How To Start An Insurance Company? – Steps You Must Take

How to start a life insurance company? – There is no short answer to this question. It is not a small task to start an insurance company. However, having the right focus and the right steps can help you to turn your new business into a victorious one in a short span of time. To learn more, read on through to the end of the article.

The best steps to take on how to create an insurance company would be the ones that are tried and tested by many. Realistically speaking, the risks associated with the insurance sector are so high that a small mistake can cost you a fortune. Hence, you need to take careful steps. Despite that, there are some places you will need to be unique as well. But, to get started, the best option for you would be to stick to the basics.

How To Start An Insurance Company? – Major Steps

One of the first things that you can do to start an insurance company is to find out an idea of what will make your company different from the top companies in the market. Once you have chosen the insurance industry, you will need to do a quick search of the existing companies.

According to Business News Daily,

“Learn what current brand leaders are doing and figure out how you can do it better. If you think your business can deliver something other companies don’t (or deliver the same thing, only faster and cheaper), you’ve got a solid idea and are ready to create a business plan.”

To start with

“how to start my own insurance company,”

you will need to ensure that your business does not face any legal problems or any other external problems. Hence, you need to make sure that your business is safeguarded as long as external issues are concerned. For that to happen, you need to follow some basic rules.

The following are the major steps you must take to start your own insurance company in 2023:

1. Planning To The Core

According to The Hartford,

“When you create a business plan, you’re describing every aspect of your business in a formal document. This lets other people understand what you do, what your objectives are and what strategies you have in place to achieve your goals.”

Furthermore, this document will also be your proof that you are dedicated to the business. This is beneficial for staying clear in front of insurance companies, shareholders, and staff members. However, with time, you will also need to update your business plan with necessary changes as per the demand of the market.

Read More: The Types Of Business Insurance Needed For Every Business

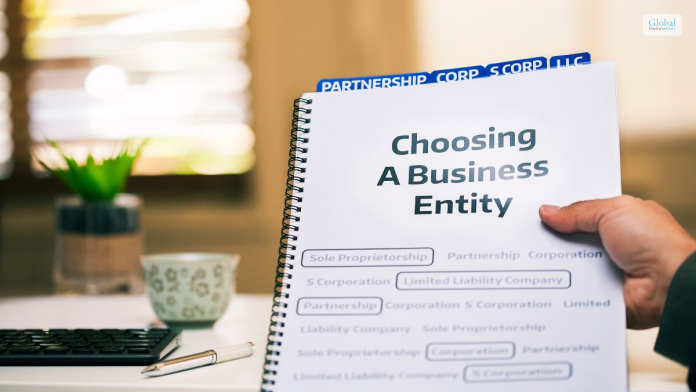

2. Decide What Will Be Your Business Structure

According to SBA.gov,

“The legal structure you choose for your business will impact your business registration requirements, how much you pay in taxes, and your personal liability.”

Here are the major types of business structures:

- Sole Proprietorship

- Corporation

- Limited Liability Company (LLC)

- Partnership

- S Corporation

This depends on your personal responsibility and the setup of your business, as well as the setup of your business. Hence, you will need to choose the business structure that is right in your case. The structure depends upon your personal liability level.

3. Register Your Organization’s Title

Registering is important. As per the recommendations of TheHartford.com,

“Your business needs to be official. Aside from giving your startup more credibility with potential customers and clients, registering can also help protect your business’ name.”

If your business is structured as a sole proprietor, your personal name is automatically the legal name of the company. However, you can give another name in the “doing business as” section. You will need to select and register a suitable name for your business.

4. Get Your TIN (Tax Identification Number)

As per IRS regulations, every corporation and partnership needs to use FEIN (Federal Employer Identification Number) while it is filing taxes. This number is also important in the case of opening a bank account or a credit account for your business.

However, if your business is structured as a sole proprietor, you will need to use your social security number (SSN). You will get the number after you register your business with the local government and IRS.

5. Ensure That Your Business Is State Registered

Once you have received your Tax ID, you will have to connect with the State Insurance Commissioner’s desk. Businesses typically register as “resident business entities” when it comes to purposes related to state and local taxes.

Once you register, your state will charge a registration fee from you. They will also give you a checklist, where they will ask you to ensure that you are aware of the state requirements and comply with them.

