Fullerton India Review: Things To Know Before Taking A Loan!

Nowadays, if you are in need of money, whether it’s for personal uses or for your business, getting it instantly is a major convenience. Therefore, many new loan institutions are cropping up globally. One such company from India that I am going to discuss is Fullerton India Ltd.

To learn more about this Kolkata-based company, read this post till the end!

Fullerton India: Company Overview

Fullerton India credit company Ltd is a new finance company originating from Kolkata, India. With its headquarters in Park Street, they have managed to gain a lot of traction lately by providing instant loans to people and businesses.

One of the primary reasons they have become popular is because of how easy it is to get approved loans from Fullerton. Plus, their loan application processes are easy – you can do them entirely online if you wish to! In addition, you don’t need a Fullerton India credit company limited account!

Fullerton is similar to other Indian financial institutions like Navi, PayMe India, and LoanTap.

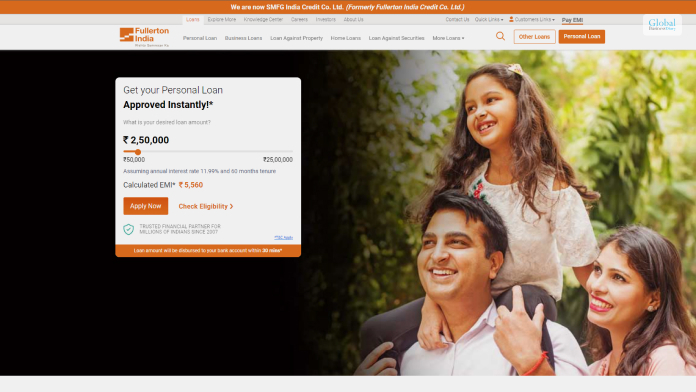

Fullerton India Personal Loans

Fullerton India is widely renowned for providing personal loans to account holders at lower-than-average interest rates. As long as you are eligible for Fullerton India personal loans and you are a salaried employee, you will get such loans quickly.

All the procedures of this company are completely transparent to ensure that there are no hidden charges or secret terms and conditions in place. In addition, most of the Fullerton loan payment solutions can be customized by you to an extent.

| Maximum Loan Amount | Upto INR 25,00,000 |

| Repayment Tenure | Minimum 12 months, maximum 60 months |

| Interest Rate | Starting from 17% |

| Processing Fees | Upto 6% of the total loan amount |

| Prepayment Charges | Upto 7% of the total loan amount |

Why Should You Apply For Fullerton India Personal Loan?

Some of the benefits of applying for a Fullerton India personal loan are:

- The application process for this loan is 100% digital – no paperwork is required.

These personal loans are free of any collateral. - Repayment tenures for these personal loans are flexible.

- Since these are personal loans, the reasons for applying for this loan can be anything.

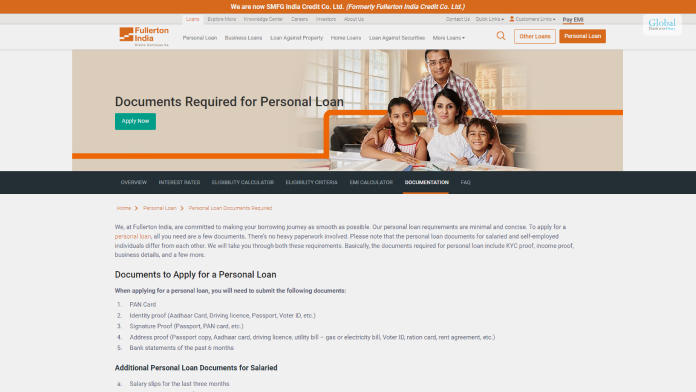

Required Documents

To apply for this loan, you need the following documents:

- A filled application form that is also digitally signed.

