Is PHI Stock A Good Buy? Everything You Should Know

PHI stock prices have shown a positive trend in the past few months. So chances are there that you can earn big if you invest in this stock.

Before investing in PHI stock, you need to understand its background and assets to withstand the stock holdings for a longer duration.

The Company is one of the oldest conglomerates in the USA and has shown a promising growth rate over the past few years. As a result, investors in the US stock market are now witnessing PHI stock as the safest option for them in 2022.

Company Profile & Background Of PHI Group

PHI( Provincial Holdings Inc) is one of the oldest companies in the USA. In 1982, it was established with the name of JR consulting.

The Nevada Corporation is primarily into mergers and acquisition business offerings. The company’s name got changed to Provincial Holding Inc after acquiring California’s Investment banking and asset management company in 2000.

In 2009, the company’s name was again altered as the PHI Group, and now it is operating its functions in the USA smoothly.

Reasons To Buy The PHI Stock In 2022

There are several reasons you should buy the PHI stocks in 2022 to get better returns from your investments. Some of them are as follows. But, first, it will hint at why you must buy the PHI Stocks in 2022.

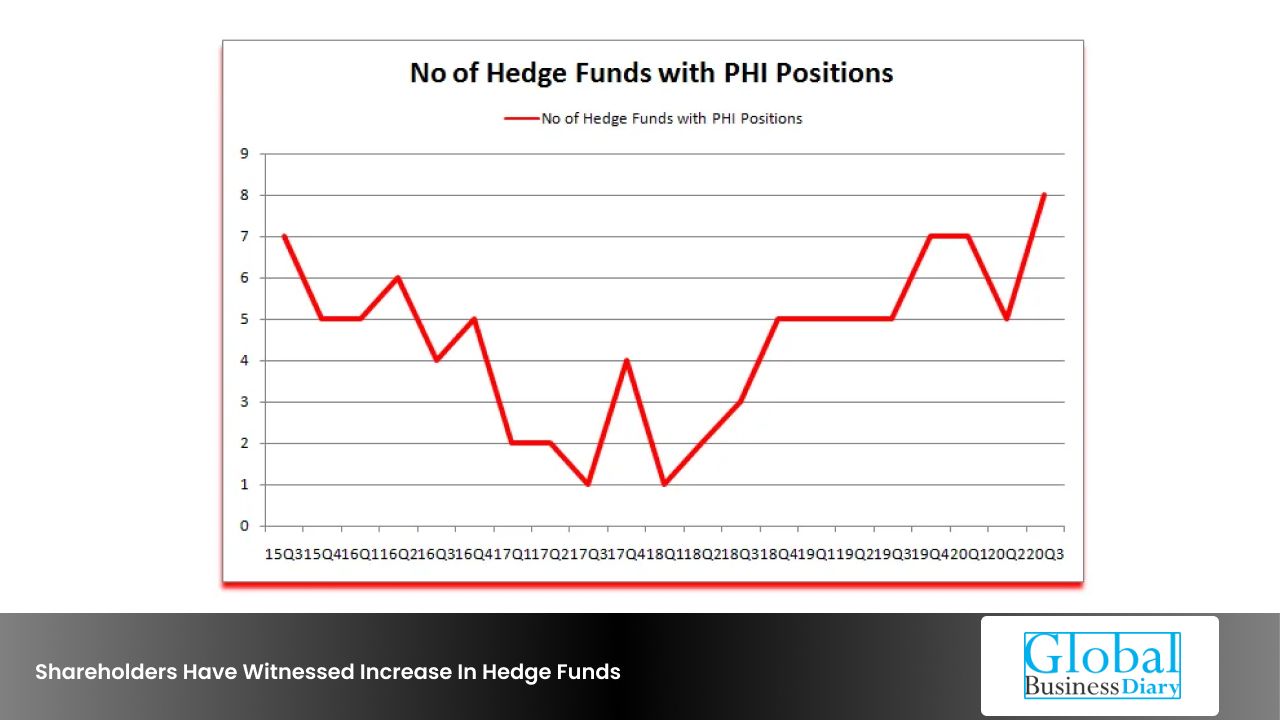

1. Shareholders Have Witnessed Increase In Hedge Funds

Shareholders have witnessed increased hedge fund interest over the last few quarters in PHI stock. As a result, it comprises eight hedge fund portfolios over the end of the third quarter in 2022.