6. Get The Necessary Local Authorizations And Licenses

Getting authorized at the local level and getting all the necessary licenses and permits is crucial to operating your business. Although you are a licensed insurance agent now, you will still need a general business permit at the local level or even a license if you want legal safeguards.

However, according to Insureon.com,

“The licensing, insurance, and bonding requirements for insurance agents vary by state. Having the right insurance and bonding can help keep you financially protected, and may be required for some jobs within the insurance industry.”

7. Get Insurance To Save Your Company’s Capital

Depending on the structure and assets of your business, you will need to purchase insurance. There are a variety of business insurance you can check out to find which one is the right need for the moment. You can also consult with your lawyer, as well as your insurance guide, to find out which insurance is perfect for you now.

Read More: Maximizing Home Insurance Coverage For Your At-Home Business With Riders

Final Thoughts

Hope you have found your answer on how to start an insurance company. Before starting your business and competing in the market, you will need to make sure that your business has all the legal safeguards. This is the most important aspect, as it will help your business in the long run. Share your thoughts about the business safeguards and other ideas in the comments section below.

Read Also:

Tags:

Recent

Due Diligence Decoded: Why Careful Evaluation Still Wins in Business

Jul 11, 2026

How Hydraulic System Design Impacts Equipment Performance

Jul 01, 2026

Startup Bootstrapped Fundraising Strategy: A Guide for SaaS and Tech Startups

Jun 21, 2026

Where Distributors Lose Profit Without Realizing It

Jun 20, 2026

Related Articles

The Best Risk Mitigation Techniques For Your Business

Risks in business are inevitable, and with new projects and processes, the level of risks in business increases. This is because there are inherent risks that are associated with the processes of a project. However, there are some strategies that you can follow for risk mitigation. These will help you deal with risks in business that arise with the coming of new projects. In this article, you will learn some general details about risk mitigation. You will also learn how to plan for risk mitigation in business. Then, we will share with you some of the major risk mitigation strategies to follow. Hence, to learn more about risk mitigation in business read on through to the end of the article. What Does Risk Mitigation Mean In Business? According to Indeed.com, “Risk mitigation refers to the process of planning and developing methods and options to reduce threats—or risks—to project objectives. A project team might implement risk mitigation strategies to identify, monitor and evaluate risks and consequences inherent to completing a specific project, such as new product creation.” Major risk mitigation strategies include the actions that managers put in place to deal with major issues and also the effect of these issues in regard to the project. These strategies are brought in by risk management. Risk management is one of the most essential tools required to run a business, especially when the business faces a downturn. When an internal risk or an external risk, an unexpected surprise can easily destroy the business processes. Hence, this is whether risk management strategies help. With these strategies, you will be able to know what steps to take if you want to mitigate the risks in business. How To Plan For Risk Mitigation? With the help of a risk mitigation program, you will have your procedures in hand. However, before you mitigate the risks, you will be able to identify those risks. You will have to learn what type of risks you are dealing with, for example, organizational risks. Furthermore, you will have to stress the importance of identifying the different vulnerabilities that can affect your business. According to TechTarget.com, “A priority list should be created to rank each risk according to the likelihood of occurrence and severity of the impact on the enterprise. A high-probability event, for example, that has little or no impact on the enterprise, such as an employee calling in sick for one day, will be treated differently than a low-probability, high-impact event like an earthquake.” Identification is necessary if you want to address a particular risk and its threats and vulnerabilities. Next up, you will need to validate