How To Start An Insurance Company? – Steps You Must Take

How to start a life insurance company? – There is no short answer to this question. It is not a small task to start an insurance company. However, having the right focus and the right steps can help you to turn your new business into a victorious one in a short span of time. To learn more, read on through to the end of the article.

The best steps to take on how to create an insurance company would be the ones that are tried and tested by many. Realistically speaking, the risks associated with the insurance sector are so high that a small mistake can cost you a fortune. Hence, you need to take careful steps. Despite that, there are some places you will need to be unique as well. But, to get started, the best option for you would be to stick to the basics.

How To Start An Insurance Company? – Major Steps

One of the first things that you can do to start an insurance company is to find out an idea of what will make your company different from the top companies in the market. Once you have chosen the insurance industry, you will need to do a quick search of the existing companies.

According to Business News Daily,

“Learn what current brand leaders are doing and figure out how you can do it better. If you think your business can deliver something other companies don’t (or deliver the same thing, only faster and cheaper), you’ve got a solid idea and are ready to create a business plan.”

To start with

“how to start my own insurance company,”

you will need to ensure that your business does not face any legal problems or any other external problems. Hence, you need to make sure that your business is safeguarded as long as external issues are concerned. For that to happen, you need to follow some basic rules.

The following are the major steps you must take to start your own insurance company in 2023:

1. Planning To The Core

According to The Hartford,

“When you create a business plan, you’re describing every aspect of your business in a formal document. This lets other people understand what you do, what your objectives are and what strategies you have in place to achieve your goals.”

Furthermore, this document will also be your proof that you are dedicated to the business. This is beneficial for staying clear in front of insurance companies, shareholders, and staff members. However, with time, you will also need to update your business plan with necessary changes as per the demand of the market.

Read More: The Types Of Business Insurance Needed For Every Business

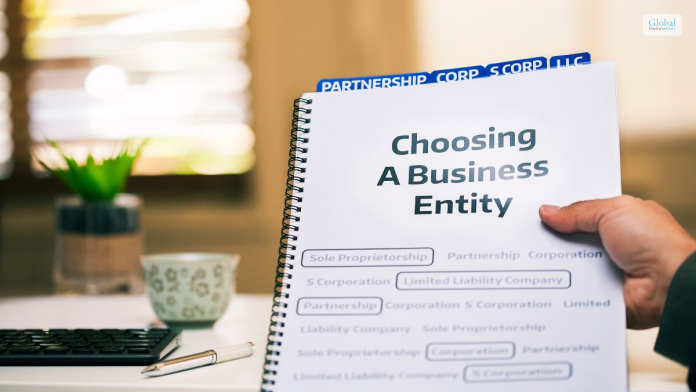

2. Decide What Will Be Your Business Structure

According to SBA.gov,

“The legal structure you choose for your business will impact your business registration requirements, how much you pay in taxes, and your personal liability.”

Here are the major types of business structures:

- Sole Proprietorship

- Corporation

- Limited Liability Company (LLC)

- Partnership

- S Corporation

This depends on your personal responsibility and the setup of your business, as well as the setup of your business. Hence, you will need to choose the business structure that is right in your case. The structure depends upon your personal liability level.

3. Register Your Organization’s Title

Registering is important. As per the recommendations of TheHartford.com,

“Your business needs to be official. Aside from giving your startup more credibility with potential customers and clients, registering can also help protect your business’ name.”

If your business is structured as a sole proprietor, your personal name is automatically the legal name of the company. However, you can give another name in the “doing business as” section. You will need to select and register a suitable name for your business.

4. Get Your TIN (Tax Identification Number)

As per IRS regulations, every corporation and partnership needs to use FEIN (Federal Employer Identification Number) while it is filing taxes. This number is also important in the case of opening a bank account or a credit account for your business.

However, if your business is structured as a sole proprietor, you will need to use your social security number (SSN). You will get the number after you register your business with the local government and IRS.

5. Ensure That Your Business Is State Registered

Once you have received your Tax ID, you will have to connect with the State Insurance Commissioner’s desk. Businesses typically register as “resident business entities” when it comes to purposes related to state and local taxes.

Once you register, your state will charge a registration fee from you. They will also give you a checklist, where they will ask you to ensure that you are aware of the state requirements and comply with them.