The all-time high statistics of PHI stocks stand as 7 out of 10 ratings, and it will deliver better returns to its investors.

It comprises the bullish hedge fund situation for the stocks that sit for their all-time high. There are currently five hedge funds in all of the database positions for the PHI group.

2. PHI Stock Will Experience The Bull Run

Insider Monkey has analyzed PHI stocks, will show a bullish run in the upcoming years.

From the previous quarter, the growth rate of the stocks for the PHI group is more than 60%. Therefore, the shareholders can earn more from it if they can invest their money now. Later on, the prices of the stocks may fluctuate.

Hedge fund managers are boosting their Holdings and market caps on this stock. It is providing safe heaven to its investors during the upcoming years.

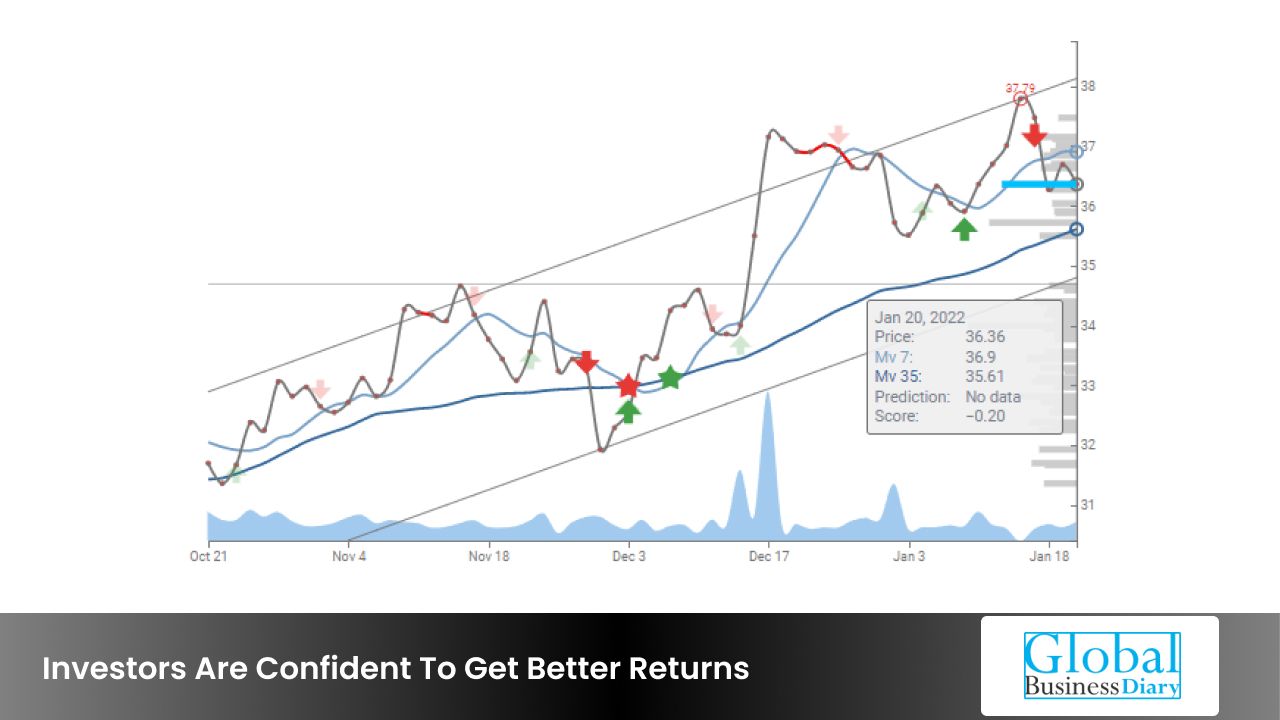

3. Investors Are Confident To Get Better Returns

Renaissance Technologies is now holding $91.5million worth of the shares of the PHI company, so the chances of returns will be higher.

The chances of earning from PHI stocks are more as bigger organizations are the clients of these companies, which ensures stable growth. Therefore, experts of the stock markets believe PHI will provide a higher stock return in the upcoming years.

The chances of price fluctuations and company debt are less. The PHI group believes in a Zero debt policy, and so PHI stock forecast will show better returns for their investors.

