What Is The Leverage Ratio And How to Calculate It?

Leverage ratio is a tool for businesses that helps to determine the extent to which a particular business depends on debt to purchase assets and build capital. On the one hand, it helps businesses determine their own capability to secure funding. On the other hand, the leverage ratio helps investors and lenders evaluate the ability of a business to meet its financial obligations after securing capital.

In this article, you will learn about leverage ratio in general and how it works for businesses as well as investors and lenders alike. We will also share with you details on how to calculate the leverage ratio formula of different types of leverage ratios. Finally, you will learn about the importance of the leverage ratio and how it applies to businesses. Hence, to learn more, read on through to the end of the article.

What Is The Leverage Ratio?

According to Investopedia,

“A leverage ratio is any one of several financial measurements that look at how much capital comes in the form of debt (loans) or assesses the ability of a company to meet its financial obligations. The leverage ratio category is important because companies rely on a mixture of equity and debt to finance their operations, and knowing the amount of debt held by a company is useful in evaluating whether it can pay off its debts.”

Basically, the leverage ratio is a set of ratios with the help of which you can highlight the financial leverage of a business when it comes to assets, liabilities, and equities. The ratio gives you an idea of how much of the capital of a business comes from its debt. Hence, you will get a good idea of whether the business makes well for its financial obligations.

Read More: Network Marketing: What Is It? Is It The Right Option For You?

How Does Leverage Ratio Work?

According to Hubspot.com,

“A higher financial leverage ratio indicates that a company is using debt to finance its assets and operations — often a telltale sign of a business that could be a risky bet for potential investors. It can mean that earnings will be inconsistent, it could be a while before shareholders can see a meaningful return on their investment, or the business could soon be insolvent.”

These metrics are really useful for creditors and investors to find out whether they should extend credit to or invest in the business. If the financial leverage ratio of a company is very high, it means that the company is allocating most of its cash flow to pay off its debts and is more prone to default on loans.

On the other hand, if the financial leverage ratio of a business is low, it shows that the business is financially responsible and has a steady stream of revenue. Even if a company is in significant debt, having a good financial leverage ratio shows that there are minimal risks for investors and creditors, and the business is likely worth an investment.

Leverage Ratio – How To Calculate It?

The following are the different formulae of leverage ratios based on the type of ratio you want to choose:

1. Operating Leverage Ratio

You can calculate it using this formula:

| Operating Leverage Ratio = Percentage change in EBIT (earnings before interest and taxes) / Percentage change in Sales |

2. Net Leverage Ratio

Here is the formula to calculate this ratio:

| Net Leverage Ratio = (Net Debt – Cash Holdings) / EBITDA (Earnings before Interest, Taxes, Depreciation, and Amortization) |

3. Debt-to-EBITDAX

You can calculate EBITDAX using this formula:

| EBITDAX (Earnings before Interest, Taxes, Depreciation, and Amortization before Exploration Expenses) = EBIT (Earnings before Interest and Taxes) + Depreciation + Amortization + Exploration Expenses |

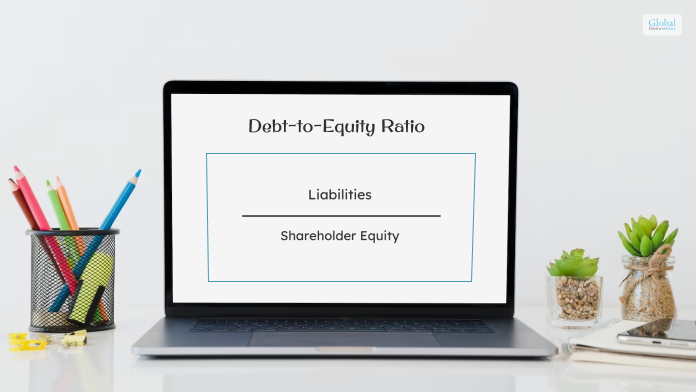

4. Debt-to-Equity Ratio

Here is the formula to calculate this ratio:

| Debt-to-Equity Ratio = Liabilities / Stockholders’ Equity |

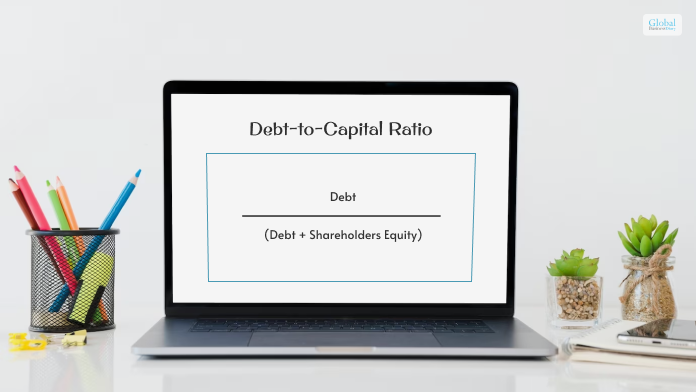

5. Debt-to-Capital Ratio

You can calculate it using this formula:

| Debt-to-Capital Ratio = Debt / (Debt + Shareholders Equity) |

6. Debt-to-Capitalization

Here is the formula to calculate this ratio:

| Debt-to-Capitalization Ratio = (Short-term Debt + Long-term Debt) / (Short-term Debt + Long-term Debt+ Shareholder Equity) |

7. Interest Coverage Ratio

You can calculate it using this formula:

| Interest Coverage Ratio = Operating Income / Interest Expenses |

8. Fixed-Charged Coverage Ratio

Here is the formula to calculate this ratio:

| Fixed-Charged Coverage Ratio = EBIT (Earnings before Interest and Taxes) / Interest Expense of Long-term Debt |

By having a good idea of your leverage ratios related to a business, you might understand how the business can run in the near future.

Why Is Leverage Ratio Important?

According to the Wall Street Mojo,

“Leverage ratios are important as they allow investors to assess a company’s financial position with respect to its financial obligations. Though firms have an option of using their equity to purchase assets and resources for undertaking different business activities, they go for taking up loans to finance their capital building. The reason is one – the cost of debt or cost of borrowing is way less than the cost of equity.”

The different types of leverage ratios help investors get a better idea of how the business’s capital flow is structured. By calculating these ratios, you can have information about a company in regard to whether it can take advantage of its leverage or not.

For example, if the company you want to invest in or lend credit to has taken too much debt, it is obviously risky for you. On the other hand, if the leverage ratio is too low and the company does not have any debt, it will be able to pay off too much cost of capital and reduce its earnings in the long run. Hence, consider your choices carefully.

Read More: Project Management: What Is It? – Major Types, Examples, And More

Wrapping Up

Hope this article was helpful for you in getting an understanding of how a leverage ratio works. You can see here that this is one of the major financial tools with the help of which you can assess a company’s ability to meet its financial obligations. By using it to measure operating expenses, you can get an idea of how differences in output can change operating income.

The debt-equity ratio, equity multiplier ratio, degree of financial leverage, and consumer leverage ratio are some of the common leverage ratios. Do you have any more information to add regarding how to calculate the leverage ratio? Share your ideas and opinions with us in the comment section below.

Read More:

Tags:

Recent

Why Business Intelligence Exercises Are Important for Effective Data Analysis

Feb 22, 2026

The Hidden Cost of Dirty Curtains: More Than Just an Eyesore

Feb 20, 2026

Strategic M&A: Turning Opportunity Into Lasting Value

Jan 24, 2026

Beyond the Box: What a Shipping Container’s Journey Reveals About the Supply Chain