- Identity proof (should contain proof of your address, age, and citizenship)

- Salary Pay Slips for the last three months

- Bank statement for the last six months

- Form 16 Income Tax Returns report

- Other necessary financial statements and Proof of income (if you are self-employed)

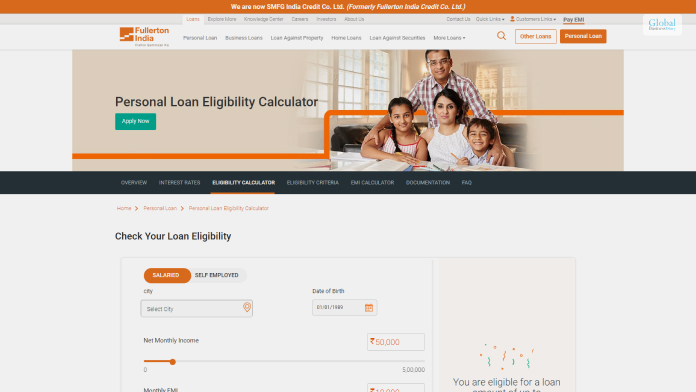

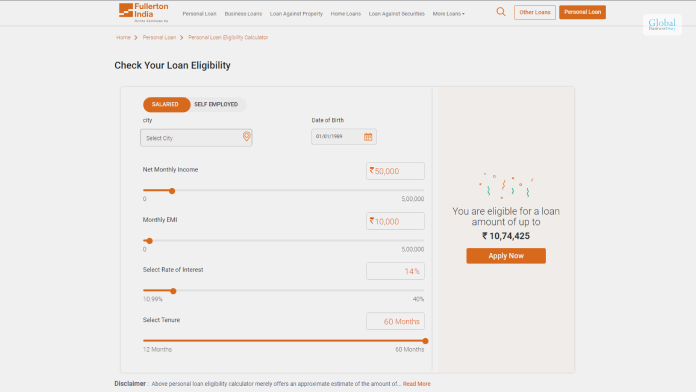

Personal Loan Eligibility Criteria

You will be eligible for Fullerton India personal loans by meeting these requirements:

| Age | Minimum 21, maximum 60 |

| Employment Status | Must be salaried or self-employed |

| Minimum Income | Minimum salary INR 25,000 |

| Credit Score | 750+ CIBIL score with a good credit history |

| Nationality | Indian |

| Work Experience | Minimum 1 year of work experience |

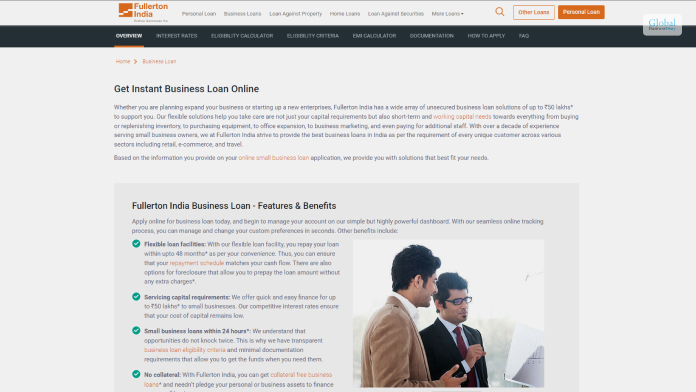

Fullerton India Business Loans

If you are an entrepreneur and you are in need of funds to expand your business, then contact Fullerton India. They have business loans for all types of businesses, both big and small.

Not only will these loans help you manage your business capital necessities, but they will also help you manage your capital needs for other purposes. This includes inventory purchases, workspace expansion, marketing, and any other additional payments.

| Maximum Loan Amount | Upto INR 50,00,000 |

| Repayment Tenure | Minimum 12 months, maximum 60 months |

| Interest Rate | Starting from 11.99% |

| Processing Fees | N/A |

| Prepayment Charges | N/A |

Why Should You Apply For Fullerton India Business Loan?

The primary benefits of applying for loans from Fullerton India home finance company limited are:

- All the loan facilities provided by the company are flexible since you have a loan repayment tenure of upto 48 months.

- Such business loans of upto INR 50 lakhs will be provided to you quickly within 24 hours after you apply.

- There are no collaterals for Fullerton business loans.

- You can access your loan account online pretty easily.