Also Check: Is MAX Stock A Good Buy? Everthing You Should Know

4. Agricultural Sector In US Is Showing Growth

You may wonder why I am talking about the agricultural sector in the context of the PHI group, right.

The PHI group invests its money in the Agricultural sector company’s stocks and earns the return. Currently, the stock prices of the agricultural sector are growing by 1.53 percent every year.

Due to this factor, the chances of the growth rate of the PHI group will be on the higher side, and you can get better returns from your investments. As a result, the PHI stock prices will increase rapidly and will deliver better returns for their investors.

5. Healthcare Sector Is Showing Steady Growth

The US government spends almost 18 percent of the GDP in the health care sector for its development and growth, and the PHI group also invests its money in this area.

Investors will get stable returns from their investments in PHI stocks as the management of the PHI group takes care of its investors very aptly.

The innovative leadership and out-of-the-box thinking ability of Mr. Fahman, who possesses 30years of experience in the Corporate management field and settling the Corporate management strategy, have never upset its investors. As a result, you can also expect better returns from this company.

6. Real Estate Industries Are Witnessing Healthy Returns

The average sale price of the real estate sector has increased in the past few years. Its count stands as 43 percent growth rate over the past few years.

The most astonishing fact for the investors of the PHI stockholders is that this company also invests its money in this area as well. The chances of earning more money increase when PHI makes more money from these country’s core sectors.

Do not waste your time and buy the stocks of PHI group to earn big within the next few years.

The Real estate sector will also grow rapidly in the upcoming years, and the investors will witness better returns from their investments.

Also Check: What Is SHLL? Is SHLL A Good Stock In 2022?

Final Take Away

The world market economics is changing rapidly, and countries like the USA are now showing a better growth rate post-COVID-19. As a result, the PHI stock prices will increase in upcoming years.

Experts of the stock markets are at least confident about the growth in the share prices of the PHI group. Now, you may have some different opinions about this fact.

You can feel free to share your opinions, comments, and advice in our comment box. Your opinion is valuable to us, and so we are expecting a valid reply from your end. Do not forget to share this article with your friends, peers, and colleagues.

FAQs ( Frequently Asked Questions)

More Resources:

Tags:

Recent

Due Diligence Decoded: Why Careful Evaluation Still Wins in Business

Jul 11, 2026

How Hydraulic System Design Impacts Equipment Performance

Jul 01, 2026

Startup Bootstrapped Fundraising Strategy: A Guide for SaaS and Tech Startups

Jun 21, 2026

Where Distributors Lose Profit Without Realizing It

Jun 20, 2026

Related Articles

Reducing Bad Debt: 5 Debt Collection Strategies You Must Implement

Debt and dues collection are crucial for B2B organizations because they rely on credit for their operations. Debt collection entails obtaining payments from clients in accordance with a pre-established payment schedule for the goods or services delivered. However, effective debt collection methods are required because several factors may impede the collection process. These methods can include precautions and solutions for when a debt becomes problematic, and no payments are made. It is crucial to recover customer debts because the money made from debt collection can be used for everyday operations. Businesses that don't timely collect debts risk suffering sizable losses from bad debts. The improvement of cash flow and the development of stronger client relationships both depend on a strict debt collection strategy. Two of the most difficult parts of revenue cycle management (RCM) are bad debt and collections. What Are The Challenges Faced By Debt Collection Teams? Managing past-due accounts while taking care of all the accounts on their work list presents difficulties for collectors. Unreliable and out-of-date data can result in time loss, strained customer relationships, and high DSO. Inadequate communication is essential for customer collaboration, but collectors might give non-critical clients more attention than those who need it. Moreover, in cases of international debt collection, the differences in policies and currencies can often stand as a hurdle in the way of repaying debts. As static parameters like due dates and invoice values may not be adequate to handle dynamic changes in a customer's accounts payable functions, improper customer prioritization is another issue. To ensure effective operations and maintain a strong customer relationship, finance leaders must continuously evaluate the maturity of the collections process. Strategies To Overcome The Challenges Of Debt Collection Given below are some of the most sought-after strategies used by a company and commercial debt collection agency— 1. Timely Invoices To guarantee a successful collection, sending timely and accurate invoices is crucial, giving customers enough time to plan and gather their finances. Being proactive can significantly reduce waiting time and improve productivity. Although automated debt collection software can speed up the process, it's essential for the sales and collections teams to collaborate and avoid duplication of effort to improve client satisfaction. To prevent errors that could delay payment, verifying every detail of an invoice before sending it is necessary. Double-check the unit price and rates, the appropriate person's address, the items and descriptions, and the contact information. This will help reduce errors that could cause payment delays and ensure a smoother collection process. Implementing these strategies can decrease your collection costs, increase customer satisfaction, and save time. 2. Prevent Communication Gaps Rather than chasing after bad debt, focusing on preventing it is crucial. This can be achieved by implementing responsible credit policies that will reduce defaults and increase collections. Before making any credit-based sales, it's vital to ensure that your sales team is well-informed about the credit policy and the necessary procedures for credit terms. Open communication between the sales and collection teams is essential to improve collaboration and collections. Patients can also contribute to reducing bad debt and increasing collections by staying informed about their bills and payment options. To facilitate this, reminders, statements, and notices can be sent through various channels such as phone calls, emails, texts, or portals. It's crucial to explain any charges, discounts, or adjustments and address any questions that may arise. To accommodate patients, consider offering flexible payment options, such as credit cards, online or mobile payments, payment plans, or financial aid. Patient education and communication can foster engagement and satisfaction, ultimately leading to better collections. 3. Planning Ahead Two ways businesses can increase collections are by prioritizing customers and keeping an eye on accounts' aging and the amount owed. AI-based collections software can assist businesses in scheduling and prioritizing customer calls, accelerating the recovery of receivables by identifying high-risk clients, predicting payment schedules, and providing specialized dunning strategies. Patients' bills and payment options can be explained to them, lowering bad debt and increasing collections. Giving patients flexible payment options can increase their satisfaction and engagement. Higher collections may also result from patient education and communication initiatives. Software for automated accounts receivable collections can aid in simplifying this issue. By helping to develop collection strategies based on customer payment history and behavior, AR automation software can save time and help collection agents know where to go, speeding up the collection process. Businesses can increase collections and patient satisfaction by prioritizing accounts and implementing patient communication and education. 4. Effective Documentation Improving coding and documentation practices is key to reducing bad debt and increasing collections. This can be achieved by using standardized codes, following coding standards, gathering relevant clinical data, and reviewing claims before submission. By doing so, it's possible to increase reimbursement rates and lower the amount of money owed. Moreover, lenders can make use of CRM to effectively track and follow up with defaulters, predict recovery, and facilitate faster debt collection. Keeping accurate records is crucial for tracking unpaid debts, prioritizing debt recovery efforts, and identifying critical dates such as the last payment dates, which help determine whether a debt is statute-barred. Dishonest clients often deny their debts, so recording transactions at every stage is essential to avoid such tactics and ensure accurate debt collection. 5. Sign Up Contracts And Agreements Many small businesses avoid using service agreements and contracts with their customers because they worry it might put them off. However, leaving disputes unresolved can result in significant legal and financial liabilities. Although contracts can be complex legal documents, they are essential in safeguarding both parties by ensuring they understand and fulfill their obligations. Service agreements, on the other hand, are less formal and may not be enforceable in court if a dispute arises. Having a written agreement signed by both parties is best because it clearly outlines the terms of the agreement. Contracts and service agreements are crucial for maintaining a positive working relationship with customers while also safeguarding the interests of both parties. Role Of A Debt Collection Agency A commercial debt collection agency is a company that helps lenders recover overdue or unpaid debts. They work closely with lenders to create payment schedules, locate debtors, and negotiate debt payments. Collection specialists, also known as collections agents, act as intermediaries between creditors and customers. They keep a close eye on accounts to identify past-due payments, report collection activities, respond to client inquiries, and establish repayment plans. They may also discuss debt settlements for repayable debts. Read Also: contribution margin: what is it, overview, examples, and more business risks – how to identify, manage, and reduce them? the best risk mitigation techniques for your business

