Instant Loan App: Top 25 Best Loan Apps Should You Know In 2023

With the rise in the level of digitization, there has been a simultaneous rise in the number of instant loan apps in the last few years. As per various sources, in the year 2022 itself, the demand for personal loans surged by 50% in the retail industry. However, a very interesting fact is that in the disbursement of personal loans, non-banking financial institutions were on top of banks.

In this article, we will mainly discuss the top twenty-five instant loan apps that offer personal loans in 2023. These are the best loan apps that will allow you to avail of loans fast. However, these apps come with different types of service options, and the time of disbursal changes with the app. Hence, to get fully informed, read on through to the end of the article.

The Best 25 Instant Loan Apps In 2023

The following are the best instant loan apps that you must look for before you try to avail yourself of personal loans fast in 2023:

1. Earnin

If you are qualified to get loans in this app, you can get an emergency loan from this app if you are confident to pay it back. The advances are large.

2. Chime

This is one of the best $50 Loan Instant Apps if you are looking for payday loans. However, lenders can still charge high interest.

3. Current

The best thing about this app is that there are no overdraft fees associated with it. Furthermore, you can get overdraft protection of $200.

4. MoneyLion

You can get an instant cash advance of up to $300 dollars, and you can also be able to access and improve your credit score.

5. Brigit

This is one of the best cash advance apps. If you are an eligible member, cash advances are available to you between #50 and $250.

6. Dave

This is one of the best $100 loan instant apps that you will come across. Cash advances start here at only $5, and there is also automatic overdraft protection.

7. Spotloan

Once you do a SpotLoan login, they will inform you, “It’s an installment loan, which means you pay down the balance with each on-time payment.” It means that it is not a payday loan app.

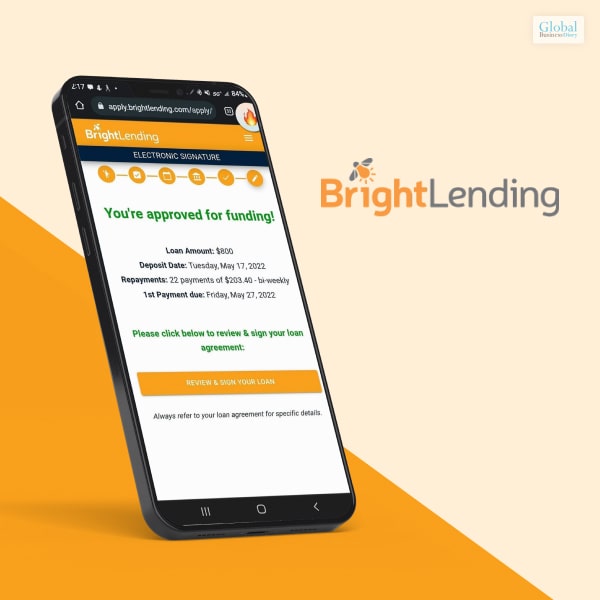

8. Bright Lending

You can get loans from $300 to $1000, but there are also triple-digit APRs, as well as short terms for repayment.

9. Cash App

How to borrow money from Cash App? The Cash App borrow loan services allow you to use the app and access loans from multiple devices using the tag “$cashtag”.

10. MoneyLion

With the help of Moneylion NYC, you will be able to avail of credit-builder loans without a credit check if you are a member.

11. SoFi

The best thing about this loan app is that you can get even $5000 to $100,000 loans and can get your funds on the same day.

12. PayActiv

You can get here early paycheck access, and also you will be able to get up to 50% of earned wages before your payday.

13. Even

If you are eligible, you can get up to 50% of your earned wages early, and you can get budgeting tools to track your spending as well.

14. Branch

Apart from getting 50% of your earned wages early, you will also benefit from no credit checks and zero-cost loans.

15. Grain

If you have low credit scores, then this is one of the best loan apps for you. This is also great if you have a short credit history.

16. Vola

If you are able to pay a monthly fee, with the help of Vola, you can permanently avoid overdraft fees with the help of instant cash advances.

