What Is The Leverage Ratio And How to Calculate It?

Leverage ratio is a tool for businesses that helps to determine the extent to which a particular business depends on debt to purchase assets and build capital. On the one hand, it helps businesses determine their own capability to secure funding. On the other hand, the leverage ratio helps investors and lenders evaluate the ability of a business to meet its financial obligations after securing capital.

In this article, you will learn about leverage ratio in general and how it works for businesses as well as investors and lenders alike. We will also share with you details on how to calculate the leverage ratio formula of different types of leverage ratios. Finally, you will learn about the importance of the leverage ratio and how it applies to businesses. Hence, to learn more, read on through to the end of the article.

What Is The Leverage Ratio?

According to Investopedia,

“A leverage ratio is any one of several financial measurements that look at how much capital comes in the form of debt (loans) or assesses the ability of a company to meet its financial obligations. The leverage ratio category is important because companies rely on a mixture of equity and debt to finance their operations, and knowing the amount of debt held by a company is useful in evaluating whether it can pay off its debts.”

Basically, the leverage ratio is a set of ratios with the help of which you can highlight the financial leverage of a business when it comes to assets, liabilities, and equities. The ratio gives you an idea of how much of the capital of a business comes from its debt. Hence, you will get a good idea of whether the business makes well for its financial obligations.

Read More: Network Marketing: What Is It? Is It The Right Option For You?

How Does Leverage Ratio Work?

According to Hubspot.com,

“A higher financial leverage ratio indicates that a company is using debt to finance its assets and operations — often a telltale sign of a business that could be a risky bet for potential investors. It can mean that earnings will be inconsistent, it could be a while before shareholders can see a meaningful return on their investment, or the business could soon be insolvent.”

These metrics are really useful for creditors and investors to find out whether they should extend credit to or invest in the business. If the financial leverage ratio of a company is very high, it means that the company is allocating most of its cash flow to pay off its debts and is more prone to default on loans.

On the other hand, if the financial leverage ratio of a business is low, it shows that the business is financially responsible and has a steady stream of revenue. Even if a company is in significant debt, having a good financial leverage ratio shows that there are minimal risks for investors and creditors, and the business is likely worth an investment.

Leverage Ratio – How To Calculate It?

The following are the different formulae of leverage ratios based on the type of ratio you want to choose:

1. Operating Leverage Ratio

You can calculate it using this formula:

| Operating Leverage Ratio = Percentage change in EBIT (earnings before interest and taxes) / Percentage change in Sales |

2. Net Leverage Ratio

Here is the formula to calculate this ratio:

| Net Leverage Ratio = (Net Debt – Cash Holdings) / EBITDA (Earnings before Interest, Taxes, Depreciation, and Amortization) |

3. Debt-to-EBITDAX

You can calculate EBITDAX using this formula:

| EBITDAX (Earnings before Interest, Taxes, Depreciation, and Amortization before Exploration Expenses) = EBIT (Earnings before Interest and Taxes) + Depreciation + Amortization + Exploration Expenses |

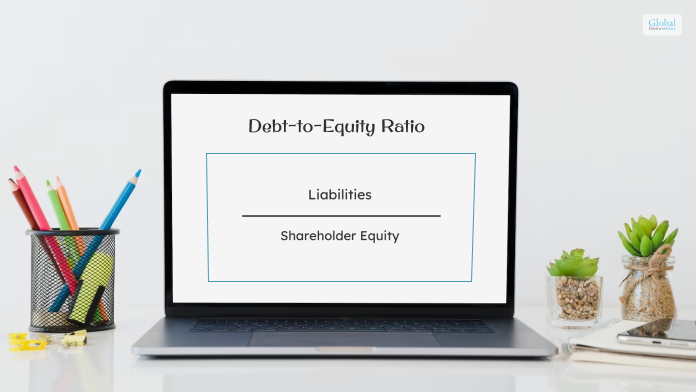

4. Debt-to-Equity Ratio

Here is the formula to calculate this ratio:

| Debt-to-Equity Ratio = Liabilities / Stockholders’ Equity |

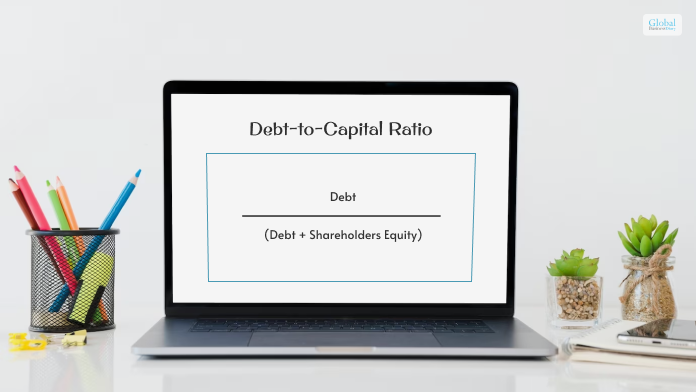

5. Debt-to-Capital Ratio

You can calculate it using this formula:

| Debt-to-Capital Ratio = Debt / (Debt + Shareholders Equity) |

6. Debt-to-Capitalization

Here is the formula to calculate this ratio:

| Debt-to-Capitalization Ratio = (Short-term Debt + Long-term Debt) / (Short-term Debt + Long-term Debt+ Shareholder Equity) |

7. Interest Coverage Ratio

You can calculate it using this formula:

| Interest Coverage Ratio = Operating Income / Interest Expenses |

8. Fixed-Charged Coverage Ratio

Here is the formula to calculate this ratio:

| Fixed-Charged Coverage Ratio = EBIT (Earnings before Interest and Taxes) / Interest Expense of Long-term Debt |

By having a good idea of your leverage ratios related to a business, you might understand how the business can run in the near future.

Why Is Leverage Ratio Important?

According to the Wall Street Mojo,

“Leverage ratios are important as they allow investors to assess a company’s financial position with respect to its financial obligations. Though firms have an option of using their equity to purchase assets and resources for undertaking different business activities, they go for taking up loans to finance their capital building. The reason is one – the cost of debt or cost of borrowing is way less than the cost of equity.”

The different types of leverage ratios help investors get a better idea of how the business’s capital flow is structured. By calculating these ratios, you can have information about a company in regard to whether it can take advantage of its leverage or not.

For example, if the company you want to invest in or lend credit to has taken too much debt, it is obviously risky for you. On the other hand, if the leverage ratio is too low and the company does not have any debt, it will be able to pay off too much cost of capital and reduce its earnings in the long run. Hence, consider your choices carefully.

Read More: Project Management: What Is It? – Major Types, Examples, And More

Wrapping Up

Hope this article was helpful for you in getting an understanding of how a leverage ratio works. You can see here that this is one of the major financial tools with the help of which you can assess a company’s ability to meet its financial obligations. By using it to measure operating expenses, you can get an idea of how differences in output can change operating income.

The debt-equity ratio, equity multiplier ratio, degree of financial leverage, and consumer leverage ratio are some of the common leverage ratios. Do you have any more information to add regarding how to calculate the leverage ratio? Share your ideas and opinions with us in the comment section below.

Read More:

Tags:

Recent

Due Diligence Decoded: Why Careful Evaluation Still Wins in Business

Jul 11, 2026

How Hydraulic System Design Impacts Equipment Performance

Jul 01, 2026

Startup Bootstrapped Fundraising Strategy: A Guide for SaaS and Tech Startups

Jun 21, 2026

Where Distributors Lose Profit Without Realizing It

Jun 20, 2026

Related Articles

The Impact Of News Releases On Forex Markets

Today, we're about to embark on a journey that separates the rookies from the seasoned pros in the dynamic world of forex trading. We're diving headfirst into the thrilling realm of news releases and their undeniable influence on the forex market. Strap in, because this is where the real action happens, and understanding it can be the key to unlocking your trading potential. The News Release Rollercoaster: A Brief Overview Alright, let's start with the basics. News releases, or economic indicators, are like fireworks in the forex market. They're announcements made by governments, central banks, or other influential organizations that provide critical information about a country's economic performance. These announcements can cover a wide range of topics, from employment figures and inflation rates to comparisons like robomarkets vs roboforex. Why Should You Care? Now, you might be wondering, "Why should I pay attention to these news releases?" Well, my friend, they hold the potential to send shockwaves through the forex market, and this can mean either a wild ride of profit or a bumpy road to losses. Ignoring them is like trying to navigate a ship blindfolded – not a great idea! Market Reaction: The Lightning-Fast Response The forex market is like a finely-tuned machine, reacting swiftly to any new piece of information. When a major news release hits the wires, you can bet your bottom dollar that currencies will start dancing. Prices can soar or plummet in a matter of seconds, catching unprepared traders off guard. The Two Faces of News Releases News releases can be classified into two main categories: scheduled and unscheduled. Scheduled releases, like the Non-Farm Payrolls report or interest rate decisions are announced at fixed times and are eagerly anticipated by traders worldwide. Unscheduled releases, on the other hand, can hit the market unexpectedly due to unforeseen events like natural disasters or political crises. Also Read: What Are BA Stocktwits? Is BA Stocktwits A Good Buy? The Forex Calendar: Your New Best Friend To stay ahead of the game, you need to keep a close eye on the economic calendar. It's your playbook for scheduled news releases. Websites like Forex Factory or Investing.com offer comprehensive calendars with details on upcoming releases, their expected impact, and historical data. Trust me, this tool will become your trading sidekick. Three Major Players in the News Release Game Now, let's talk about the big dogs of news releases: central banks, governments, and international organizations. These heavyweights have the power to make or break currencies with their announcements. Pay special attention to the Federal Reserve in the US, the European Central Bank (ECB) in the Eurozone, and the Bank of Japan (BOJ) in Japan. Reading the Tea Leaves: Interpreting News Releases Understanding the potential impact of a news release is vital. Some indicators have a more pronounced effect on the market than others. For instance, interest rate decisions by central banks are often considered the most influential, as they directly impact borrowing costs and monetary policy. The Art of Risk Management: A Crucial Skill When news releases hit, volatility can spike, and emotions can run high. This is where solid risk management comes into play. Set stop-loss orders, use proper position sizing, and consider reducing your exposure during high-impact news events. Remember, it's not about avoiding risks entirely, but about managing them smartly. Strategies for Tackling News Releases Alright, it's time to get tactical. There are two main strategies for trading news releases: the breakout strategy and the fade strategy. The Breakout Strategy: This involves placing pending orders just outside the current price range before a major news release. When the news hits, and volatility spikes, one of these orders will be triggered, potentially leading to a quick profit. The Fade Strategy: Contrary to the breakout strategy, this involves going against the initial market reaction. You wait for the initial surge or drop in price, and then enter a trade in the opposite direction, anticipating a retracement. Final Thoughts: Navigating the News Release Maze So, there you have it, my friend – the ins and outs of how news releases can rock the forex market. Armed with this knowledge, you're better equipped to tackle the wild swings and capitalize on the opportunities they present. Remember, practice makes perfect, so start small, build your confidence, and always keep learning. Happy trading! Also Read: Trade With Precision: Steps To Implement Your Prop Trading Strategy What Is IPO (Initial Public Offering) Stock And How To Buy It? Trading Options Using Iron Condors