Jan 23, 2026

Related Articles

Financial Planning Tips For Different Stages Of Life

Let us tell you something that can change your perspective on handling finances. It may sound cliché, but it has never been truer than ever – planning always pays off regardless of where you are in your life right now. Did you know that taking control of your hard-earned cash at every stage of your life could greatly impact where you want to be financially? That's right; we are talking about the concept of financial planning for different stages of your life. From embracing adulthood to reaching old age, here's why it matters so much! You go through different stages in your life and might encounter new challenges and goals at various points along the way. So, whether you are a government employee, just graduated from school, hit mid-life stability, or are getting ready to kick back in old age, understanding the nuances of your journey will help you make smarter decisions when it comes to your finances. And guess what? We have got you covered with all things related to financial planning across these distinct life phases. Are you ready to take charge and start building your roadmap to prosperity? Buckle up because our next stop is where the magic happens! 1. Employment The nature of your job plays a crucial role in financial planning. Every organization offers different benefits, including insurance options and provident funds. However, financial planning for Govt. Employees may involve in some particular issues. You might have chosen this career path due to the attractive benefits packages offered, including comprehensive healthcare coverage and generous pensions. Still, you may also confront special financial issues specific to government employment. Let's take a closer look at some crucial variables to bear in mind when budgeting your money. A. Benefits Evaluation (Healthcare & Pension Plans): When comparing private sector positions to government jobs, the latter typically offers competitive salaries alongside robust benefits packages. Adequately assessing all possibilities within healthcare and pension options allows for customization to fit individual circumstances. B. Retiree Status Planning: Reaching retirement age marks a significant milestone for anyone. For civil servants, there are particular guidelines that must be followed to attain retirement status. Determining the correct timeframe and milestones will enable the optimal use of certain benefits like annuities and deferred compensation. C. CSRS vs. FERS Comparison: As a government employee, you fall under either CSRS (Civil Service Retirement System) or its successor program, FERS (Federal Employee Retirement System). Each system has advantages and disadvantages; understanding their differences is crucial for selecting the most suitable option. D. Young Adult Life As you enter adulthood, the world opens up like a freshly blossomed flower, offering myriad possibilities. You might find yourself navigating entry-level jobs while trying to build a solid credit score. With little experience and even less knowledge, managing money becomes an intimidating task. However, this is the time when smart financial choices set you apart from others. Starting with simple steps such as crafting a basic budget, monitoring expenditures, and setting aside cash for unexpected events, lays the groundwork for a secure future. 2. The power of compounding interests So, have you paid off those hefty student loans yet? Well, hang tight because now begins the arduous battle against the burden of repayment. Remember, a thorough approach to tackling debt includes exploring multiple income sources, setting realistic targets, prioritizing expenses wisely, and seeking advice when needed. The beauty lies in exploiting the power of compounding interests, i.e., allowing your money to grow exponentially over time. Plus, who doesn't love having extra cash stashed away for a rainy day? Beginning to save diligently helps avoid potential financial disasters down the line. Leverage low risks With time comes the luxury of witnessing your investments yield rich dividends. Don't wait until you reach midlife to jumpstart your portfolio; instead, leverage low risks early on. Learning about asset allocation, balancing stocks vs. bonds, researching companies, and other complex investment techniques form the basis of successful long-term growth. 3. Mid-Career Professionals This stage brings stability and predictable routines but requires consistent monitoring of finances. Reflect on previous errors and stay committed to ensuring similar pitfalls don't arise in the near future. Analyzing well-thought-out long-term plans and assessing whether they have been met serves as an excellent reality check. It's never too late to pivot or adjust said objectives. Budgetary reviews now include higher net worth and larger monthly savings than before. Savvy savers will focus on boosting retirement accounts through maximized employer matches, IRA contributions, Roth conversion opportunities, and after-tax investments. Umbrella liability insurance coverage can help guard against legal issues triggered by unexpected events. High-interest credit card balances often get transferred to home equity lines, reducing interest charges owed by consolidating obligations. College savings plans also demand careful consideration to secure the best possible educational options for loved ones. With careful deliberation and expert guidance, one can navigate this stage with relative ease and confidence while maintaining momentum toward meeting established fiscal targets. 4. Old-age Retirement represents the culmination of lifelong hard work and dedication. However, it is crucial to ensure adequate preparation has occurred beforehand to avoid any unwanted surprises. At this stage, carefully evaluate the value of accumulated assets and the potential impact of inflation or market volatility on net worth. Importance of Estate Planning and Retirement Decision-Making Now more than ever, having up-to-date estate plans in place becomes paramount, especially if looking to distribute inheritance among heirs in an orderly manner. Carefully contemplate the decision to continue working or transition fully into retirement, including decisions surrounding when to start receiving Social Security benefits to optimize lifetime payouts. Maximizing Retirement Resources: Identifying Potential Shortfalls and Preparing for Healthcare Needs Additionally, take stock of expected post-retirement spending requirements and compare those figures against currently projected financial resources to identify potential shortcomings. Pay attention to Medicare enrollment and appropriate Part D prescription drug coverage choices. Building a Lasting Legacy Lastly, focusing efforts on legacy building through means such as philanthropy or intergenerational wealth transfers will help create lasting impressions beyond mere monetary measures alone. By addressing these critical areas, entering old age provides a solid foundation for living happily and purposefully during this exciting chapter of life. Conclusion As the old saying goes, “Failing to plan is planning to fail.” That couldn’t be more true when it comes to managing our finances through every stage of our lives. From young adulthood to retirement and beyond, having retirement planning services and plans is crucial to achieving both short-term and long-term goals. Remember that it's never too late to start fresh and implement positive changes. Make a habit of regularly reviewing and updating your financial blueprint to adapt to evolving needs and goals. By staying organized and proactive, you'll enjoy greater peace of mind, stronger overall stability, and happier days ahead. Read Also: A Brief Guide To Business Integrated Planning Maximizing Tax Refunds: Tips And Tricks For Canadians Seven Potential Tax Credits Available To Small Businesses In 2023