and analyze it to find the likelihood of the risk’s occurrence in business. You can also involve the employees and customers and learn from them their own feedback on the problems they are facing. This way, you can find the hidden risks that are threatening your business. In the business realm, these vulnerabilities can often appear in financial areas, notably during taxing periods. For these complexities, hiring a professionals can be invaluable. If you're considering hiring a sales tax accountant, you're opting for a preventive risk mitigation strategy. This expert can help manage your tax affairs effectively, ensuring complete compliance while identifying possible cost-saving areas. Hence, hiring a CPA for sales tax can indeed act as a significant risk buffer for your business. Read More: The Types Of Business Insurance Needed For Every Business What Are The Best Risk Mitigation Ways In Business? According to Investopedia, “Risk management has always been an important tool in running any business, particularly when a market experiences a downturn. In any economic environment, an unexpected surprise can destroy your business in one fell swoop if you didn’t have the right risk management strategies in place to prevent, or at least mitigate, the damage from that risk.” Hence, it is important for the business to have a risk management process in place. However, to enable risk management to work, risk mitigation is important. Here are the steps that you can take to ensure risk mitigation: 1. Throw A Challenge Towards The Risk If you see a future risk, start challenging it by allowing it to progress. However, make sure that the dangers are negligible and are easily manageable. This way, you will be able to learn the risk and prevent it accordingly. 2. Start Prioritizing The hazards that the risk can bring pose negative effects for your business and your team. Once you prioritize the risks, you can minimize the potential impact. You are just dealing with the risk as per its order of importance. 3. Exercise The Risk Since you have already identified the major hazards associated with the risk, it is time to exercise those risks. To do that, start running experiments, drills, and other exercises to model threats. 4. Risk Isolation You cannot stop other activities in the business which are necessary for its operation. By isolating the risk from other aspects of operations, you can minimize the risk’s negative impact. 5. Risk Buffering Once you add extra resources to the situation, you can minimize the potentiality of the risk. The resources can be time, money, or even personnel. This is called buffering of the risk, as it reduces the negative impact of the risk. 6. Risk Quantification Risks come with both cost and reward. You will need to quantify, compare, and analyze both sides in regard to the risks. This will help you to determine whether the positives are enough to justify the risk’s impact. 7. Monitoring The Risk Since risks are not static, you must use a two-way communication solution to monitor the risk conditions that affect your business. 8. Contingency Planning No matter how much you plan and stick to the plan, it can still lead to failure. Hence, always keep a backup plan in place, even when you think you have handled the risks. 9. Learning From Best Practices Since there are many businesses and industries present, the occurrence of a novel risk for your business is less probable. Someone might have already faced the risks that you are facing now. Hence, you should look for best practices in the industry to mitigate risks. Read More: How To Start An Insurance Company? – Steps You Must Take Wrapping Up Hope this article was helpful for you in getting a better idea of the best risk mitigation strategies for businesses. To ensure proper risk mitigation, the business needs to implement a top-end risk management policy in place. This will act as insurance in itself and can become an important step to ensure the success of the business. Consider following the aforementioned risk mitigation strategies in your business once you have identified the inherent risks for your business. Do you have any more recommendations in mind regarding the best ways for risk mitigation in business? Share your views with us in the comments section below. Read Also: How Do Entrepreneurs Make Money? – The Secrets You Should Know Project Management: What Is It? – Major Types, Examples, And More 10 Must-Have Entrepreneurial Characteristics

Sep 02, 2023

Why Business Continuity Planning Is Essential For Your Company?