17. Empower

Borrowing a small number of finances can be easy with the help of the Empower Loan App. Furthermore, there are budgeting tools to track expenses.

18. CLEO

The app uses AI to help you analyze your spending and help you by giving actionable insights as well. You can also avoid overdraft charges with the help of rewards and auto savings.

19. SoLo

Once you apply for a loan here, you will get a soft credit check, which will not affect your credit score. However, based on the credit check, lenders will have a better idea in regards to lending their money to you.

20. Upgrade Personal Loans

You can get fast loans with Upgrade, You can get loans up to $50,000. However, there is a high origination fee associated with the borrowing.

21. Varo

Apart from being a loan app, this is also a bank account, which gives you an account with a minimum balance with no monthly charges or overdraft. Furthermore, the credit card option is also secure.

22. Albert

According to Business Insider, “Albert is a financial app offering automatic savings tools, cash accounts, cash-back rewards, auto-investing, and much more.” However, you can get some customer service issues, as per complaints of borrowers.

23. LendJet

Although not a direct lender, you can get access to a variety of lenders through this platform. Hence, it will be easier to look for personal loans from various options.

24. ZippyLoan

Like the other platforms, ZippyLoan also offers you to choose from a variety of lenders. You can get loan amounts from $100 to $15,000.

25. Viva Payday loans

You can apply for loans in this app without having a credit history for yourself. The loans are hassle-free, and you will get fast approvals as well.

Summing Up

Hope this list is informative enough to give you a better idea of the best instant loan apps in 2023. If you are trying to avail of fast loans, then you must try one of these apps mentioned above to get the best services. However, we will still recommend you read all the information related to availing of loans.

This will give you a better idea of what services are offered by the loan app that you are taking a loan from. Which of the aforementioned loan apps do you think is the best option for you? Share your reviews with us in the comments section below.

Read Also About:

Tags:

Recent

Time Matters: The Role of Early Hazard Detection in Industrial Safety

Jan 20, 2026

Hidden Ignition Risks in Industrial Environments

Jan 17, 2026

Critical Thinking Exercises in the Digital Age and Emotional Intelligence Integration