Apr 27, 2023

Goldman Sachs Recommends 5 Stocks To Buy As It Updates About AI’s Role In The Music Industry

Goldman Sachs's statements about the role of AI in the music industry in the future raise hopes for music shares. The investment company is optimistic about the structural change that is about to happen in the music industry. Last month Goldman Sachs raised its estimates for the revenues regarding the music industry, where they predicted that the industry would be worth $94.9 billion by the end of 2023, and by 2023, it will be worth $153 billion. It described that AI would bring "significant opportunities" for the music industry in the next few years. As per Goldman Sachs' analysts' claim on 28th June, “Generative AI will super-charge music creation capabilities and improve productivity.” Furthermore, regarding AI’s concerns in the music industry with fake syncing, the analysts claimed that many investors are overstating them. The investment company named five stocks that are expected to remain in trend for a long time in the music industry. These are Universal Music Group, Warner Music Group, Live Nation, Believe, and NetEase. Goldman Sachs claims all five stocks as top stocks. The Goldman analysts directed many eyes towards the music industry, as they added, “We believe the music industry is on the cusp of another major structural change given the persistent under-monetisation of music content, outdated streaming royalty payout structures and the deployment of Generative AI.” The analysts at Goldman Sachs reported that the music industry is properly set up to protect its intellectual property rights. This is because there are three large companies on the list that have already established in the industry for a protracted time. The hopes for the music industry are lofty, as the new technology systems coming with AI will reportedly change the perception and the processes of music creation. Read Also: Elon Musk Again Tops The Chart For Becoming The Richest Person In The World, Beating Bernard Arnold $852 Billion Surge Lead By Zuckerberg Among The World’s Richest People Sudden Demise Of Sylvester DaCunha Makes Shocked The Nation