Nov 24, 2023

Successful Trading Strategies With Bullish Engulfing Patterns

In financial markets, traders are constantly on the lookout for reliable patterns and signals to guide their decisions. One such pattern that has stood the test of time is a bullish engulfing pattern. This candlestick pattern is a strong indicator of a potential bullish trend reversal and has been a cornerstone in the toolkit of successful traders. So, delve into the strategies below that traders employ to capitalize on the Engulfing Patterns and potentially turn the tides of their trading fortunes. Identifying The Patterns The first step in any successful trading strategy involving these Patterns is identifying them. These patterns consist of two candlesticks – the first is a smaller bearish candle, followed by a larger bullish candle that completely engulfs the previous one. Traders look for this clear and distinct formation on their price charts. It's crucial to use technical analysis tools like moving averages, RSI, and trend lines to confirm the potential reversal before making any trading decisions. Timing Is Key Timing is everything in the trading world, and this holds when dealing with a bullish engulfing pattern. So, to maximize the chances of success, traders often wait for additional confirmation before entering a trade. This can include waiting for the bullish candle to close, ensuring it engulfs the bearish one. Waiting for confirmation can help filter out false signals and reduce the risk associated with premature entries. Setting Stop-Loss And Take-Profit Levels Risk management is a key aspect of any trading strategy, and trading these Patterns is no exception. Setting stop-loss and take-profit levels is crucial to safeguarding your capital and locking in profits. Traders typically place a stop-loss just below the low of the bullish candle that formed the pattern. This level serves as a safety net to limit potential losses if the trade doesn't go as expected. Meanwhile, take-profit levels, on the other hand, are usually set at a reasonable distance from the entry point, allowing traders to secure profits when the market moves in their favor. Combine With Other Indicators Successful traders understand the critical importance of utilizing a variety of multiple indicators and analytical tools in their comprehensive market analysis. While these Patterns are inherently powerful on their own, they become exponentially more robust and reliable when combined with other diverse technical indicators. Traders often vigilantly look for additional confirming signals such as overbought or oversold conditions, pivotal support and resistance levels, or clear trend confirmation from other reputable indicators like the MACD. This multifaceted, layered approach can provide stronger, more reliable validation for the potential bullish reversal, enhancing trading strategies. Practice Patience And Discipline Trading can be emotionally charged, and the excitement of spotting an Engulfing Pattern can lead to impulsive decisions. However, discipline and patience are essential virtues in trading. Successful traders know the importance of sticking to their trading plan and not letting emotions cloud their judgment. They wait for the right setup and confirmations and ensure they are not overtrading. Consistency in applying their strategies is what sets them apart. Conclusion In trading, mastering a bullish engulfing pattern can be a game-changer for traders looking to capitalize on potential bullish trend reversals. By identifying these patterns, timing their entries, setting appropriate risk management levels, combining them with other indicators, and practicing patience and discipline, traders can enhance their chances of success. Remember that no trading strategy is foolproof, and losses are a part of the game, but by adhering to these strategies and continuously learning and adapting, traders can work towards achieving consistent profitability. So, the next time you spot an Engulfing Pattern on your price chart, approach it with these proven strategies in mind, and you might just find yourself on the path to trading success. Read Also: Bnku Stock: Microsectors Us Big Banks Index 3x Leveraged Etns Tui Share Price Forcast: Everything You Should Know Poocoin Stock Forecast: Everything You Should Know