Jan 14, 2026

Why Strategic Partnerships Matter More Than Ever

Jan 13, 2026

Related Articles

Need Help with Tax Debt? Check Out These Relief Options

Meta Description: The IRS provides relief options for tax debt, including installment plans, penalty relief, and offers in compromise, but beware of scams. You might feel stressed and overwhelmed if you owe money to the IRS. How can you pay off your tax debt and avoid penalties and interest? You might also worry about losing your property or facing legal action. But don't panic. Fortunately, some relief options are available for taxpayers struggling with tax debt. These options can help you reduce your tax liability, set up a payment plan, or even settle your debt for less than you owe. This blog post will explain some of the most common relief options and how they work. Hire a Tax Relief Company for Assistance (But with Caution!) This is the first thing you can do to save your back from IRS debts. The process of applying for tax debt relief programs can often be overwhelming for those who don’t have a good understanding of accounting and tax-related terms. Working with a reputable tax relief company like https://globalgatecpa.com/ will genuinely help you if you don’t understand the process or need assistance filling out forms. However, you should carefully consider this decision, as scams and fraudulent tax relief companies are looking to take advantage of your vulnerability. Here are some things to keep in mind: If the company loses or delays your application, you're still responsible for your tax debt, interest, and penalties with the IRS. Some companies may charge an upfront fee, surpassing the potential savings on your tax bill. Be cautious of any company that demands payment before work is done, as this is a red flag for potential scams. Also, don’t work with a company who are - guaranteeing debt reduction or elimination promising your tax debts will be forgiven not reviewing your financial situation thoroughly The Federal Trade Commission advises taxpayers first to try to settle their tax debt directly with the IRS before seeking the assistance of a tax relief company. If you have concerns or suspect you've fallen victim to fraud, file a complaint with the FTC. A free tip: If you owe less than $10,000, you can tackle the matter yourself. If you owe over $10,000, hiring an expert to negotiate with IRS can help you get better terms. What Are the Relief Options for Tax Debt? The IRS offers several relief options for taxpayers with trouble paying their tax debt. Some of these options are: 1. Installment Agreement You have the option of selecting from two different types of installment agreements (IAs), both of which provide you with additional time to settle your tax debt: Short Term Plan If you owe the IRS less than $100,000, you can apply for a payment plan with up to 120 days to pay off the balance. You can apply through different methods, such as online or by phone, without fees. Once approved, you can pay through credit/debit card, money order, check, online, or by phone using the Electronic Federal Tax Payment System (EFTPS). Long Term Plan Consider a long-term payment plan if you owe the IRS less than $50,000 (including extra fees) and can't pay it off in 120 days. This plan lasts for 72 months, and you can either make payments directly every month or through automatic debit withdrawals. However, you must make automatic debit withdrawals if you owe more than $25,000. The amount you need to pay to set up the payment plan depends on how you want to make payments. If you pay directly using a money order, Direct Pay portal, or EFTPS, the fee is $130 if you apply online or $225 if you apply by mail, in person, or by phone. If you're a low-income taxpayer (earning an adjusted gross income at or below 250 percent of the federal poverty level), you may get a $43 reimbursement for the setup fee. If you choose automatic debit withdrawals, the fee is only $31 if you apply online or $107 if you apply by mail, phone, or in person. You might also qualify for a fee waiver if you're a low-income taxpayer. Note that both payment methods don't stop the interest and late payment penalties from accumulating until the balance is fully paid. 2. Currently Not Collectible Currently, not collectible (CNC) status is a temporary relief option that suspends the IRS's collection activity if you cannot pay your tax debt. You can request “currently not collectible” status by calling the IRS. The IRS will ask you to fill out a form called Collection Information Statement for Wage Earners and Self-Employed Individuals or Collection Information Statement to confirm your financial situation. You will have to provide proof of your financial hardship and show that paying your tax debt would cause significant hardship for you or your family. The IRS will review your income, expenses, assets, and hardship circumstances to determine if you qualify for CNC status. If the IRS grants you CNC status, it will stop sending you notices and taking enforcement actions against you. However, you will still owe your tax debt, and interest will continue to accrue, but the IRS will not levy your income or assets or file a tax lien against you. Remember, this is just a temporary solution, not a permanent one! 3. Offer in Compromise The Internal Revenue Service (IRS) is known to be stringent in forgiving tax debts, but taxpayers may apply for an "offer in compromise" to settle their liabilities for less than the full amount owed. However, such arrangements are typically only granted to individuals genuinely experiencing financial hardship, such as those who have incurred substantial healthcare expenses or lost their jobs with limited prospects of generating income in the future. Although exceptions do occur, these situations are relatively rare. Taxpayers to be realistic about their circumstances. For example, those who possess assets and earn a significant income are unlikely to receive tax relief. To apply for an OIC, you must fill out Form 656, Offer in Compromise, and Form 433-A (OIC), Collection Information Statement for Wage Earners and Self-Employed Individuals. You can also apply for tax credits available to small businesses. Fill out Form 433-B (OIC), Collection Information Statement for Businesses to avail that. You must also pay a $205 application fee and a 20% deposit of your offer amount. These are non-refundable even if your application is rejected! Conclusion Managing your tax debt is essential to maintain a healthy balance between your personal and work life. However, it can badly affect your financial well-being and peace of mind. The three relief options discussed in this post can help you resolve your tax debt and get back on track with your taxes. To choose the best option for your situation, you should review your tax records and financial information, compare the pros and cons of each option, and contact the IRS or a tax professional for guidance and assistance. Read Also: Why Create A Powerful Business Continuity Plan? What Is Network Marketing And How To Do It In 2021 Virtual Data Rooms: What They Are And Their Critical Importance For Businesses

Apr 10, 2023

How A Student Loan Debt Financial Advisor Can Help You?