6. Get The Necessary Local Authorizations And Licenses

Getting authorized at the local level and getting all the necessary licenses and permits is crucial to operating your business. Although you are a licensed insurance agent now, you will still need a general business permit at the local level or even a license if you want legal safeguards.

However, according to Insureon.com,

“The licensing, insurance, and bonding requirements for insurance agents vary by state. Having the right insurance and bonding can help keep you financially protected, and may be required for some jobs within the insurance industry.”

7. Get Insurance To Save Your Company’s Capital

Depending on the structure and assets of your business, you will need to purchase insurance. There are a variety of business insurance you can check out to find which one is the right need for the moment. You can also consult with your lawyer, as well as your insurance guide, to find out which insurance is perfect for you now.

Read More: Maximizing Home Insurance Coverage For Your At-Home Business With Riders

Final Thoughts

Hope you have found your answer on how to start an insurance company. Before starting your business and competing in the market, you will need to make sure that your business has all the legal safeguards. This is the most important aspect, as it will help your business in the long run. Share your thoughts about the business safeguards and other ideas in the comments section below.

Read Also:

Tags:

Recent

Time Matters: The Role of Early Hazard Detection in Industrial Safety

Jan 20, 2026

Hidden Ignition Risks in Industrial Environments

Jan 17, 2026

Critical Thinking Exercises in the Digital Age and Emotional Intelligence Integration

Jan 14, 2026

Why Strategic Partnerships Matter More Than Ever

Jan 13, 2026

Related Articles

Business Deductions And Tax Planning: Two Critical Steps To Save Money

As the owner of a company, doing tax planning is an essential part of sound financial management. Locating and making the most of all available company deductions is one of the most important aspects of tax preparation. Your overall tax liability will go down as a result of the reduction of your taxable income brought about by deductions. Continue reading to find out about some potential tax write-offs and deductions for your business that you may be overlooking, as well as some suggestions on how you might utilize these opportunities to reinvest in your company. Understanding Businesses Deductions And Tax Planning Steps For businesses are costs that are directly relevant to the running of a firm. When calculating your taxable income, these expenditures may be subtracted from the money generated by your firm. Expenses that are regular and essential, as well as those that are considered capital, may be deducted from a business's income. 1. Locating And Making A Claim For Tax Deductions It is essential to maintain precise records of your company's costs to properly identify and account for tax deductions. The Internal Revenue Service mandates that all expenditures must have supporting paperwork and receipts. Knowing which deductions you are eligible to claim is also very important since certain costs could not be deductible at all. 2. Utilize The Available Tax Breaks The qualifying business income (QBI) deduction allows owners of pass-through businesses to take a deduction equal to up to 20% of their share of the firm's income. However, this deduction is subject to several regulations and limits and does not come without restrictions. Figuring out who is eligible to claim the QBI deduction and then determining the amount of the deduction itself is not a straightforward operation. However, the deduction may offer a large tax break for owners of small businesses. If you believe you could qualify for this, you should discuss it with your accountant. 