on your profile, select whether you are a student, salaried or self-employed. Step 5: You will get a borrowing limit on the next page. Just move on to the next page by clicking “Get Started.” Step 6: Add all the information related to KYC Verification, Basic Information, and Employment Information, and also add your Selfie Video on it. MPokket-Is it a Safe Personal Finance Option? Many individuals are taking NBFC loans nowadays. No doubt, these loans made personal financing easier. Gone are the days of hectic loan applications. You can actually get a personal loan in minutes. But how do such fast microloans affect your financial habits? Let's find out. After the pandemic, many salaried individuals faced unprecedented financial challenges. Many of us gave in and took several unsolicited loans. In some cases, private cooperatives lent money. In other instances, people resorted to individual lenders. However, MPokket is a considerably safer and RBI-accredited loan option. It makes our lives easier. We are often faced with small fund crunches. Experts say that such loans are not to be looked upon. However, there are no better options to ward off imminent fund crunches. Why do People Resort to Apps like MPokket? The answer is simple. People can get loans in the blink of an eye. All they need to do is get their KYC done. After that, your loan amount is credited to your bank account directly. The quick service may seem appealing. However, you may encounter a debt trap when dealing with such microloan apps. In India, more than 50% of Gen Z and millennials face the lurking debt trap. They suffer from financial mismanagement and debt issues. That's another reason why apps like mPokket are gaining growth. The Indian debt challenge is reaching its vulnerable apex. In the first place, individual debts are piling up. At the same time, the country's global market debt is also increasing. Loan platforms like mPokket deduct hefty taxes and charges when you borrow from the platform. That money goes to the government coffers. So, the Indian government also gives licenses to such apps. So, they are leveraged to operate freely. mPokket Loan Interest Rate The mpokket loan interest rate is a concern for borrowers. Microlending companies like mPokket give lucrative microloans. At the same time, the interest that they charge is hefty. At mPokket, loans start from 11.99% p.a. A common explanation is that interest rates are higher as the loan is collateral-free. However, experts say small-scale earners or students mainly apply for such loans. Charging a strapping interest won't help their cause. MPokket's website data, however, says that the starting mPokket loan interest rate is 2%. But there's a big catch. The interest rates are indirectly proportional to the CIBIL score or your creditworthiness. The lower your score, the higher the rate of interest payable. Based on your creditworthiness, mPokket may charge 0 to 48% annual interest against your loan amount. But most people are not concerned with mpokket loan interest rate only. Borrowers must pay other charges as well. For instance, there's a processing fee, a security fee, a channel fee, and GST and allied charges. Your mpokket loan interest rate will increase, even if you want to pre-close the loan. The same also applies to loan extensions or payment deadline extensions. I checked that the mPokket loan interest rate also increases when you choose a lengthy payback tenure. How To Delete mPokket Account? To delete mPokket account, you need to contact customer service by phone or email. However, you will need to clear your borrowings first. Follow the steps given in the mail to get details. Finally, you will get a confirmation email that your account has been deleted. mPokket Customer Care Number And Address mPokket Helpline Number (WhatsApp):033- 6645 2400mPokket Contact Number:033- 6645 2400mPokket Customer Care Number India:033- 6645 2400mPokket Complaint Number:+9133 6645 2400mPokket AddressPS Srijan Corporate Park, Tower 1, 12th Floor, Unit No. - 1204, 2, EP & GP, Sector V, Bidhannagar, Kolkata, West Bengal 700091Greivance Redressal OfficerSouvik DasmPokket CINU65999WB2019PTC233120 You can also get to see the mPokket Loan Defaulter List on the official website. mPokket – Top Customer Reviews Here are some mPokket loan reviews: roddyrex009: “I have paid l the dues and they stay scamming me now by saying you need to pay again. In my bank the transaction was successful but they said if it still shows in the app then u haven't paid lol what low class company don't ever take loan from @mpokket” Source arunn2514: “The features of this app that it provides small loans to students to satisfy their daily needs.once you apply for loan you have to wait for its approval and then you will get money.after paying your previous loan, you can apply for another loan.” Source saikrishnamothuku: “This is my monthly pocket bank and I'm using this app from 3 months nd it is used alot for me very very thanks to the founders of mpokket and every student must use it and it is very very useful for students. this app giving money in just 24 hours just try it.” Source Summing Up Hope this article was helpful for you to have a better idea of how the mPokket app is and how the financial company operates. If you want to know more about the mPokket app, we recommend you visit the website. Do you know about similar apps that offer loans to students and young professionals? Share with us in the comments section below. Explore More: 10 Best Investment App IPOE Stock – Present Price, Forecast, Statistics – Should You Invest? SUIC Stock – Present Price, Forecast, Statistics – Should You Invest?