Navigating the complexities of student loan debt can be a daunting task for many. With various repayment plans, refinancing options, and forgiveness programs available, it's easy to feel overwhelmed. This is where a student loan debt financial advisor comes into play, offering tailored advice and strategies to manage your loans effectively, save money, and reduce stress. By understanding the role of such an advisor, you can make informed decisions about your financial future and take control of your student loan debt. Understanding Your Student Loan Portfolio A financial advisor specializing in student loans can provide a comprehensive analysis of your entire loan portfolio. They can help you understand the details of your loans, including student debt interest rates, balance amounts, and repayment terms. This deep dive into your loans is crucial for crafting a personalized repayment strategy that aligns with your financial goals and situation. Advisors can identify opportunities to consolidate or refinance your loans, potentially lowering your interest rates and monthly payments. Moreover, they can explain the differences between federal and private loans, and the implications of each on your repayment plan. Understanding these distinctions is vital for making informed decisions, such as whether to pursue federal loan forgiveness programs or to refinance through private lenders. This foundational knowledge is the first step towards managing your loans more effectively. 1. Strategizing Repayment Plans One of the most significant ways a financial advisor can assist is by helping you choose the best repayment plan. Whether you're aiming for loan forgiveness under programs like Public Service Loan Forgiveness (PSLF) or trying to minimize interest costs, an advisor can guide you through the complexities. They can simulate various scenarios to show how different repayment plans affect your long-term financial health, taking into account factors like income growth and life changes. Advisors are also adept at identifying eligibility for income-driven repayment plans, which can significantly reduce monthly payments for those who qualify. They understand the nuances of each plan and can help you navigate the application process, ensuring you're taking full advantage of available options to manage your student loan debt efficiently. 2. Navigating Loan Forgiveness And Discharge Programs Loan forgiveness and discharge programs offer pathways to eliminate student loan debt under specific conditions, but they come with their own set of rules and requirements. A financial advisor with expertise in student loans can help you understand if you qualify for these programs and guide you through the application process. They can provide invaluable advice on how to maintain eligibility for forgiveness programs over time, such as ensuring you're in the correct repayment plan and fulfilling any employment requirements. Additionally, advisors can help you understand the tax implications of loan forgiveness, preparing you for potential financial impacts down the line. Their guidance can be crucial in avoiding common pitfalls that disqualify applicants from forgiveness, ensuring you remain on track towards achieving your goal of loan discharge. 3. Refinancing And Consolidation Strategies Refinancing and consolidating student loans can be an effective strategy for reducing interest rates, lowering monthly payments, or simplifying repayment by combining multiple loans into one. However, these options are not suitable for everyone. A financial advisor can help you weigh the pros and cons of refinancing or consolidating your loans, taking into account your specific financial situation and goals. They can also assist in finding reputable lenders, comparing offers, and understanding the long-term implications of refinancing, such as losing eligibility for federal loan benefits. This tailored advice ensures you make a decision that's in your best interest, potentially saving thousands of dollars over the life of your loans. 