3. Investigate Different Ways To Cut Down On AGI Your adjusted gross income, often known as your AGI, is a primary factor in determining the taxes that you must pay. For instance, if your adjusted gross income (AGI) is less than $200K, or if you are married, your AGI is less than $250K, then you will not have to pay the extra 0.9 percent in Medical taxes. You may reduce your AGI by the below methods or by lowering your salary: For example, by registering a company in the US we can obtain some benefits. Making contributions to a retirement plan that postpones paying taxes until later. Using the itemized deductions method if your total deductions are more than the standard deduction. Making contributions to a health-related savings account If you have any reason to believe that you will wish to itemize your deductions, you might think about keeping track of them on a spreadsheet throughout the year. 4. Learn To Leverage Tax Credits Tax credits are an additional method that businesses may use to reduce the amount of tax liability they are responsible for paying. Tax credits, in contrast to tax breaks, which lower the level of cash that is subject to taxation for a person or corporation, reduce the percentage of tax that is actually owed by the taxpayer. It is in the best interest of businesses to benefit from tax benefits. Consider the following few options: Credit for work opportunities offered: Access credit for the disabled: Tax breaks for health insurance premiums paid by employers with less than 25 employees 5. Delay Or Accelerate The Receipt Of Income When it comes to their financial records and tax filings, many small firms rely on cash. When using this cash method a business records revenue and costs at the time that the corresponding cash transaction takes place. So, it means records are taken when the cash changes hands. This opens up some intriguing possibilities for tax planning tactics. You could wish to delay receiving income until the next year if you believe that you will be in a reduced tax band the following year. 6. Purchase Assets At The End Of The Year In certain tax years, it can be helpful to estimate the amount of taxes your company will owe, and then to acquire assets, both new and already used, to lower those estimated taxes. 7. Pay Student Loans Of Workers Employers are now permitted to provide financial assistance to their workers in the form of student debt repayment via a clause that was included in the CARES Act 2020. This Act contains a condition that permits companies to claim a tax exemption for repaying employee student loans and eliminates it from employee income, which means that workers do not have to pay required taxes on the money. 8. Work With Independent Contractors If you engage independent contractors or freelancers for any reason linked to your company (for example, taking images of things for your online shop), you can deduct the cost of their services from your taxable income. Before independent contractors begin working for you, you should always make it a point to gather their 1099 forms and ensure that you file them correctly. 9. Reconsider The Type Of Business Entity Your choice of business entity has a big influence on the amount of Taxes You Will Owe. People who are self-employed and must pay self-employment taxes include those who operate their businesses as sole proprietorships, limited partnerships, or certain limited liability companies. If you anticipate that your company will owe a significant amount of money in taxes, one solution to this problem is to restructure your company so that it is treated as a different kind of legal organization. Last Words: Why Is It Important For Businesses To Plan Their Taxes? You are required to pay taxes as the owner of a company, but the amount that you owe should never come as a complete shock to you. It is crucial to understand how company taxes operate and to make estimations of the amount you need to pay each quarter or year to guarantee that you have sufficient funds. Tax planning is something that can help you generate correct tax predictions, make all tax forms and reports on time, and avoid the possible ramifications of not doing so. Planning your taxes properly may help you achieve all of these things. Read Also: How To Start A Logistics Company? An Expert Guide Biggest Stock Market Crashes In The World History 10 Best Investment Apps For 2021