Dec 28, 2023

Capex Vs Opex: Essential Points Of Difference

A company has to pay off different kinds of expenses to run its business smoothly. Capex vs Opex is one of the popular expense differentiation you must know. Among them, two kinds of expenditures are quite prominent in this regard. First is the Capex, and second is the operating expenses. Most of the time, these costs can be one, and sometimes they can take the shape of recurring expenses. You must follow the correct process that can assist you in getting things done in perfect order. Micromarketing techniques can work well here. The capital expenditure of a company will occur once, while the operating expenses will keep on occurring all the time. If you are a business owner, you must know the core points of differences between the two concepts. Essential Points Of Difference Between Capex vs Opex There are several points of difference between Capex vs Opex. It will offer you the complete insight once you go through the complete article. You need to know the reality while making the differentiation between the two concepts of business./ 1. Nature Of Expenses Capex vs Opex has some core differences in the nature of their expense model. Capital expenditures or Capex are investments in assets that provide long-term benefits to a company. These expenses are typically for acquiring, improving, or maintaining assets such as property, equipment, machinery, or infrastructure. Operating expenditures are day-to-day expenses incurred in running a business. These include costs for salaries, utilities, rent, marketing, repairs, and other ongoing operational expenses. You must consider these facts from your end while making the differences between the two concepts. 2. Duration Of Benefit Capital expenditures provide benefits over an extended period, usually beyond one fiscal year. They contribute to the company's future productivity, efficiency, or revenue generation. Capex vs Opex has some significant points of differences that you must know while you make the comparison. Operating expenditures are incurred for immediate use and provide short-term benefits. They are essential for maintaining regular business operations and generating immediate revenue. It will give short-term and regular benefits to your company. 3. Treatment In Financial Statements Capital expenditures are recorded as assets on the balance sheet and depreciated or amortized over their useful life. Depreciation or amortization expense is then reported on the income statement over time. Operating expenditures are immediately shown on the income statement in the period they are incurred. They directly impact the company's net income for that period. You need to identify the perfect solution that can make things easier for you to reach your goals with ease. 4. Tax Treatment Capital expenditures might be eligible for tax benefits such as depreciation or amortization deductions over time, reducing taxable income. Capex vs Opex, you must consider things at your end while reaching your objectives. Operating expenditures are fully deductible in the year they are incurred, providing immediate tax benefits. You should get through this difference to have a better idea of it. Ensure that the scope of errors is as low as possible. 5. Impact On Profitability & Cash Flow While CapEx affects profitability indirectly through depreciation expenses. It has a significant impact on cash flow at the time of purchase or investment. You cannot afford to make things work in the wrong direction from your counterpart. On the other hand, Operating expenditures directly affect profitability by reducing net income and also impact cash flow in the period they occur. Effective planning can boost the chances of reducing the expenses of your business. 6. Decision Making & Budgeting Capital expenditures involve strategic decisions as they impact the company's long-term growth and productivity. Budgeting for CapEx requires careful planning and consideration of future benefits. You should know the core points of differences between Capex vs Opex. It will assist you in attaining your goals with complete ease. Operating expenditures are part of routine budgeting and are necessary for maintaining day-to-day operations. They are generally more predictable and recurring. Without proper application of the strategies, things can turn worse for you. Examples Of Capex Expenditure There are several examples of Capex expenditure that you should know at your end. It will help you to get a better insight into it. Let’s find out some of the core examples of the Capex Expenditure that can make things easier for you. Machinery, manufacturing plants, and equipment. Computers. Building Improvements. Trucks and vehicles. The contribution margin of the company plays a vital role here. You should pay it from your end to meet all the expenditure. Examples Of Opex Expenditure There are several examples present for Opex expenditure that you must know at your end. Some of the core examples of it are as follows:- Salaries and wages. Rent and Utilities Legal and accounting fees. Overhead costs. Business travel. Property expenses. Interest on debt. Research and development expenses. You can easily make the market segmentation with the help of the differences between capex vs opex to meet the requirements. How To Reduce Capital Expenditure? There are several techniques you can employ to reduce the capital expenditure of your company to a great extent. You must follow the correct process in this regard to have a better idea of it. 1. Evaluate The Asset Needs Conduct a thorough assessment of current assets to determine if there are underutilized or redundant assets. Selling or repurposing such assets can free up capital and reduce the need for new investments. 2. Leasing Vs Buying Consider leasing equipment or assets instead of purchasing them outright. Leasing can lower initial costs and shift maintenance and upgrade responsibilities to the lessor. 3. Prioritize Essential Investment Focus on essential investments that directly contribute to core business operations or strategic growth. Prioritize projects that offer the highest return on investment (ROI) and align with long-term business goals. 4. Implement Of Efficient Technology Invest in technology that streamlines processes, reduces manual work, and improves efficiency without significant capital outlay. Cloud-based solutions or software-as-a-service (SaaS) models often have lower upfront costs. 5. Outsource Non-Core Functions Consider purchasing refurbished or used equipment instead of new. Often, these options come at a lower cost while still providing adequate performance and reliability. Final Take Away Hence, if you are making the differences between the two concepts of capex vs opex, then the mentioned points can prove to be useful for you. Try to reduce your expenses as much as possible. It will reduce your debts to a great extent. You can share your views and opinions in our comment box. It will help us to know your take on this matter. Once you follow the correct process, things are going to be easier for you. The application of the correct strategy can make things work for you. Continue Reading For More Business-Related News!! How To Buy An LLC? – Steps To Follow How To Become A Strategy Consultant? Roles & Responsibilities What Is A Sales And Purchase Agreement For Business? – Let’s Find Out