4. Achieving Financial Freedom Managing student loan debt effectively requires a comprehensive approach that considers your entire financial picture. A student loan debt financial advisor is equipped to guide you through this process, offering strategies that can save money, reduce stress, and ultimately lead to financial freedom. Their expertise can be invaluable in making the most of your repayment options, navigating forgiveness programs, and achieving your financial goals. With the right advice and support, you can take control of your student loan debt and pave the way for a brighter financial future. Role Of Financial Advisor In Managing Student Loans There are several roles in financial advisor that can help you to manage the student loans with complete ease. Some of the key factors that you must know at your end are as follows:- 1. Loan Repayment Strategies A financial advisor can help you develop a repayment strategy that aligns with your financial goals and circumstances. They can explain different repayment plans, such as income-driven repayment plans, and help you choose the best option. Make application of the loan repayment strategies that can boost the chances of your brand value in correct order. Ensure that you follow the correct way that can assist you in reaching your objectives. 2. Debt Consolidation If you have multiple student loans, a financial advisor can advise you on whether consolidating them into a single loan could be beneficial. They can help you understand the pros and cons of consolidation and how it may impact your overall financial situation.Debt consolidation can help you in reducing the chances of your expenses to a greater level. It can offer you a mental peace at the time of crisis. 3. Budgeting & Financial Planning A financial advisor can help you create a budget that allows you to manage your student loan payments while also meeting your other financial goals. They can provide strategies for saving, investing, and managing your money effectively. 4. Loan Forgiveness Program If you qualify for loan forgiveness programs, such as Public Service Loan Forgiveness (PSLF) or Teacher Loan Forgiveness. A financial advisor can help you understand the requirements and maximize your chances of qualifying. An advisor can opt for the loan forgiveness program that can help a student to seek for immediate loans. 5. Interest Rate Management A financial advisor can help you understand how interest rates affect your student loans and provide strategies for managing them, such as refinancing at a lower rate if possible. You can make use of the interest rate management that can boost the scope of your brand value. 6. Financial Education Beyond managing student loans, a financial advisor can provide education on various financial topics. It comprises such as credit management, investing, and retirement planning, to help you build a solid financial foundation for future. You must ensure that you follow the best process that can make things easier for you. Final Take Away Hence, the above factors can help you in meeting your goals with complete ease. You must ensure that you follow the right process that can make things easier for you in reaching your objectives. You can share your views and comment in our comment box. This can assist you in reaching your goals with ease. Try to follow the best solution that can make things easier for you in attaining your requirements with ease. A financial advisor can provide personalized advice and support to help you effectively manage your student loans and achieve your financial goals. They can offer you the perfect solution that you require from your counterpart. Read More: Evolution Of Fintech: A Complete Story Of Start To Rise The Future Of Money: An Insight To Money’s Transformation Global Fintech Companies Of 2024: Everything You Should Know About