When crises happen in business, it is quite common to panic and make wrong decisions by remaining unprepared. Crises can happen anytime, and you must not start every day with the worst that can happen. However, you must stay prepared for anything to happen. You can do this with the help of a useful business continuity planning structure in place. This is because, if you do not stay prepared for the crises, it can cost your company a lot. In this article, you will learn some general details about business continuity planning. Apart from that, you will learn the importance of having such a planning structure in place. Furthermore, we will also discuss some of the major benefits of business continuity planning, which you must be aware of. Finally, we will share with you the steps you can follow to implement business continuity planning. What Is Business Continuity Planning? Business continuity planning is essential for a company as it helps in creating a prevention and recovery from the various risks and threats that can potentially affect the company. Having the plan will ensure that the personnel and assets of the company are protected. Protecting them will enable the company to start functioning by recovering quickly after a disaster situation. Business continuity planning is also essential to recover from situations like cyber-attacks where the company’s data gets compromised. Read More: What Is Risk Management? – Find Out How To Manage Risks in Business Why Is Business Continuity Planning Important? According to TechTarget.com, “The plan should enable the organization to keep running at least at a minimal level during a crisis. Business continuity helps the organization maintain resiliency in responding quickly to an interruption. Strong business continuity saves money, time and company reputation. An extended outage risks financial, personal and reputational loss.” With the help of the business continuity plan, you are making the company look after itself. You are analyzing the potential areas for risks and gathering important information from those areas. You have to have full information about those areas which are helpful for disaster situations. Furthermore, having a business continuity plan is also important to comply with legal processes. What Are The Benefits Of Business Continuity Planning? According to Investopedia, “Business continuity planning is typically meant to help a company continue operating in the event of major disasters such as fires. BCPs are different from a disaster recovery plan, which focuses on the recovery of a company's IT system after a crisis.” Basically, such a business continuity plan will help you to take stapes, including creating backups of projects, client information, and more. If something must happen to the company’s office, the satellite offices of the company will have access to all the essential information of the company. However, a business continuity plan does not work if a large population in the company is affected. It can happen at times of an outbreak of a disease. Despite that, having a business continuity plan in place will help you to improve the risk management processes of the company. Business Continuity Planning - Steps To Follow To make a great business continuity plan, it is important to have a management that oversees the plan. According to Hubspot.com, “This type of management determines the potential threats to a company and how each of these threats might impact business functions. Based on these findings, business continuity management is able to tweak the company's continuity plan to address any new potential hazards.” There are some steps you must follow to develop useful business continuity planning for your organization. Here are they: Step 1: Select your Business Continuity Team. Here, you must assemble a management team. Make sure the team is well-organized and detail-oriented. Make sure there is at least an executive manager, a program coordinator, and an information officer. Step 2: Define the objectives of the business continuity plan. To do that, you will need to know about what your end goal is. Furthermore, you must also have good information on the resources and budget based on your current projects. Step 3: Find the key players of your department and interview them. Make sure to talk with the executives as they have a bird’s eye view of the organization. Furthermore, make sure to interview the key team members of each department. This will help you to get an analysis that is useful and comprehensive. Step 4: Identify the essential functions of the business and the types of threats. By doing so, you will be able to find the major areas of your business that require the highest level of business continuity. Step 5: Assess the Risks in Every Area. Here, all you need to do is quantify the information that you have gathered from the interviews. Step 6: Conduct an Impact Analysis. Here, you will need to summarize your findings based on the costs and benefits to find out further what your priorities are. Step 7: Draft the business continuity plan. You must have already got ideas regarding what to include in the plan. Include all the requirements of the plan, followed by the procedure and end goals. Step 8: Test gaps in the plan. Once you have created your plan, you must immediately test it for any gaps. You can do it by communicating with those who are implementing the plan. Step 9: Revise your plan on the basis of findings. This will be on the basis of your findings in Step 8. Here, you will need to correct the flaws that you have found throughout the process. Read More: Business Risks – How To Identify, Manage, And Reduce Them? Bottom Line Business continuity planning is essential to hasten an organization’s recovery from a major risk leading to a threat or disaster. Basically, the company identifies all the risks that can affect the organization. The continuity plan puts in place various mechanisms and functions. With the help of these, the organization allows assets and personnel to minimize the company’s downtime. In case of a disaster in the company, it is important to implement business continuity planning to provide cover for the disaster. Do you have any recommendations regarding how to implement business continuity planning? Share your views and ideas with us in the comments section below. Read More: Entrepreneur : Who Coined The Term ‘Entrepreneur’? Intrapreneurship – Definition, Importance, Duties, And Responsibilities What Is a Franchise, And How Does It Work? – Examples, Benefits & More