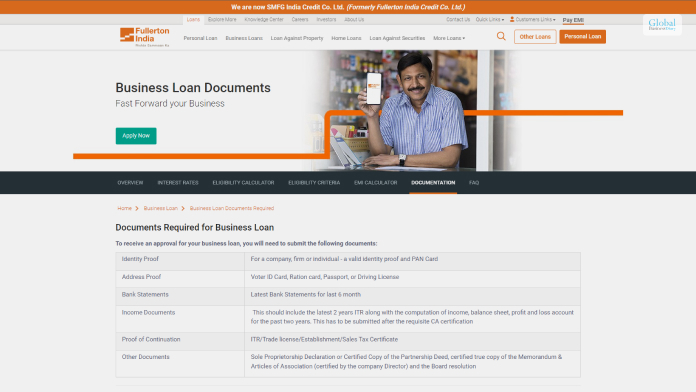

Required Documents

To apply for this loan, you will need these documents:

- A recently clicked photograph of you.

- Identity proof, like your PAN card.

- Address proof like your passport.

- Necessary bank statements

- Income Tax Report (ITR) files or GST Reports

- Income proof

- Business existence proof (like your business’s Certificate of Existence)

Business Loan Eligibility Criteria

You and your business will be eligible for these loans if you meet these requirements:

| Age | Minimum 25, maximum 65 |

| Business Status | Sole proprietorship or partnership |

| Minimum Turnover | Minimum INR 10,00,000 per annum, with INR 2,00,000 profit |

| Credit Score | 750+ CIBIL score with a good credit history |

| Nationality | Indian |

| Business Experience | Minimum 3 years of business life with profits in the last two years |

Other Types Of Fullerton India Loans

Apart from the two loans described above, which are the specialty of Fullerton India, they also provide other customizable loans like:

- Loan Against Property: If you have an immediate expense to clear out as soon as possible, then you can get a loan against your property as collateral instantly!

- Two-Wheeler Loans: These are short-term loans for purchasing your first two-wheeler!

- Home Loans: If you wish to purchase that dream house you have been eyeing for some time, you can apply for this loan!

- Commercial Vehicle Loans: If your business needs a commercial vehicle like trucks and other vehicles, you can apply for this loan!

How To Apply For Fullerton India Loans?

If you wish to apply for a Fullerton India loan, you have to follow a simple process, which I have described below:

- First, go to the Fullerton India official website.

- Here, click on the Apply Now button at the top of the page.

- Now, out of all the loan options, select the type of loan you wish to apply for.

- Depending on the type of loan you have chosen to apply for, an application form will open on your screen. Fill it up with all the required details.

- After you have filled up the application form, click on Next.

- An OTP will be sent to your registered email ID and phone number. Confirm them by following the on-screen procedures.

- Now, you must upload scanned copies of the necessary paper documents.

- After you are done uploading scanned copies, click on Submit.

After you hit the final Submit button, Fullerton India will get back to you if your loan is approved in the next 24 hours.

Conclusion

Fullerton India provides loans to people who are in dire need of them. All you need to do is meet their eligibility criteria and apply for their loans online! Plus, they provide many loans like personal loans, business loans, loans against property, two-wheeler loans, commercial vehicle loans, and home loans to apply for!

If you have any queries, please comment below!

Read Also:

Tags:

Recent

Due Diligence Decoded: Why Careful Evaluation Still Wins in Business

Jul 11, 2026

How Hydraulic System Design Impacts Equipment Performance

Jul 01, 2026

Startup Bootstrapped Fundraising Strategy: A Guide for SaaS and Tech Startups

Jun 21, 2026

Where Distributors Lose Profit Without Realizing It

Jun 20, 2026

Related Articles

Consideration For Choosing Or Comparing Credit Cards

Choosing the right credit card, also known as charge plate or plastic money, is an important decision that can offer valuable perks, financial flexibility, and benefits. In this article we’re going to be assessing a number of factors with the aim of making the right decision while choosing the card. Consideration will be given to payment flexibility and terms, credit card types, network, and terms and conditions. Lastly, thoughts will also be given to its universality. Comparing Credit Card Payment Flexibility and Terms and Terms There is not an iota of doubt on the fact that credit cards have offered innumerable benefits to people. Amidst their different facilities, flexibility is undoubtedly one of them. It has undoubtedly provided the necessary convenience to people. We shall compare payment flexibility and terms associated with plastic money. To get information on comparing credit cards visit: https://moneywise.com/. Analyzing Payment Flexibility Options Across Credit Cards Some cards have a flexible due date that suits your financial situation and allows you flexibility in managing payments. We all know that the management of payments is indeed one of the biggest challenges entrepreneurs face in their day-to-day lives. Another form of control offered by other cards is the adjustment of minimum payment based on financial capacity. Other flexibility options on the block are the allowance to select how often you make payments such as monthly, bi-weekly, etc. Evaluating the Importance of Payment Terms The impact on payment scores positively influences your credit score, while late payment significantly affects your reputation. Payment terms influence interest accrual on the outstanding balance, so it shouldn’t be ignored. Fees and penalties are imposed based on payment terms; it’s why it is important to adhere to due dates. Responsible Credit Card Usage for Optimal Payment Terms Timely payments help in maintaining optimal payment terms that affect your financial standing positively. Also, note that if you maintain a low monetary utilization ratio by not exceeding your threshold, your payment management terms will be effectively enhanced. Related: Credit Card Frauds And What You Can Do To Avoid Them Comparing Credit Card Type and Network Plastic money, as a versatile financial tool, offers a variety of benefits depending on network affiliation and types. Understanding Credit Card Types Credit cards have undoubtedly revolutionized the entire payment system. They not only helped with the quick transfer of money but also facilitated business development. However, we understand the different types of credit cards in this section. · Secured: This card type is good for people rebuilding their credit card history. It requires a security deposit. · Unsecured: These are the most common types used to cater to a wide range of financial needs and require security deposit. · Reward: Rewards or incentives such as cashback, points, or miles depend on your spending pattern. You will find different reward offers from different providers. You should therefore choose one that suits your lifestyle. For example, you can compare Amex Gold vs Chase Sapphire Preferred to see what each offers before making a choice. · Student: These types are designed for students to help them establish their credit history. These card types have lower monetary limits. Analyzing Different Credit Card Networks Different types of plastic money are available in the financial market. The main ones are - · Visa: This option is versatile with extensive network offerings. It is widely accepted globally and caters to various consumer needs. · Mastercard: This option is also accepted globally and comes with different beneficial offers and perks that make it a popular choice among consumers. · American Express: This premium credit card type is favored by customers seeking rewards and luxury. The American Express is also known for its exceptional customer service. · Discover: Discover doesn’t have any annual fees and is good for individuals looking for straightforward rewards such as cash-back rewards. Comparing Terms and Conditions of Plastic Money Plastic money has ushered in a revolution in the entire circle of the payment system. However, we try to understand some of the ways through which the entire payment system. Different financial organizations have their own terms and conditions for their credit cards. Terms and conditions are laid out guidelines and rules governing the operations and responsibilities of both the issuer and cardholder. Key Comparison Factors Interest rates, credit limits and penalty charges are some of the critical terms and conditions to watch out for when signing up for the plastic. You should carefully note the penalties imposed for late payments, exceeding the threshold, or other infractions. Making Informed Decisions Based on Terms and Conditions Before committing to terms and conditions you’re encouraged to read it thoroughly. By comparing these terms with those across multiple offers, you’re likely to find the best suited for you. Assessing Credit Card Versatility: International Use Plastic money offers flexibility and convenience for transactions worldwide as a financial tool because of its ubiquity and its technological integration. They facilitate seamless currency conversion, allow for online transactions and, above all, enjoy global acceptance providing a comfortable payment option for travellers. Comparing Plastic Money Networks for Global Usability American Express, Visa, Mastercard and Discover are common monetary instruments that have gained extensive worldwide acceptance and used globally for transactions by travelers. This has made them the preferred choice for many individuals the world over. Merits and Demerits of Using Credit Cards Internationally Convenience, a secure way of making purchases and the accrual of rewards and benefits are some of its advantages. Drawbacks such as incurring foreign transaction fees and exchange rates, which may not be favourable may be applied by the plastic money companies. You can read this article to learn more about this international type of payment. Conclusion With comparison from the standpoint of information, one can make choices that best align with one's lifestyle and financial goals. However, a good understanding of its diverse landscape, terms, conditions, and other factors is crucial to making the right choice. The right card is the key to optimizing your financial experience while traveling or making international purchases. Read Also: The Amazon Store Card All You Need To Know About California No Credit Check Loans: A Solution For Those With Poor Credit Home Credit: Information, Eligibility Criteria, Interest Rates, Review & More