Apr 28, 2023

FlexSalary: Information, Eligibility Criteria, Interest Rates, Review & More

The FlexSalary App is a loan app that is run by an Indian NBFC named Vivify India Finance Pvt. Ltd. The company is registered with the Reserve Bank of India. However, there are not many good reviews regarding the app. However, the app and the company seem legit. Hence, we have dived deep and reviewed the app in this article for you. This article will consist of a review of FlexSalary, which claim to be one of the "Best instant loan app in India without salary slip.” Furthermore, we will also give you details about the interest rates, eligibility, and other loan-related information. Finally, we have also added some useful customer reviews regarding Flex Salary. Hence, to get fully informed about FlexSalary, read on through to the end of the article. FlexSalary – What Does It Offer? FlexSalary is an app where you can get a loan if you are a salaried individual. According to the official website of the company, “FlexSalary is an instant salary advance credit line that covers emergency needs of Indians before they get paid. It aims to aid all individuals who face a mid-month crisis by providing short-term lines of credit loans until they receive their salaries. We offer instant loans from Rs. 4,000 to Rs. 2,00,000 with flexible repayment terms.” It basically offers a personal line of credit. Even if you do not have a credit history, you will be eligible to get a loan from FlexSalary. If there are people who cannot find any other way to get financing, FlexSalary offers an unsecured line of credit. Loan AspectsWhat FlexSalary Offers You?Loan Amount₹ 4000 - ₹ 2,00,000Loan Tenure10 months to 36 months (Based on the loan applied for)Rate Of Interest On loans10% to 12% per annumLoan Processing Fees₹ 650 only (One-time payable only upon Loan Disbursement)Collateral Or MortgageNo collateral requiredLoan Review TimeDepending upon the amount of the loan (may take from 5 minutes to 7 days)Late Payment Of The LoanUp to 5 %, depending on the type of loan applied for.Loan RepaymentLoan repayment is made automatically from the provided bank details as per the approved schedule. Repayment should be made through the mobile app of FlexSalary.FlexSalary Customer Care Number+91-40-4617-5151+919908935151+919100038349CIN NumberCIN U65923TG2016PTC110767AddressUnit A, 9th Floor, MJR Magnifique, Survey No 75 & 76, Khajaguda X Roads, Raidurgam, Hyderabad, Telangana – 500008. Is FlexSalary Safe? Yes. FlexSalary is fully legit and safe. The website is also safe to use as it is HTTPS-secured and SSL certified as well. However, regarding the customer service of the company, many borrowers of loans have complained. Despite that, as per our experience, we think the app works quite well and is legit. Furthermore, the company has a CIN number, and it is registered through the Reserve Bank of India. When Can Flex Salary Comes To Rescue? There are certain circumstances where flex salary comes to the rescue. You need to get through the possible solutions that can make things easier for you. You need to follow certain steps that can make things easier for you to attain your requirements with ease. 1. Don’t Have Collateral Flex salary will offer you unsecured lines of credit loans. You do not have to pledge to your assets if the collateral gets approved for your loan. You need to get through the complete process that can develop things in perfect order. 2. If Your CIBIL Score Is Low Flexsalary will not focus on your CIBIL score to provide you with the loan you need in times of crisis. If you have a low CIBIL score then you must go through the best flex salary options to meet your requirements with ease. 3. Need An Emergency Cash If you are facing a medical emergency and you need the loan on an immediate basis, then you must consider using Flex salary. You need to identify the perfect solution that can make things lucid for your business development. 4. Loan Is Rejected By Banks If you have low income, bad credit history, and banks have rejected your loans, then Flex salary can be the best option for you. Flex salary will offer you loans at times of crisis. You do not have to pay any kind of interest to get these loans. 5. Don’t Want To Pay Excess Interest If you are afraid of bearing the higher interest rates on your loan, then Flex interest loan amounts can be one of the best options for you. If you do not use money, you do not have to pay the interest. 