Jul 05, 2023

Navigating Home Financing: A Deep Dive Into Non-Qm Mortgage Loans

In the realm of mortgage financing, Non-QM (Non-Qualified Mortgage) loans have emerged as a flexible and inclusive option for individuals who may not fit the traditional lending criteria. This comprehensive guide aims to shed light on the intricacies of Non-QM mortgage loans, exploring their definition, eligibility criteria, benefits, and considerations for those seeking alternative paths to homeownership. If you're curious about Non-QM loans and want to learn more, click here. Understanding Non-QM Mortgage Loans What Are Non-Qm Loans? Non-QM loans fall outside the guidelines set by government-sponsored entities like Fannie Mae and Freddie Mac. Unlike traditional Qualified Mortgages (QM), Non-QM loans provide a more inclusive approach to lending by considering a broader range of borrower profiles. Eligibility Criteria For Non-Qm Mortgage Loans 1. Credit Flexibility Non-QM loans are designed to accommodate borrowers with unique credit profiles. Individuals with a recent bankruptcy, foreclosure, or fluctuating income may find Non-QM loans more accessible. 2. Debt-To-Income Ratio Variation While conventional mortgages often adhere to strict debt-to-income ratios, non-QM loans allow for greater flexibility. Borrowers with higher debt-to-income ratios may still qualify based on other compensating factors. 3. Alternative Documentation Traditional mortgages often require extensive documentation to verify income and employment. Non-QM loans, however, may accept alternative forms of documentation, making them more suitable for self-employed individuals or those with non-traditional income sources. 4. Unique Property Types Non-QM loans can be more lenient when it comes to financing unique property types. This flexibility is beneficial for borrowers looking to invest in non-traditional homes or properties. Benefits Of Non-Qm Mortgage Loans 1. Accessibility For Non-Traditional Borrowers Non-QM loans provide an alternative for borrowers who don't meet the stringent criteria of conventional mortgages. This inclusivity extends to self-employed individuals, retirees, and those with unique financial circumstances. 2. Flexible Underwriting Criteria The flexibility of non-QM loans allows lenders to consider a broader range of factors beyond the traditional credit score and debt-to-income ratio, providing more opportunities for approval. 3. Unique Property Financing Borrowers interested in financing unique or non-traditional properties may find Non-QM loans more accommodating than traditional mortgages. 4. Credit Repair Opportunities For individuals with recent credit challenges, Non-QM loans can serve as a stepping stone to homeownership while providing an opportunity to rebuild credit over time. Considerations And Drawbacks 1. Higher Interest Rates Non-QM loans typically carry higher interest rates in contrast to conventional mortgages. It's crucial for potential borrowers to thoroughly assess the long-term financial implications. 2. Potential For Larger Down Payments Some Non-QM lenders may require larger down payments, impacting the initial financial commitment for borrowers. 3. Limited Regulatory Protections Non-QM loans are not subject to the same regulatory protections as Qualified Mortgages. Borrowers should carefully review loan terms and conditions. 4. Variable Loan Terms Non-QM loans may come with variable terms and conditions. Borrowers must understand and assess the specific terms offered by lenders. The Non-Qm Mortgage Loan Application Process 1. Pre-Application Consultation Prospective borrowers should engage in a pre-application consultation with a Non-QM lender. During this phase, the lender will assess the borrower's unique financial situation and discuss available loan options. 2. Documentation Submission Borrowers will be required to submit documentation to support their application. This may include alternative income documentation, proof of assets, and other relevant financial information. 3. Underwriting And Approval The lender will conduct a thorough underwriting process, considering the borrower's unique circumstances. Upon approval, the borrower will receive a loan offer with specific terms and conditions. 4. Property Appraisal As with any mortgage, a property appraisal may be required to determine its value and suitability for financing. 5. Closing And Homeownership Upon completing the necessary steps and meeting any remaining conditions, borrowers can proceed to the closing. This involves signing the required paperwork, officially making them homeowners. Conclusion Non-QM mortgage loans offer a valuable alternative for individuals who may not fit within the parameters of traditional lending. While they come with certain considerations and potential drawbacks, the inclusivity and flexibility of Non-QM loans make them a viable option for a diverse range of borrowers. As with any significant financial decision, thorough research, consultation with non-QM lenders, and a clear understanding of the terms are crucial. If you're intrigued by the possibilities of Non-QM mortgage loans and want to explore more, click here for additional information. Read Also: How To Get Personal Loan On Bajaj Markets Speed Up Your Funding: A Quick Guide To Business Loans What You Should Know Before Committing To A Cash Buyer

Dec 04, 2023

What Are BA Stocktwits? Is BA Stocktwits A Good Buy?