Feb 23, 2024

What Is Net Operating Income? How To Calculate NOI?

Net operating Income is a valuation method. If you are a real estate professional, then you have to calculate it. It will help you in the determination of the income-producing properties For the calculation of NOI, Operating expenses need to be deducted from income a property generates. Most of the time, people often get confused between the concepts of Net Income and Net operating income. Net Operating Income will help you to know the capacity of the property to generate revenue. What Is Net Operating Income? Net operating Income helps you to calculate the profitability of an asset. It can be an income from an investment as well. After subtracting the operating expenses from Income, you will get net operating income. Most of the time, this parameter is used in the real estate industry. In order to determine the profitability of investment properties such as apartment complexes, warehouses, and buildings, this Net Operating Income is used. You can get the similar information in Investopedia. What Is The Net Operating Income Formula? You have to follow the simple Net Operating Formula to calculate the Net Operating Income. Let’s go through it once. Most of the time, for making an accurate valuation of commercial real estate, the Net Operating Income Formula is taken into consideration. You cannot ignore this fact from your end. Net Income Formula For Managerial Accounting The Net income formula for managerial accounting involves the following calculation methods:- Net Income = Total Revenue -Total Expenses Net Operating Income vs Net Income Net Operating IncomeNet IncomeNOI is a metric typically used in the context of real estate and investment propertiesNet Income, also known as Profit or Earnings, is a fundamental financial metric used in the context of businesses, not just limited to real estate.It represents the income generated from the property's operations before accounting for taxes, interest, depreciation, and amortization (known as EBITDA). It represents the profit a company makes after deducting all expenses, including operating expenses, interest, taxes, depreciation, and amortization (known as EBITDA). The formula for calculating NOI is: NOI = Total Revenue - Operating ExpensesThe formula for calculating Net Income is: Net Income = Total Revenue - Total ExpensesOperating expenses include items like property management fees, maintenance costs, property taxes, insurance, and other day-to-day operational expenses.Total expenses include operating expenses, interest payments on debt, income tax, and depreciation or amortization. Are Operating Income & Operating Revenue Same? Operating revenue is not the same as operating income. Operating revenue signifies the total cash inflow from your primary income-generating activity. After subtracting the cost of doing the business, the leftover income is the operating income. It is the primary form of difference between the two concepts. Operating income calculation is completed from the gross income depreciation, and amortization from the gross profit is deducted. Operating expenses are the expenses that involve administrative costs, rent, and supplies. If you want to calculate the gross profit, you need to calculate the Cost Of Goods Sold from the revenue. It is almost similar to the calculation of marginal cost. Benefits Of Calculating Net Operating Income There are numerous benefits to calculating the net operating income for your business. Now, you may be wondering what can be the benefits of calculating the Net Operating Income. Let’s dig deep into the details to have better insights into it. Its process of calculation is almost similar to that of the current ratio formula. 1. Profitability Assessment NOI offers you clear insight into operating profitability. When you subtract the property’s operating expenses from the gross rental income, you will get a clear idea of how much money the property is generating before the calculation of the taxes and financing. 2. Comparative Analysis Investors can use NOI to compare the financial performance of different properties. This comparison allows them to identify which properties are more profitable and make informed investment decisions. Investors need to identify the financial performance of the property before buying it. Net Operating Income can leverage the value of your property. 3. Valuation It is one of the primary components in determining the value of the property. You can estimate the value of the property after dividing it by its capitalization rate. It will be easier for you to make an accurate estimation of the market value of the property. Try to make things easier from your end. 4. Financial Planning Property owners can use NOI to create budgets, assess ongoing financial performance, and plan for the future. Understanding the NOI helps in making decisions related to rent increases, cost management, and property improvements. It is one of the basic purposes of making the calculation of NOI. It can benefit you on a pro-rata basis as well. 5. Financing Lenders often use NOI to assess the financial viability of a property and determine the amount of financing they are willing to provide. A higher NOI can lead to more favorable financing terms. You need to make the financial planning in the perfect order while attaining your requirements. 6. Income Tax Planning NOI can have implications for income tax planning. Property owners need to understand the taxable income generated by their property. It can be different from the NOI due to factors such as depreciation. In accounting terms, Depreciation reduces the value of the assets to a considerable extent. You need to get through these facts before the NOI calculation. 7. Risk Management When closely monitoring NOI, property owners can identify changes in the financial performance of a property. This allows them to address issues promptly, such as rising expenses or declining rental income, to mitigate financial risks. You need to identify the areas where Non-Operating Income can be of great help to you. 8. Investors Confidence The confidence of the investors depends largely on the operating income. Most of the time, we miss out on this fact at the time of selling the property to its investors. When investors and stakeholders have access to accurate NOI figures, it builds confidence in the property's performance. It can attract potential investors or partners. Final Take Away Hence, if you do not calculate the operating income, then you cannot get the correct insight into the accurate estimation of the property. You must not make your selection on the wrong end. Proper application of the NOI calculation can make things easier for your valuation. You can share your views and comments in our comment box. It will help us to know your take on this matter. You cannot make any kind of compromises in this regard while you calculate real estate property. Read More: Marketing Campaigns: How To Do It? – Steps To Follow Market Orientation – What Is It, And How Does It Work? Market Cannibalization – Definition, How Does It Work, Example, And More