6. If You Need A Loan For A Lifetime Flex salary personal line of credit you can receive for a lifetime. Your credit limit gets filled up once you pay back the withdrawn amount. It works almost like that of a credit card. You need to identify the perfect solution that can make things easier for you. Can You Get An Instant Personal Loan For Your Marriage From Flex Salary? Yes!! You can receive an instant personal loan for your marriage when you opt for the flex salary. If you have an urgent need for cash in order to meet your marriage-related expenses, then Flex salary can be of great help to you. You will get the help for money within a few hours. It can help you to get the desired amount of money for a personal loan when you need it the most from your endpoints. How To Do FlexSalary Login? – Steps To Follow The following are the steps through which you can apply for a loan through FlexSalary: Step 1: Visit their official website and click on "Apply for an Instant Loan." Step 2: You will get a form on the next page, which you will need to fill out and add information into. Add all the documents required to get a loan from the FlexSalary platform. Step 3: There are various verification processes available. You can either apply for Net Banking Verification or you can upload the documents on your own. Once you upload the documents, they will verify your credentials and will tell you what you are eligible for. Through the app, it is almost the same. All you need here is to download the app and register your account with it. FlexSalary – Eligibility Of The Loan Loan RequirementsEligibilityAge Of the Borrower22 to 60FlexSalary Credit ScoreDepends on the type of loan applied for.Type of EmploymentSalaried professionals only.Minimum Monthly Income₹ 8000 (However, it can change depending on the loan amount applied for)Work ExperienceWork experience requirements depend on loan terms and amounts. Required Documents1. Salaried Employees- Identity Proof (Aadhaar / Driving License / Passport / Voter ID) - PAN card - Address Proof (Driving License / Utility Bills / Aadhaar / Passport / Bank Statements / Voter ID) - Last three months Pay Slips - Photo with the applicant’s face clearly visible. (The applicant will be prompted to take a selfie or upload a photo while applying for a loan through the FlexSalary mobile app) - Net banking verification to validate the bank account and salary information of the applicant 2. Self-Employed Individuals- No loan is allowed for self-employed- The applicant must have an employment FlexSalary Reviews From Customers The following are some of the useful customer reviews regarding FlexSalary that you can benefit from: Syed Abrar: “I'm very happy much satisfied with the service Uma Maheshwari are very nice she was helped me through out the process I got the loan amount as soon as the documents were collected best app.” Manjeera Dhfm: “My credit limit was activated in 1day. But I was not able to withdraw amount,due to my account issue, then customer support team interacted with me continuously and solved the problem. Thank you team. They are well mannered employee's who have patience to listen the issue and resolve it quickly.” Selva Raj: “Last month urgently required some amount, one of my friend referred me Flexsalary and they had treat me as a friend and pay me the amount with very minimum documents. Thank you Flexsalary very fast, very effective good customer service really appreciate your overall performance.” Summing Up Hope this article was helpful for you in getting a better idea of the FlexSalary platform. If you are hoping to get a loan from this platform, you need to download the app and register your account. Furthermore, you need to upload all the necessary documents. They will verify and give you the loan within one to five days if you are eligible for it. Do you know of any better loan app, which is registered by the Reserve Bank of India, and offers instant personal loans? Share some of them with us in the comments section below. Explore More: The Amazon Store Card All You Need To Know About BNKU Stock: MicroSectors US Big Banks Index 3X Leveraged ETNs IPOE Stock – Present Price, Forecast, Statistics – Should You Invest In It In 2022?

Apr 28, 2023