Feb 20, 2023

The Best Risk Mitigation Techniques For Your Business

Risks in business are inevitable, and with new projects and processes, the level of risks in business increases. This is because there are inherent risks that are associated with the processes of a project. However, there are some strategies that you can follow for risk mitigation. These will help you deal with risks in business that arise with the coming of new projects. In this article, you will learn some general details about risk mitigation. You will also learn how to plan for risk mitigation in business. Then, we will share with you some of the major risk mitigation strategies to follow. Hence, to learn more about risk mitigation in business read on through to the end of the article. What Does Risk Mitigation Mean In Business? According to Indeed.com, “Risk mitigation refers to the process of planning and developing methods and options to reduce threats—or risks—to project objectives. A project team might implement risk mitigation strategies to identify, monitor and evaluate risks and consequences inherent to completing a specific project, such as new product creation.” Major risk mitigation strategies include the actions that managers put in place to deal with major issues and also the effect of these issues in regard to the project. These strategies are brought in by risk management. Risk management is one of the most essential tools required to run a business, especially when the business faces a downturn. When an internal risk or an external risk, an unexpected surprise can easily destroy the business processes. Hence, this is whether risk management strategies help. With these strategies, you will be able to know what steps to take if you want to mitigate the risks in business. How To Plan For Risk Mitigation? With the help of a risk mitigation program, you will have your procedures in hand. However, before you mitigate the risks, you will be able to identify those risks. You will have to learn what type of risks you are dealing with, for example, organizational risks. Furthermore, you will have to stress the importance of identifying the different vulnerabilities that can affect your business. According to TechTarget.com, “A priority list should be created to rank each risk according to the likelihood of occurrence and severity of the impact on the enterprise. A high-probability event, for example, that has little or no impact on the enterprise, such as an employee calling in sick for one day, will be treated differently than a low-probability, high-impact event like an earthquake.” Identification is necessary if you want to address a particular risk and its threats and vulnerabilities. Next up, you will need to validate and analyze it to find the likelihood of the risk’s occurrence in business. You can also involve the employees and customers and learn from them their own feedback on the problems they are facing. This way, you can find the hidden risks that are threatening your business. In the business realm, these vulnerabilities can often appear in financial areas, notably during taxing periods. For these complexities, hiring a professionals can be invaluable. If you're considering hiring a sales tax accountant, you're opting for a preventive risk mitigation strategy. This expert can help manage your tax affairs effectively, ensuring complete compliance while identifying possible cost-saving areas. Hence, hiring a CPA for sales tax can indeed act as a significant risk buffer for your business. Read More: The Types Of Business Insurance Needed For Every Business What Are The Best Risk Mitigation Ways In Business? According to Investopedia, “Risk management has always been an important tool in running any business, particularly when a market experiences a downturn. In any economic environment, an unexpected surprise can destroy your business in one fell swoop if you didn’t have the right risk management strategies in place to prevent, or at least mitigate, the damage from that risk.” Hence, it is important for the business to have a risk management process in place. However, to enable risk management to work, risk mitigation is important. Here are the steps that you can take to ensure risk mitigation: 1. Throw A Challenge Towards The Risk If you see a future risk, start challenging it by allowing it to progress. However, make sure that the dangers are negligible and are easily manageable. This way, you will be able to learn the risk and prevent it accordingly. 2. Start Prioritizing The hazards that the risk can bring pose negative effects for your business and your team. Once you prioritize the risks, you can minimize the potential impact. You are just dealing with the risk as per its order of importance. 3. Exercise The Risk Since you have already identified the major hazards associated with the risk, it is time to exercise those risks. To do that, start running experiments, drills, and other exercises to model threats. 4. Risk Isolation You cannot stop other activities in the business which are necessary for its operation. By isolating the risk from other aspects of operations, you can minimize the risk’s negative impact. 5. Risk Buffering Once you add extra resources to the situation, you can minimize the potentiality of the risk. The resources can be time, money, or even personnel. This is called buffering of the risk, as it reduces the negative impact of the risk. 6. Risk Quantification Risks come with both cost and reward. You will need to quantify, compare, and analyze both sides in regard to the risks. This will help you to determine whether the positives are enough to justify the risk’s impact. 7. Monitoring The Risk Since risks are not static, you must use a two-way communication solution to monitor the risk conditions that affect your business. 8. Contingency Planning No matter how much you plan and stick to the plan, it can still lead to failure. Hence, always keep a backup plan in place, even when you think you have handled the risks. 9. Learning From Best Practices Since there are many businesses and industries present, the occurrence of a novel risk for your business is less probable. Someone might have already faced the risks that you are facing now. Hence, you should look for best practices in the industry to mitigate risks. Read More: How To Start An Insurance Company? – Steps You Must Take Wrapping Up Hope this article was helpful for you in getting a better idea of the best risk mitigation strategies for businesses. To ensure proper risk mitigation, the business needs to implement a top-end risk management policy in place. This will act as insurance in itself and can become an important step to ensure the success of the business. Consider following the aforementioned risk mitigation strategies in your business once you have identified the inherent risks for your business. Do you have any more recommendations in mind regarding the best ways for risk mitigation in business? Share your views with us in the comments section below. Read Also: How Do Entrepreneurs Make Money? – The Secrets You Should Know Project Management: What Is It? – Major Types, Examples, And More 10 Must-Have Entrepreneurial Characteristics