Oct 04, 2023

Biggest Stock Market Crashes In The World History

The stock market is a triangle industry where a crash takes place when the market value drops in a series. It will be tough to provide a generalized definition of the stock market crash, but it may occur when the price drops more than natural. When the market price decreases and losses 10% from the current value, then people can consider this event as the “great depression.” In 1929, the marketing industry got 34%. A market crash takes place suddenly. But when it starts falling down, you may know that this is going to be cashed soon. Approximately 25% of workers lost their jobs due to this destruction in the market. If you are a stock market investor, the market crashing history can provide you with a primary imagination about the stock market. We will tell you how the whole industry flows to the veils in a short period of time. You will learn the history as well as the economy of the stock market world. It took 5 to 10 years naturally to get back to the previous stage. What Is The Stock Market Crash? As I have mentioned earlier, it is challenging to offer a generic definition of the stock market crash, but we can tell it is the rapid change of the price in the market. Before crashing a market, the stock market industry always reaches its peak, and from that point, it suddenly drops to the ground. Generally, stock market crashes happen in a short time period. For example, the price is normal today, and after nightfall, you may see the price drop down to 12%. This is how the market crashed. If you consider the whole system as a pyramid, you will see in a long time, the price is rising to the top and after reaching its catastrophic position, it suddenly drops. You, as an investor, can predict the market crash beforehand. When the price is increasing, you have to keep it in mind. However, it will go down all of a sudden. From the steady rising, it comes to the ultimate drop. This is a stock market crash. Also Read: Angel investors - Overview, pros and cons in 2021 Indications Of Stock Market Crash When you are a long-term investor, you have knowledge of the stock market. If you have ever followed, will see in a specific time, the market growth is going as a bounce. At this time, you can make an assumption about the market crash. There are more things about the market that you can follow. When you are in the stock market business, always stay alert and invest money after looking at all aspects. Therefore, let’s get started with the major indications. Drastic Speculations. Stagnant Market Value. Low-Interest Rates. Catastrophic Illusion. Slow Growth Rates. Exceptional Market value. These are all the things that you can follow through so that you can make an assumption. However, keep all these things in your mind and then step towards your goal. The Biggest Market Crashes In World History In world history, many times the market fails and for that thousands of people lose their jobs. You will be surprised to know that after the market crash in 1929, a total of 10% of people lost their jobs. Generally, there is always a balance between the economy and the stock market industry. When the stock market industry gets injured, it affects the economy on a large scale. Many times, many incidental cases happen in the stock market industry. For the time being, let’s get up to date with the large world history of stock market crashes. Black Tuesday Of 1929 One of the major stock market crashes began on 24th October 1929. Although there are some confusions about this theory. Some authorities have opined that the fall began on 18th October. The same condition went on till 29th October. Mass hysteria was created when a total of 12,894,650 shares were traded. When the price started falling, people tried to get their money out, and for this reason, chaos was also created. The market first opened with 11% lower than the average. At this time also, people never think that the market will crash. This happened in the next few days when it got more decreased. Before starting the black day, the market reached its last peak position on 3 September. The situation was not like the previous devastation. Though later it became like that, and mass curiosity was also one of the main reasons. Black Monday Of 1987 In the year 1987, the market started decreasing. After then, this became devastating for the stock market investors. At that point in time, Dow jones’s market value got decreased up to 22%. Still, now this situation is remarked as one of the major incidents in the world history of the stock market. From 19th October, the market value started decreasing, and it reached the lowest stage in November. The market lost its stock, and the market value also decreased 20% from the average value. It is said that there were many investors that could manage themselves to get out their stocks. Whenever this type of incident takes place, you may see the mass hysteria that makes the incident more ridiculous. The same thing happened in the 1987 market loss. This grand loss took years to get the scenario back. The professional marketers have said later that this incident took place because of the computing trading and as well as for the middle investors. Many of the investors do not even accept these things as the prime reasons, though. It never drops off, only for computing trading and for the trade deficit. Dot-Com Bubble Of 1999-2000 This dot-com bubble incident took place almost thirty years ago. This is why it is far away from the other types of incidents. You may know this incident from the NASDAQ composite index. Many of the investors inculpated the online market agencies that created chaos among people. The technology-dominated services created mishaps, and that probably deals the case to the deeper