Oct 20, 2023

Is Twitch Stock Worth Buying Now? Everything You Should Know

Want to buy the twitch stock to get better returns from your investments? If yes, you have to do the necessary research work about the company’s condition before making your investment. Without doing the research, if you make your investment in Twitch stock, it can be a matter of great concern. Multiple factors can affect the stock status of your company. You cannot ignore them at once. Twitch Company Inception Story In 2011, Twitch company laid down its foundation by Justin Kan. He was an American Tech investor and innovator involved in numerous different venture capital investing and startups. Twitch was the continuation of an experiment done by Justin kan on Justin. Tv. Today, the twitch stock prices are creeping high at a faster pace. In 2014 Justin Tv was shut down and acquired by Amazon. But Twitch took over the share prices of the Justin Tv and launched it in the market with the same intention to excel in it. Brief Details About Twitch Stocks Twitch stocks are the stock market games, or you can tell it as the simulation where the stocks are the twitch Streamers. The game is a simplified model for a traditional stock market for most twitch streamers. So, investors can start selling and buying the twitch stocks, and they will benefit the gamers in this investment. An interesting new concept appears when you are talking about twitch stocks. It is one of the virtual stock markets that you can invest in. Twitch streamers are the stocks that can be sold and brought by considering them as stock. There is no real money involved in twitch betting in this stock format. You can use this game just for fun. However, there are some real options available if much virtual trading is involved. How Do Twitch Stocks Work? The Stocks and shares of the Twitch stock work based on the actual twitch stock or shares for the twitch stocks game. There is no way to earn real money from it as there is no money involvement while playing. You can buy Amazon stocks to get the returns from the investment from Twitch stocks. However, when exploring the options for various prizes, you need to know the most advantageous portfolios at the end of different time ranges. On What Factors The Stock Prices Of Twitch Stock Varies? There are several factors on which the prices of twitch stock vary. You need to know these factors before you decide about investing in these stocks. Multiple factors are there that hunters the growth of the Twitch stock some of them are as follows:- A total number of followers the streamers have. Average viewerships. Trading activity on the virtual trading platform. A total number of the channel views the trading platform possesses. Why Should You Invest In Twitch Stocks? There are specific genuine reasons which can provoke you to make your investment in Twitch stocks. Some of them are as follows:- Real money is not at risk. You do not have to risk the real money for making investments in Twitch stock. Amazon owns Twitch, so if you want to invest and grow your trading business, then Twitch stock can help you in that. When you buy the shares of Twitch stocks today, it means you are purchasing the shares of Amazon. As a result, it will provide you with better returns from your investments. You can also buy shares in some of the esports teams. Today, the total number of Twitch streamers has increased to 500 followers, even more than the previous count. You can become a Twitch affiliate and earn commissions from it once you reach 50 followers after your game streaming. Making money from Twitch is quite simple as Amazon charges the subscription money from the Streamers depending on the Tier of cities you want. You can buy the twitch stocks depending on various subscription rates like:- For Tier 1 