Nov 26, 2023

How To Transfer Stocks From Robinhood To Webull?

Do you want to know how to transfer stocks from Robinhood to webull? If yes, you have to follow specific steps that can help you to transfer the stocks from Robinhood to webull. Unfortunately, investors like you often find themselves stuck in the process of moving the stocks from Robinhood to Webull. They often find themselves in complete disarray as investors could not find out how to transfer stocks from Robinhood To Webull. Step by step, you have to follow a specific process to ensure the smooth transfer of the stocks from Robinhood to webull. First, you must clear your fundamentals about these two platforms before transferring the stocks from Robinhood to webull. What Is Robinhood? Robinhood is an online brokerage trading platform that offers investors discounts and commission-free trading options. The best thing about this trading platform is it provides commission-free stocks. ETF and the options trade are easy to do with this platform. In addition, Free Cryptocurrency trading is possible through this app. What Is Webull? It is also an electronic trading platform that allows commission-free stocks to be traded from mobile phones, computers, and desktops. It will also provide the investors with real-time data, news, and stocks statistics to help them get detailed knowledge about the current market scenario. Webull Vs. Robinhood Points of Differences Robinhood Webull For Beginners Robinhood is better for the beginner investors Webull is better for experienced investors in stocks. Investment Options It offers a more diverse selection of investment options Webull provides a limited range of investment options for its investors. Experience of The Investors Robinhood lacks trading tools compared to webull. The current market scenario can be easily traced with the help of webull. Detailing of each aspect of the stock trends is present here. How To Transfer Stocks From Robinhood To Webull? You need to follow specific steps to transfer stocks from Robinhood to Webull. You will get the complete details to read the article to the end. So, do not skip any point as it is a matter of your stock transfer. You cannot afford to ignore the essential issues that can bother you. 1. Gather Transfer Information From The Robinhood First of all, you need to collect all the required information about Robinhood to know how to transfer stocks from Robinhood to Webull. Then, you have to go through all the information available in the Robinhood app to complete the transfer of stock process from this app to another app. 2. You Must Use The Robinhood Account Number You need to use the Robinhood account number to make the transfer possible quickly without any hassle. Also, you can use the Robinhood app and find your Robinhood account number by tapping in the Account Icon, which is present in the bottom right corner of the app. You just have to click on the investment option, and you can see your account number is located on the top of the screen. Webull can also ask you to produce your most recent statement to clarify all the required information that you need. 3. DTC Number You have to insert the Robinhood DTC number( Depositary Trust Company) number 6769 as it remains the same for every transfer to make your transfer process smoother and effective. It is the third solution to your question about how to transfer stocks from Robinhood to Webull. 4. Transferring Assets After you have collected the required information about Robinhood, it’s time to make a proper assessment for transferring the assets and ensure that it is acceptable in the Webull. You need to remember certain assets that are not accepted on the Webull at your ends, like bonds, mutual funds, penny stocks, and pink sheets, are not accepted on the Webull. The stocks you plan to transfer in webull must be traded in webull. 5. Initiate The Transfer To Webull You have to follow specific steps to transfer the assets or stocks to the webull. Some of the crucial steps are as follows:- You need to hit the transfer button in the Webull app after navigating the Webull deposit page or logo page. The second step of transferring the stock to webull is to “Tap on the transfer stock button on the Webull app.” Select the broker you want to transfer from if you want to transfer your stock from the Robinhood app. You need to enter all the information provided by the Robinhood app in the Webull app to initiate the transfer process. In the last step, you have to tap on the initial transfer button to start the transfer process. The world market economics is changing at a significantly faster pace. Therefore, you have to understand the scenario before making your investment plans. How to transfer stocks from Robinhood to Webull will no longer be a big deal for you if you follow the above process. 