Sep 02, 2023

What Is A Sales And Purchase Agreement For Business? – Let’s Find Out

A sales and purchase agreement for business is a binding legal contract that consists of conditions both the buyer and seller of a business or property agree upon. In any sale process, it is one of the main legal documents. It basically sets out the elements that are agreed upon in a business deal. It also consists of the number of protections of both parties as well as the legal framework for the completion of the sale. In this article, you will learn about the sales and purchase agreement (SPA) and some of its general details. Apart from that, you will also learn about how the sales and purchase agreement works for businesses. In addition to that, we will also discuss the major constituents of a sales and purchase agreement that all the parties in a sales process need to consider. Hence, to learn more about the SPA, read on through to the end of the article. What Is A Sales And Purchase Agreement For Business? According to Investopedia, “A sales and purchase agreement (SPA) is a binding legal contract between two parties that obligates a transaction to occur between a buyer and seller. SPAs are typically used for real estate transactions, but they are found in other areas of business. The agreement finalizes the terms and conditions of the sale, and it is the culmination of negotiations between the buyer and the seller.” In the case of the trading of a product or a service between two parties, there is a need for a legally binding contract that outlines the details of the agreement. This is called the sales and purchase agreement, and both parties (the buyer and the seller) need to sign the agreement contract. Furthermore, neither of the parties will be able to disobey the contract at any cost. Otherwise, it might lead to legal action. However, it is not an obligation for either of the parties to stay on the deal in question if one of them disagrees with the deal. Once both parties sign the agreement, they will need to follow the terms of the translation. Some of the essential things that are present in this agreement include - terms and conditions, purchase price, deposits made, limitations, closing date, contingencies, etc. How Does A Sales And Purchase Agreement (SPA) Work? According to Wall Street Mojo, “The sales and purchase agreement of business signifies the culmination of negotiations between the buyer and seller and restricts them from ditching each other. The two parties mutually agree upon it before signing it and making it legally binding. It does, however, require both parties to read the contract carefully and seek legal counsel before deciding whether or not to sign it or request a revision.” The sales and purchase agreement occurs mostly in real estate deals, stock purchases, mergers & acquisitions, advertising contracts, etc. On the other hand, the constituents of the SPA include its purchase price, settlement date, deposits paid during the negotiation process, limitations, contingencies, and many more. Apart from that, in such an agreement, both parties in the sales process need to agree to the contract after thoroughly reading it. For this, a business needs to obtain legal advice after signing it and requesting a change. The agreement, basically, provides protection to the interests of both parties. Apart from that, it also restricts them from working against each other or moving away after signing the deal. This factor helps in minimizing potential conflicts and helps to forecast demand and costs of business. What Are The Constituents Of An SPA? According to the Corporate Finance Institute, “Essentially, the sale and purchase agreement spells out all the details of the transaction so that both parties share the same understanding. Among the terms typically included in the agreement are the purchase price, the closing date, the amount of earnest money that the buyer must submit as a deposit, and the list of items that are and are not included in the sale.” 1. Asset Identification Here, you will get information about the specific asset that is subject to sale. In the case of a real property, the location and other details of the asset are jotted down. 2. Purchase Price and Conditions It consists of the exchange price of the transaction in question. Apart from that, the agreement also contains details about how much is already paid and how much is left. It also contains information about the way that the deposit is to be made. It also outlines how the buyer will pay the remaining balance of the transaction. 3. Due Diligence There is a section in the agreement that asks the buyer to acknowledge their due diligence in the transaction. It also contains the due diligence period, which might contain additional payments. 4. Covenants/Conditions Prior to Close The agreement also contains the next steps of the transaction process. The conditions here must be in order to make the sales process legally binding. If the parties fail to follow or if there is any inaction, then it amounts to a breach of contract. 5. Damages/Remedies In some cases, the parties need an explanation regarding what to do in case of damage prior to the sale or during the transit of a product. Hence, this section consists of various levels of damages that can occur to the asset. As per each damage, there is a remedy present. Final Thoughts Hope this article was helpful for you in getting to know about the sales and purchase agreement (SPA). A sales and purchase agreement for a business is a legally binding contract that consists of the conditions set by the buyer and seller, which both agree upon. SPAs are mostly common in real estate dealings, in which the item of transaction is large and includes a big amount. The SPA basically consists of various important information about the sales deal that includes the prices of the asset, the sales price, as well as the payment terms of the sales. It also consists of information about the due diligence period and the agreed-upon conditions. Do you have any more info to add? Share your ideas with us in the comments section below. Go For The Best And Latest Business Related Articles By Clicking Below!! What Are Articles Of Incorporation? – Importance, Working, And More Inventory Turnover Ratio: Definition, Formula, Working, And More What Are Articles Of Organization? – Let’s Find Out