streamers, you will get $4.99. Tier 2 streamers will receive $ 9.99. The tier 3 streamers will receive$ 24.99. These are some of the core reasons you need to take care of while developing your returns from the investment in Twitch stock. Is Twitch A Public Company? The answer to this question is Twitch is not a public company; instead, it is a private company. It is why you cannot buy Twitch, but you can trade twitch stock by owning the stocks of Amazon. In addition, you can deal with these stocks by leaving them with some options. Now, if you are not aware of the basics of the options, you can start your trading with Twitch. You do not have to spend hundreds and thousands of dollars on Twitch stock. First, however, you need to understand the ways before earning better returns from Twitch. How Much Competition Affects Twitch Stock? Today in 2021, people are streaming multiple hours of content on a per-day basis depending on the demographics of GenZ and millennials. But, when it comes to the games, it reigns supreme. Plenty of similar services users can gain from any other live streaming opportunities. But, unfortunately, you cannot be able to make your choices in grey. The IPO of Twitch stock is increasing its credibility over the past few years. It will help you to achieve your goals in the best possible manner. The more you can make your choices in the right direction, the better you can achieve your goals. Who Are The Core Competitors Of Twitch Stock? The core competitors of the Twitch Stocks are as follows:- NetFlix. OnlyFans. These are some of the core Competitors of the Twitch Stocks who can provide stiff competition to the share prices of the Twitch Stock in a short period. Frequently Asked Questions (FAQs) [su_accordion class=""] [su_spoiler title="Q1. Does Twitch Have A Stock?" open="yes" style="default" icon="plus" anchor="" anchor_in_url="no" class=""]There is no such Twitch stock as it is a subsidiary of Amazon. It is not a publicly-traded company. If you want to transfer stocks, then twitch stock is the best option for you as you will get the affiliates of Amazon. [/su_spoiler] [su_spoiler title="Q2. What Company Owns Twitch?" open="yes" style="default" icon="plus" anchor="" anchor_in_url="no" class=""]Amazon owns Twitch stock as it is the subsidiary of that company. Investors can gain more from it in the current year. Owning the Twitch stock today can provide plenty of opportunities like shll stocks provides its users today.[/su_spoiler] [su_spoiler title="Q3. Can You Talk Stocks On Twitch?" open="yes" style="default" icon="plus" anchor="" anchor_in_url="no" class=""]Viewers can buy the simple stocks by placing some simple commands and putting forward their opinion in Twitch stock. Yes, but with caution as the market of Twitch, stocks are increasing at a rapid pace. [/su_spoiler] [/su_accordion][su_accordion class=""] [su_spoiler title="Q4. How Much Is Twitch Worth In 2022?" open="yes" style="default" icon="plus" anchor="" anchor_in_url="no" class=""]The current value of the Twitch stock is worth $5 million, and it can rise in the years to come. It is the current rate, and the rates can differ with the passage of time. You have to stay vigilant about it if you want to become smart investors in it.[/su_spoiler] Final Take Away Hence, if you want to get better returns from your investments from your twitch stock, then you need to understand the market sentiments in the correct order to achieve your goals. Therefore, do not make your choices in grey while you want to gain a better return from your Twitch stock. Instead, try to achieve your goals in the best possible manner. Read Also: Why Create A Powerful Business Continuity Plan? How To Start A Business In 2021 – Best Business Strategies Is Nykaa Going To Dominate The Market With Their Recent Launch?