Sep 02, 2023

6 Common Mistakes To Avoid When Hiring A Workplace Cleaning Company

A fresh and well-maintained workplace can improve the mood and productivity of your employees. However, it’s not that easy to maintain a clean work environment. When the day is hectic, it’s impossible not to make a mess.As a business or property owner, the best thing to do is hire a professional cleaning company. Hiring a professional cleaning company is as important as running the 10 panel drug test for new recruitments. Why Hire A Cleaning Company? You could be contemplating whether hiring a professional office cleaning company is worth it. After all, you also have the option to hire employees who can handle cleaning duties instead. Plus, some businesses utilize a chore chart to delegate cleaning duties to their employees on a regular basis. So, what's the point of hiring a professional cleaning service? One significant benefit of hiring a workplace cleaning service is that you don’t have to screen and hire your own cleaning staff. This saves you a lot of time, effort, and resources. Additionally, you don’t even have to provide training since the cleaning company will take care of that. With a cleaning company, you’re assured that the cleaners you get are skilled, professional, and well-equipped to handle any kind of cleaning or disinfecting job. Moreover, you don’t have to worry about buying vacuums, mops, and any other cleaning equipment since professional cleaning companies can provide them. Common Mistakes To Avoid When Hiring A Cleaning Company Hiring a cleaning service is advantageous for both employees and the company. However, because of time constraints, most businesses make mistakes in choosing and hiring a cleaning company. The following are the most common blunders companies make when choosing a cleaning service and how to avoid them: 1. Failing To Check Licenses And Certificates There are plenty of fraudulent companies out there. Many businesses end up hiring cleaning companies that don't have the right paperwork, licenses, and certifications. Because of this, the cleaning staff and service they get are unsatisfactory. What Should You Do: Double-check the company's certificates and licenses. Inquire about their insurance, experience, expertise, certification, and licensing. In the end, hiring background cleared cleaning services will ensure you only get trained and well-equipped cleaning staff for your workplace. Aside from getting superior cleaning services, you don’t have to worry about possible theft and damages caused by ill-intentioned cleaners. 2. Neglecting To Read And Fully Understand The Service Contract An agreement cannot be deemed void simply because one party did not read or comprehend it. As a business owner, you know how important it is to have a service agreement with another company. Both sides need to know what their responsibilities are and what they can expect. If you don't know what's in the contract before signing it, you're at a disadvantage, specifically if a problem arises while the agreement is in effect. What You Should Do: Make sure to read the agreement and understand everything in it. Look for parts of the contract that talk about the cleaning service's scope as well as the company's involvement when accidents, loss, and other kinds of damage occur. Be sure that the payment terms, completion date, and other specifics of the cleaning service are all laid out in the contract. Lastly, don't hesitate to express and share your concerns if some terms and provisions are unclear. Communication is essential in every business relationship. 3. Hiring Low-Priced Cleaning Services As a business owner, you're used to looking for ways to make more money and cut costs. But when it comes to finding the right cleaning company, cheap doesn't always guarantee better services. Not all low-cost cleaning services are guaranteed to do a good job. So, instead of saving money, you wind up shelling out extra cash to hire another cleaning company to redo the job until you're pleased with the results. What You Should Do: Consider the cleaning service your company needs, and plan accordingly. Then, get estimates from several cleaning companies so you can evaluate their services and prices. From that, you can choose the best cleaning service that suits your business needs and budget. As a business owner, you may not have sufficient time to keep your office clean and tidy 4. Disregarding A Cleaning Service's Specialization Not every cleaning company is the same. Some can offer highly specialized cleaning services while some cannot. Some cleaning services focus on specific industries, such as hotels, factories, and restaurants. What You Should Do: Take the time to conduct research. The time and effort you put into research will pay off. You can easily find a cleaning service's specializations by visiting their company website. This is important, especially if you’re in the food and retail industry. Restaurants, groceries, and shops have to be cleaned and disinfected more thoroughly than a regular office establishment because the health and safety of customers are a major concern. 5. Skipping Reference Checks References can attest to a cleaning firm's dependability, competence, and expertise. Regardless of what kind of services your company needs, asking for references is a great way to learn more about the services and standards of a cleaning company. This is also a fantastic way to determine whether and how problems were resolved if a past client had any problems with the firm. This information might reveal whether the organization is dependable and professional, especially under difficult circumstances. What You Should Do: Conduct a reference check by calling the cleaning company's previous clients to learn about their cleaning skills and level of service. Check the company's website or social media accounts for client feedback and comments. If you can personally locate some of their clients, it is best to reach out and ask them for their thoughts about the company. 6. Rushing Decisions You might be in a rush to find a cleaning service so you can get back to running your business. However, picking the best cleaning service isn't something that should be rushed. It's important to carefully select a professional and reliable cleaning service for your company as they'll have access to your premises, valuable technologies, and office equipment. What You Should Do: To avoid making hasty decisions, you don’t have to hire a cleaning company right away if it’s not that urgent. If your workplace just needs general cleaning and maintenance, you may enlist some of your employees and give them additional compensation for agreeing to perform some cleaning duties. But do remember that this should be a temporary arrangement. Eventually, you need to hire a professional cleaning company for your workplace since most employees won’t like performing duties that are outside of their job description. Final Thoughts As a business owner, you may not have sufficient time to keep your office clean and tidy. After all, cleaning the entire workplace is a difficult undertaking that demands both expertise and consistency. But since your employees deserve to work in a clean and sanitary workplace, the best solution is to hire a professional cleaning company that provides trained and professional staff, along with reliable cleaning equipment. Additionals: Top 5 Types Of Businesses That Are Giving More Profits To The Sellers