loss. The surge was in 1995 approximately 100 that had increased upto 500 in 2000. From this point in time, the bubble started bursting. Behind the screen, there was a large lake that later came in front. The overvalued stock was also one of the main reasons for this dot-com bubble case—this time. People just hold their stocks. And when the market value decreased, they all started selling, and the mishap took place. If they sell the stock at the peak point, then may this incident never happen. This market value remained like that for a long time. It took years to get back to the previous stage of the stock market. The Stock market is sensitive, and that is why people need to manipulate the channel properly. When any mishap happens, the whole chain breaks off. Stock Market Crash Due To Covid-19 It is the most current stock market crash that happened, and even its effect is still going on the economy. From the country-based loss, it spread to the international loss. All countries got economic harm from this current market crash. At the present time, there has been an increase in the number of digital investors that are paying in this market chain through online facilities. From February onwards, the market started crashing, and that decreased upto 11% to 13% on average. You will be surprised to know from 1987 to the current time; it is the major drop in the history of the stock market. Before this, the situation never happened like this. The market plunged deeper day by day. Even in the present situation in 2021, the same thing is going on. The prior amounts and the investment were taken away, but the middle watts remained locked. In the stock market, people spend millions of dollars that the authority has driven out. But still, the mediocre investor's money got stuck. Due to the pandemic, this marketing scenario is a bit different from other creases. The prior reason behind this market falls in the unknowingness of people. The business investors and the dealers had no idea about the future going situation, and that is why they took back their stocks. This time, the market goes to the grand fall in a different manner than has a prior reason to fall back. The Dow declined 9.99% in March. Trillions of dollars are still stuck in the market. But it has no straightforward declaration of the market. We hope this situation will also be overcome at the end of the pandemic situation. Effects Of Stock Market Crashes When the stock market is running well, you will see the economy is also growing. In major cases, when the stock market gets stuck, the economy of the country also gets hampered. On the other hand, the stock market is a large industry where millions of people are investing; some are working on the online trading market. Those who are working on the stock market can lose their jobs when the whole industry breaks down. When you invest in the stock market, you have to keep in mind you are going to get a profit from the investment. If the market crashes, then you will never get your profit. The price drop means, in the literary sense the less revenue. And when the revenue is decreased, the investor will receive a bad impact. Through this, people get great depression. The depression situation took place in the previous years. You may take a look at these times. Also Read: How To Make Money Fast - 5 Strategy To Follow In 2021 Frequently Asked Questions (FAQs) You may have questions regarding stock market investment. So, let's get you covered with all aspects as well. Firstly, let’s tell you, when you are thinking of the stock market investment, you have to remove the negative thoughts. Now, take a look. Q1. Is It Worth Investing In The Stock market? Ans. Investment in the stock market is a good decision. If you are new in the industry, you may face difficulties. The stock market has an option of earning double the amount from the investment. Experienced investors generally get more profit from their investment. Don’t worry; you will get the same opportunity after learning more things about the stock market. Q2. Which App Is Best For The Stock Market? Ans. You can use NSE mobile software for trading. Except that you can go through the NDTV profit, IIFL markets, etc. You can also buy stocks online with trusted brands like eToro. It's easy to learn how to buy stocks on eToro by simply following their guides. Also Read: 10 Best Investment Apps For 2021 Q3. Is The Stock Market Safe To Invest In? Ans. It is difficult to answer properly. We can tell you that you have to be aware of the market when you will pay. So, start investing today and wait for the profit. If you find difficulties, you can go through the solutions as well. But never ever stop dreaming about getting the best profits. Q4. What Is The Best Stock Market To Invest In For Beginners? Ans. There are many investment options. Worldwide, there are many companies finding investors. You append your money there. You can spend money on Amazon, Alphabet, Apple, Facebook, Mastercard, etc. however, you have to start investing from today. The Bottom Lines These are all the relevant factors that you need to know before starting an investment in the stock market. Whenever you start investing, make sure that you will be serious about the market factors. The price can increase as well as decrease, so stay aware of the fact. In addition, we will tell you, try to think of the best things not following the backlogs. When you are doing a business, there is always a chance of loss, but you have to focus on the positive things. Only then will you be able to get the best fruit from trading. Read More: How to start a business in 2021 - Best Business Strategies Top 10 Successful Serial Entrepreneur Of All Time - 2021 Updates Top 10 Best B2B Marketing Strategies For The Entrepreneurs In 2021

Sep 13, 2021