Jan 05, 2022

Maximizing Your Home Loan Options: Finding The Best Fit For Your Financial Goals

The home loan process begins with a pre-approval, followed by house hunting. Once a home is chosen, an application is submitted to the lender. The lender then appraises the property, reviews the application, and, if approved, funds are released for purchase. Understanding the steps for a successful transaction is crucial in any business. Choose Loan Market Canberra to ensure efficiency, reduce the risk of errors, and promote trust between trading parties. It fosters smooth operations, and customer satisfaction, and ultimately, boosts profitability. Assessment Of Personal Finances Evaluation of the current financial status is essential in understanding one's economic stability. It involves assessing income, expenses, assets, and liabilities, followed by creating balanced budgets and financial goals for a secure future. Determining the affordability of a house involves analyzing your monthly income, expenses, and potential mortgage payments. Factors such as down payment, interest rates, and property taxes can significantly influence home affordability. Always plan wisely to avoid financial stress. Having a good credit score is crucial as it influences lenders' confidence in your ability to repay loans. It can dictate mortgage rates, insurance costs, and even employment opportunities. High credit scores potentially offer better loan terms, lower interest rates, and greater financial opportunities. Understanding Different Types Of Home Loans Conventional loans are a type of mortgage loan not insured by any government agency. These are typically offered by private lenders and banks, and often require stringent criteria such as good credit rating and a substantial down payment from borrowers. Government-insured loans are financial borrowings backed by a government agency. These loans, like FHA and VA loans, provide lenders with a safeguard against borrower default, thereby enabling lenders to offer favorable loan terms, such as lower interest rates or reduced down payments. Fixed-rate and adjustable-rate mortgages are two primary options for homebuyers. Fixed-rate holds a consistent interest rate throughout the life of the loan, ensuring predictable payments. Adjustable rates initially offer lower rates, but these can fluctuate over time, potentially increasing repayments. Preparing Important Documents To apply for a home loan, various documents are needed. These include proof of income, credit history, employment verification, tax returns for two years, bank statements, and identification proof. Each lender might require additional specific documents. Collecting all financial documents beforehand is crucial for accuracy and efficiency in financial management. It helps in proper bookkeeping, eases audit processes, prompts decision-making, and avoids legal issues. Moreover, it ensures transparency and accountability in financial dealings. The process of getting pre-approved for a loan involves assessing your creditworthiness and financial capabilities. It's significant because it provides a preliminary indication of how much you can borrow, thereby helping you set a realistic budget when buying a home or car. Making The Home Loan Application The home loan application process involves several stages. Initially, a borrower completes an application with a lender, providing financial and personal information. Next, the lender evaluates this information to determine the borrower's ability to repay the loan. Approval may include specific loan terms and conditions. Common mistakes to avoid during applications include submitting incomplete or inaccurate information, overlooking instructions, providing irrelevant details, not customizing the application for certain roles, late submission, and neglecting to proofread, which results in spelling and grammar errors. Home Appraisal And Inspection A home appraisal is a professional's unbiased evaluation of a home's market value. It's vital during a sale or refinancing process, as it helps in determining an accurate selling price or loan value, ensuring a fair transaction, and preventing overpayment. The necessity of a home inspection can't be overstated. It provides the potential homeowner with vital information about the property's current state, helping to identify any serious issues or needed repairs. This informs buying decisions and helps prevent future complications. During the inspection, if potential issues surface, ascertain their severity. Prioritize those requiring immediate attention. Seek professional advice if necessary and initiate corrective actions. Document findings proposed solutions, and track progress until resolution, ensuring efficient communication with relevant stakeholders. Financial Aspects Of Closing On The Home Closing costs are expenses over the property price that buyers and sellers incur to complete a real estate transaction. Understanding and signing closing documents is crucial during property transactions. These documents typically contain significant agreements, including mortgage terms, payment details, and property details. Carefully reviewing each clause before signing can prevent future disagreements or disputes. Once your home loan has been approved, the lender will send a formal approval letter outlining the loan amount, terms, and repayment schedule. You now need to complete further paperwork, like signing mortgage documents, before proceeding to the property settlement and finally moving in. Conclusion Obtaining a home loan involves several steps. First, assess your budget and determine how much you can afford. Then, research potential lenders, and compare interest rates and loan terms. Submit a loan application, and provide necessary documents. Lastly, finalize the loan upon approval. Informed decision-making is essential throughout any process to ensure successful outcomes. It entails gathering extensive, relevant information, and analyzing and interpreting it accurately. This not only reduces uncertainty and risks but also enhances productivity, efficiency, and overall success. Significant entry into homeownership can feel overwhelming but don't be daunted. Start your home loan journey today. Each step forward brings you closer to owning your dream home. Empower yourself with research and seek professional advice. Your perfect home awaits you. Read Also: How To Get Personal Loan On Bajaj Markets Speed Up Your Funding: A Quick Guide To Business Loans What You Should Know Before Committing To A Cash Buyer