Aug 18, 2022

The Rising Importance Of Vape Detectors In Business Environments

As the trend of vaping continues to grow, businesses are increasingly concerned about its impact on their premises. Vaping, while often perceived as a less harmful alternative to smoking, still presents various challenges in public and private settings. This concern has led to the rising importance of vape detectors in businesses, a technology that’s becoming crucial in maintaining health standards, adhering to regulations, and ensuring a comfortable environment for all patrons and employees. Addressing Health and Safety Concerns The primary reason businesses are turning to vape detectors is to address health and safety concerns. Vaping can release aerosols and chemicals that may affect indoor air quality and potentially harm non-vaping individuals, particularly in enclosed spaces. This is especially concerning in environments like restaurants, offices, or stores, where maintaining a clean and safe atmosphere is crucial for both employees and customers. By installing vape detectors, businesses can quickly identify and address vaping incidents, thereby ensuring a healthier environment. Complying with Regulations and Company Policies Another significant factor is compliance with regulations and company policies. Many places have strict no-smoking policies that include vaping, but enforcing these rules can be challenging without the right tools. Vape detectors help businesses ensure that these policies are adhered to effectively. They serve as a deterrent against policy violations and provide a means to enforce rules consistently. Benefits of Implementing Vape Detectors in Businesses BenefitDescriptionImpact on BusinessImproved Air QualityReduces aerosols and chemicals from vapingCreates a healthier environmentPolicy EnforcementAids in upholding no-smoking/vaping policiesEnsures compliance and reduces liabilityEnhanced Customer ExperienceMaintains a comfortable environment for allIncreases customer satisfactionEmployee Well-beingProtects employees from second-hand vaping effectsBoosts morale and productivityTechnological DeterrentServes as a deterrent against vapingReduces frequency of vaping incidents This table illustrates the benefits of implementing vape detectors in business environments, highlighting how they contribute to overall health, policy compliance, customer satisfaction, and employee well-being, and act as a technological deterrent. The Role of Vape Detectors in Customer and Employee Satisfaction Customer and employee satisfaction are paramount for any business. Vape detectors play a crucial role in ensuring that both these groups enjoy a comfortable, vape-free environment. For customers, especially those who are health-conscious or sensitive to aerosols, a vape-free environment can significantly enhance their experience. For employees, working in a vape-free environment means a cleaner, safer workplace, which can lead to increased job satisfaction and productivity. Related: Enhancing Employee Retention And Engagement With An Effective Appreciation Program Navigating the Challenges of Vaping in Shared Spaces In addition to the direct benefits of installing vape detectors, businesses must also navigate the broader challenges of vaping in shared spaces. Vaping, often less detectable than traditional smoking, can be a discreet activity, making it difficult to monitor and control in public areas. This presents a unique challenge for businesses that strive to maintain a certain standard and atmosphere in their premises. Vape detectors provide a solution to this challenge by discreetly monitoring the environment and alerting management to any vaping activity. This technology allows businesses to proactively manage their space without constant physical oversight, ensuring that all patrons and employees can enjoy a comfortable and respectful environment. It represents a balance between respecting individual choices and upholding the collective well-being of all those within a shared space. Conclusion The integration of vape detectors in businesses is a response to the evolving landscape of public health and safety concerns associated with vaping. By ensuring cleaner air quality, adhering to health regulations, enhancing customer and employee satisfaction, and effectively enforcing no-vaping policies, vape detectors are becoming an essential component of modern business operations. As vaping continues to be a prevalent habit, the use of such technology will likely become more widespread, underscoring businesses’ commitment to creating safe and comfortable environments for everyone. Read Also: 8 Best Practices For Managing Remote Teams The Importance Of Keeping Your HR Team Certified Seven Potential Tax Credits Available To Small Businesses In 2023

Dec 07, 2023