Are you planning to buy the BA StockTwits? If yes, you have to understand the current market scenario to increase the chances of your stock returns. You must not make your choices in grey. Instead, work out the plans which can help you achieve your goals in the best possible manner. Plan your market research before you invest in BA StockTwits Develop a trading business that can help you to achieve your objectives. The profit earning potential of this company's stock prices is huge. You will not feel cheated if you invest in BA stock Twits. Here, planning and proper implementation of the planning hold the key. Keep your concepts intact while making your investments in BA StockTwits. Reasons To Purchase The BA StockTwits There are several reasons to purchase the BA Stocktwits to help you achieve your business goals in the correct direction. But, first, work out the plans that can help you achieve your objectives in the best possible manner. IPO allotment Status of BAStockwits you can check to get clarity in the decision-making process of your investments. 1. BA Stock Prices Closes At A Hike Boeing has faced turbulent two years for its latest trading sessions. However, it can help your business grow further in a short time frame. Workout your plans that can work well in your favor. Do not make your choices grey while investing your money in the stocks. Boeing has made some tough decisions to increase its market strength in preparing Aircraft orders. As a result, the shares of the Airplane builders have risen to 3.42% in the past month, and it is growing at a rapid rate. As a result, BA StockTwits are now challenging the market condition to rise above expectations. 2. Its Share Prices Will Increase A Lot In Upcoming Month It is expected that Boeing will display financial strength in the prices in the upcoming months. Till the next earning release, the economic power of this company will increase. You have to work out your plans to achieve your objectives in the correct direction. Its expected returns will be $0.06 per share in the market. In the upcoming years, the financial growth of this company ranges to 100.39% on a year-on-year basis. So it can help your business to grow at a rapid pace. The IPO allotment status check online can make things easier for you. 3. It Displays Strength In The Next Financial Year In the upcoming quarter, the net sales of this company are expected to grow by $17.77 billion. It is up by 16.11% from its upscale working unit. It will grow further in the right direction in the next financial year. The estimated earnings of $1.56 per share with average revenue of $65.33 billion will be considered over the next financial year. It is possible for the share prices to dip from 93.29% to 12.34%. Do not invest your money without considering the changes in the stock prices. 4. Projected Earnings Will Rise The BAStocktwits earnings will rise in the upcoming years. It can help your trading business to grow in the right direction. Do not make your choices in the wrong order while planning to invest in the stock market. The IPO allotment status will improve in the upcoming years of Boeing company. Positive estimated revisions ensure a higher level of business growth. It is why it shows a positive outlook for your business growth in the upcoming years to come. You cannot make your choices depending on the current scenario rather you have to understand the market status of the company as well. 5. Stock Prices Will Change Directly Investors should also maintain the recent changes as an analyst that comprises an optimistic estimate for Boeing. It typically reflects the short-term trends for the business, and it can help you understand the status of stock prices in the years to come. The average annual return for the stock prices has increased to 25% in the upcoming years. You will get better returns from your investments if you want to grow your business in the correct direction. Develop your investment strategies to increase the maximum returns from your investment. 6. Ensures Strong Position In The Stock Market The Boeing stock prices are increasing rapidly, and you will get a fair return from your investment if you invest your money when there is a considerable price hike. You will get a better price if you manage to make your investments at the right time. The Defence Industry is a part of the Aerospace sector. The Aerospace giant has delivered 302 aircraft since the year it commenced its business. During the end of November 2021, 829 gross orders were completed by Boeing. Why Buying The Stock Of Boeing Is Legit? Boeing can reflect higher share prices in the upcoming years, and there are several reasons behind it. So let’s find out the reasons one after the other to get a better insight into it. The orders of Boeing are increasing at 737 max output. It has a plan to boost the production of 31 jets per month. The commercial planes production of this company will increase by 69% in the upcoming year, as stated by its CEO. Boeing has recorded 156 million Starline capsules. In the upcoming NASA’s commercial crew program. It is one of the largest Aviation companies in the world today whose share prices you can trust blindly. In the upcoming year, it is expected that there will be a 31% increase in the stock prices of Boeing as the rate of production increases. The best thing about Boeing is its competitors cannot match with the range of services it offers to its clients. Final Take Away Hence, if you want to increase the returns from your investment, then buying the stocks of BA StockTwits can prove to be a good investment plan. It can increase the chances of your stock turnover over a particular period. Make your investments after making market research. Whenever you plan to increase the chances of your returns from your investment, you must ensure that you have analyzed the company profile in all possible aspects to increase the chances of your returns from your investment. #Disclaimer: The information provided on this blog is for educational and informational purposes only and should not be construed as financial advice. I am not a licensed financial advisor. Any investment decision you make is at your own risk, and you should consult with a qualified financial advisor before making any investment decisions. This site may contain affiliate links, and I may earn a commission at no additional cost to you. More Resources: What Is SHLL? Is SHLL A Good Stock In 2021? Is MAX Stock A Good Buy? Everything You Should Know MNPR Monopar Therapeutics Inc. Stock Forecast And News

Jan 14, 2022