Jan 05, 2024

Instant Loan App: Top 25 Best Loan Apps Should You Know In 2023

With the rise in the level of digitization, there has been a simultaneous rise in the number of instant loan apps in the last few years. As per various sources, in the year 2022 itself, the demand for personal loans surged by 50% in the retail industry. However, a very interesting fact is that in the disbursement of personal loans, non-banking financial institutions were on top of banks. In this article, we will mainly discuss the top twenty-five instant loan apps that offer personal loans in 2023. These are the best loan apps that will allow you to avail of loans fast. However, these apps come with different types of service options, and the time of disbursal changes with the app. Hence, to get fully informed, read on through to the end of the article. The Best 25 Instant Loan Apps In 2023 The following are the best instant loan apps that you must look for before you try to avail yourself of personal loans fast in 2023: 1. Earnin If you are qualified to get loans in this app, you can get an emergency loan from this app if you are confident to pay it back. The advances are large. 2. Chime This is one of the best $50 Loan Instant Apps if you are looking for payday loans. However, lenders can still charge high interest. 3. Current The best thing about this app is that there are no overdraft fees associated with it. Furthermore, you can get overdraft protection of $200. 4. MoneyLion You can get an instant cash advance of up to $300 dollars, and you can also be able to access and improve your credit score. 5. Brigit This is one of the best cash advance apps. If you are an eligible member, cash advances are available to you between #50 and $250. 6. Dave This is one of the best $100 loan instant apps that you will come across. Cash advances start here at only $5, and there is also automatic overdraft protection. 7. Spotloan Once you do a SpotLoan login, they will inform you, "It’s an installment loan, which means you pay down the balance with each on-time payment.” It means that it is not a payday loan app. 8. Bright Lending You can get loans from $300 to $1000, but there are also triple-digit APRs, as well as short terms for repayment. 9. Cash App How to borrow money from Cash App? The Cash App borrow loan services allow you to use the app and access loans from multiple devices using the tag “$cashtag”. 10. MoneyLion With the help of Moneylion NYC, you will be able to avail of credit-builder loans without a credit check if you are a member. 11. SoFi The best thing about this loan app is that you can get even $5000 to $100,000 loans and can get your funds on the same day. 12. PayActiv You can get here early paycheck access, and also you will be able to get up to 50% of earned wages before your payday. 13. Even If you are eligible, you can get up to 50% of your earned wages early, and you can get budgeting tools to track your spending as well. 14. Branch Apart from getting 50% of your earned wages early, you will also benefit from no credit checks and zero-cost loans. 15. Grain If you have low credit scores, then this is one of the best loan apps for you. This is also great if you have a short credit history. 16. Vola If you are able to pay a monthly fee, with the help of Vola, you can permanently avoid overdraft fees with the help of instant cash advances. 17. Empower Borrowing a small number of finances can be easy with the help of the Empower Loan App. Furthermore, there are budgeting tools to track expenses. 18. CLEO The app uses AI to help you analyze your spending and help you by giving actionable insights as well. You can also avoid overdraft charges with the help of rewards and auto savings. 19. SoLo Once you apply for a loan here, you will get a soft credit check, which will not affect your credit score. However, based on the credit check, lenders will have a better idea in regards to lending their money to you. 20. Upgrade Personal Loans You can get fast loans with Upgrade, You can get loans up to $50,000. However, there is a high origination fee associated with the borrowing. 21. Varo Apart from being a loan app, this is also a bank account, which gives you an account with a minimum balance with no monthly charges or overdraft. Furthermore, the credit card option is also secure. 22. Albert According to Business Insider, “Albert is a financial app offering automatic savings tools, cash accounts, cash-back rewards, auto-investing, and much more.” However, you can get some customer service issues, as per complaints of borrowers. 23. LendJet Although not a direct lender, you can get access to a variety of lenders through this platform. Hence, it will be easier to look for personal loans from various options. 24. ZippyLoan Like the other platforms, ZippyLoan also offers you to choose from a variety of lenders. You can get loan amounts from $100 to $15,000. 25. Viva Payday loans You can apply for loans in this app without having a credit history for yourself. The loans are hassle-free, and you will get fast approvals as well. Summing Up Hope this list is informative enough to give you a better idea of the best instant loan apps in 2023. If you are trying to avail of fast loans, then you must try one of these apps mentioned above to get the best services. However, we will still recommend you read all the information related to availing of loans. This will give you a better idea of what services are offered by the loan app that you are taking a loan from. Which of the aforementioned loan apps do you think is the best option for you? Share your reviews with us in the comments section below. Read Also About: Credit Card Frauds and What You Can Do to Avoid Them Home Credit: Information, Eligibility Criteria, Interest Rates, Review & More

Apr 20, 2023