6. Follow Certain Steps To Transfer From Webull Whenever you are transferring the cash or the stocks from Robinhood to Webull, you have to understand specific points at your end to make things work for you in the best possible ways. You need to follow specific steps while you want to transfer the stocks to the webull app from Robinhood. Some of the crucial facts are as follows:- You must have a minimum of $500 to transfer assets or stocks using the webull. These transfer charges are maintained by this app as you have to pay a minimum charge of a certain amount to make your transfer possible from the other apps. If you want to transfer the amount freeway, you have to liquidate your assets from the bank and withdraw the required amount essential for the transfer. The minimum Webull transfer fee from Robinhood is $75 for your partial or full transfer of assets. Automated Customer Account Transfer Services (ACAT Transfers) If you want to transfer the stocks from Robinhood to another account, you have to do the ACAT ( Automated Customer Account Transfer Services) transfers. It will help you to transfer your Robinhood holdings to get a transfer from your account with ease if you have any brokerage requirements for the fund transfer. On the other hand, Webull will not allow any kind of transfer of the stocks unless the account or the name of the accounts are identical to the new account created in the Webull app. This is because any kind of difference in the account name and type can cause a delay in the transfer process. How Long Does It Take To Transfer Robinhood To Webull? The entire transfer process from the Robinhood to Webull nearly takes 5-7 working days to make a transfer if your procedure and the account type all are correct. Otherwise, it can take longer days to transfer the assets from one account to another account. Partial Or Full Transfer Robinhood allows both the partial and the full transfer of money or the stocks. But your account will be restricted once you have made the full transfer. It is done to make your process of transfer smoother and effective. Your account will be closed once all the assets from Robinhood are transferred. However, if you want to do the partial transfer, your account will remain open and not get closed. You have to weigh between the costs and benefits when you want to transfer stocks from Robinhood to Webull. How To Transfer Stocks From Robinhood To Fidelity? You should follow certain simple steps if you want to transfer from Robinhood to Fidelity. And, you will get the answer to the question of how to transfer stocks from Robinhood to Fidelity for that you need to follow Some of the core steps are as follows:- You have to pay $75 as the charge fee when you want to transfer money from Robinhood to Fidelity. Make use of the ACAT transfer service to transfer the assets of the amount of this stock. You have to share your Robinhood Securities account number with Fidelity to transfer stocks through this platform. It can be any IPO stocks as well. These are some of the crucial steps you have to follow while you want to transfer stocks using Fidelity. Final Take Away Hence, if you can follow the above steps, you will know how to transfer stocks from Robinhood to Webull. You just need to follow the steps judiciously to achieve your objectives quickly. You need to work out your plans well before making your investments in the stocks. FAQ( Frequently Asked Questions) How much time does it take to transfer the stocks from Robinhood to Webull? The stock transfer usually takes 5-7 business days to make the transfer of the stocks from your Robinhood account to webull account. Can you transfer stocks to Webull? Both the partial and full transfers of stocks are possible through this exchange platform. Does Webull Cover transfer fees? Webull will refund your fee at the right time so that it can help you to achieve your objectives and the goals in the correct manner. Read Also: Why Create A Powerful Business Continuity Plan? How To Start A Business In 2021 – Best Business Strategies Is Nykaa Going To Dominate The Market With Their Recent Launch?

Dec 08, 2021