Nov 10, 2023

What Is Risk Management? – Find Out How To Manage Risks in Business

What is risk management? - Simply put, it is the process by which businesses identify, assess, and control the various risks that threaten the growth, capital, and earnings of the organization. The risks for the organization can come from a variety of sources, both internal and external. These can be financial problems, legal problems, management errors, accidents, tech issues, economic problems, disasters, and many more. In this article, you will learn about risk management in general and will get a good understanding of its essentiality in business. Furthermore, you will also learn the importance of risk management and how it can shape a business. Finally, we will share with you some of the best practices of risk management, with the help of which you can ensure a proper risk management system in place. What Is Risk Management? According to IBM.com, “Risk management is the process of identifying, assessing and controlling financial, legal, strategic and security risks to an organization’s capital and earnings. These threats, or risks, could stem from a wide variety of sources, including financial uncertainty, legal liabilities, strategic management errors, accidents, and natural disasters.” Risk management is important for situations when an unforeseen event (internal or external) pushes the organization into a threatening situation. It can also be an economic situation where an unexpected surprise in the market can heavily impact your business. Hence, having a risk management framework for your business is really essential. The risk management framework will help you mitigate the risks in a better manner. Even if the risk affects your business, the risk management system will enable you to deal with that risk better. External risks are out of your control, and you cannot do a lot to receive the impact of the risks. However, you can do many things to stop and mitigate the internal risks for your business. You will need to anticipate and prepare for the risks, despite the size of the business or the level of impact of the risk in the business. Read More: Intrapreneurship – Definition, Importance, Duties, And Responsibilities Why Is Risk Management Important? According to Investopedia, “Risk management has always been an important tool in running any business, particularly when a market experiences a downturn. In any economic environment, an unexpected surprise can destroy your business in one fell swoop if you don’t have the right risk management strategies in place to prevent, or at least mitigate, the damage from that risk.” There are many risks that have enough potential to destroy the business and its operations. Hence, as a manager or CEO of the organization, you will need to identify what are the risks that pose threats to the operations of your business. It does not matter whether the business is a startup or an established one. Risks can impact the business a lot. Even if a risk starts impacting a business, a business that is well-prepared can minimize the impact of the risk on the business’s earnings. With the impact of the risk, the business can also lose a lot of time, productivity, and even customers. Hence, the identification of the risks of the business should be a key part of the business’s strategy and planning. You can identify risks in a number of ways once you implement a proper risk management system in the organization. What strategies you will employ to identify those risks should rely on the specific business activities of the company. What Are The Best Ways To Manage Risks? Having a proper risk management system in place is one of the major necessities. However, people still have their own biases. According to Harvard Business Review, “Multiple studies have found that people overestimate their ability to influence events that, in fact, are heavily determined by chance. We tend to be overconfident about the accuracy of our forecasts and risk assessments and far too narrow in our assessment of the range of outcomes that may occur.” Here are the steps that you will need to take to ensure that you have a proper risk management system in place: 1. Risk Prioritization If you have multiple risks, prioritizing the top ones will help you to deal with them as per their impact and possibility of impact. 2. Having A Business Insurance Once you purchase insurance, you are transferring the risks of the company to insurance companies. Furthermore, you are not paying a lot of costs. 3. Becoming An LLC If you do not want to be personally liable for the debts of the company, change your company’s structure to a Limited Liability Company (LLC) or a Corporation. 4. Quality Assurance Quality assurance of products and services will help your business in increasing its reputation. Ensure to test them before customers purchase them. This will allow you to make all the necessary adjustments beforehand. Also, ensure that your testing methods are foolproof. 5. Get Away From High-Risk Customers Implement a policy in your organization that the company will not entertain customers with poor credit. Even if the company deals with them, the customer must pay ahead of time. This shall lower the complications for the business in the long run. 6. Growth Control Training your employees is of the highest importance here. To sell your products and services, if you set big goals for your employees, they shall be tempted to take uncalculated risks. This can make things go wrong and damage your company’s reputation. 7. Risk Management Team Apart from paying an outside company to manage the risks in your business, consider having a risk management team of your own. To do this, you can appoint some of your current and experienced employees to work in risk management. Read More: Entrepreneur : Who Coined The Term ‘Entrepreneur’? Final Thought What is risk management? - Risk management basically creates insurance for the company from within and is really important to ensure the success of the organization. If you want to implement a system within your company, consider following the aforementioned steps. To shape a better strategy for your business, you will need to get a better idea of the business and the industry by diving deeper. Do you have any more recommendations regarding better risk management strategies? In that case, consider sharing your thoughts and views with us in the comments section below. Read Also: What Is Social Entrepreneurship? – Steps To Become A Successful Social Entrepreneur Business Entrepreneurship – What Should You Know Before You Start A Business? What Is a Franchise, And How Does It Work? – Examples, Benefits & More

Sep 02, 2023