Oct 02, 2023

Trial Balance: Definition, Working, Importance, And More

In a trial balance, the report of the ending balances of different ledgers of a particular company are available. It is the first statement you will need to prepare as an accountant to check the correctness of the double entry of any business accounts. To ensure that the accounts of a business are correct, having good knowledge of trial balance is necessary. Basically, with the help of trial balance you can minimize the errors in the company’s financial statements. In this article, you will learn about wha trial balance is, and what are its constituents. Apart from that, you will also learn how a trial balance works in general. Next, we will show a step-by-step procedure of how to prepare a trial balance with respect to your company’s financial statements. Finally, you will learn some rules to follow while preparing a trial balance. Hence, to learn more, read on through to the end of the article. What Is Trial Balance? - Definition According to Investopedia, “A trial balance is a bookkeeping worksheet in which the balances of all ledgers are compiled into debit and credit account column totals that are equal. A company prepares a trial balance periodically, usually at the end of every reporting period. The general purpose of producing a trial balance is to ensure that the entries in a company’s bookkeeping system are mathematically correct.” The trial balance basically consists of the test of the fundamental aspect of a set of accounting records (that is debit and credit). Only after the trial balance process, you will be able to move to more complex and detailed analyses. Read More: What Is An Angel Investor, And How Does Angel Investing Work? How Does Trial Balance Work? Basically, the trial balance is a tool that you, as an accountant, is using to check the accuracy of the general accountant ledger. Apart from that, it also helps you to ensure that the errors in the financial statement are minimal. The internal financial reports through the trial balance can help you to verify the double-entry accounting system’s accuracy. In addition to that, you can also identify eros before the issuing of the critical external financial statements. The Wall Street Mojo adds here - “Trial Balance is the report of accounting in which ending balances of the different general ledgers of the company are available; For example, utility expenses during a period include the payments of four different bills amounting to $ 1,000, $ 3,000, $ 2,500, and $ 1,500, so in the trial balance, single utility expenses account will be shown with the total of all expenses amounting $ 8,000.” How To Prepare A Trial Balance? In general, accountants create a trial balance manually. However, with the coming of various accounting software systems, accountants use them as well, when it comes to several transactions and investments. If you want to prepare a trial balance, make sure to take the following steps: 1. Make Sure to Balance The Ledger Accounts Here, you will need to record all your transactions as journal entries, and make entries in respective ledger accounts. Then, calculate the closing balances of each ledger account. You will have to take these to the trial balance. 2. Prepare A Worksheet Create three separate columns - one to contain the names of each ledger account, one for debit balances, and the last one for credit balances. You can also optionally enter account numbers and other details. 3. Complete The Worksheet In the worksheet, fill the names of each account that you are loading in the worksheet. Apart from that, enter the total debits and credits for each ledger account for the accounting period. Make sure all the information is correct. 4. Add Values In The Columns After you have filled up both the columns, you should add up the values in each column to find the total in each case. If the ledgers are correct, then the totals of both the columns should be equal. 5. Close The Trial Balance If the values in both the credit and debit column are equal, you can close the trial balance. If they are not equal, consider finding the common errors, and rectify them. Preparing A Trial Balance - A Few Things To Consider According to Indeed.com, “While computing the trial balance, you input the balances of these ledgers into debit or credit account lists in separate columns. It is necessary that the total amount in each column is equal. To ensure that bookkeeping entries are continuously correct and balanced, businesses typically perform trial balances at the end of each accounting period.” Here are a few rules to consider if you are preparing a trial balance so as to avoid any errors: Make sure all the liabilities are in the credit column and all assets are in the debit column. Make sure the gains and revenues are on the credit side of the balance. The losses and expenses for the investment should go on the debit side of the balance. While preparing the trial balance, make sure to consider the nominal, personal, and real accounts. If a ledger shows zero balance, avoid it. Include the opening stock figure in the profit and loss account. You can show the sales and returns in two ways. The first way is to show them as reductions from the original purchase and sales ledger. The second way is to show them as separate line items in the trial balance. At the end of the trial balance, the debit and credit balance need to be identical. Read More: What Is A Venture Capitalist, And What Are Their Functions? Wrapping Up Hope this article was helpful for you in getting an idea of what trial balance is, and how it works. It is basically a worksheet where you will get two columns - one for credit and the other for debit. By matching the balances of these two columns, you can ensure that your company’s bookkeeping is mathematically correct. The debits and credits are the company’s transactions. All the debits and credits of the company over a given time must tally so as to ensure that there is no error in calculation. However, there could still be mistakes or errors in the accounting system. Do you have any suggestions for preparing a trial balance report? Share your ideas and info with us in the comments section below. Read Also: How To Start An Insurance Company? – Steps You Must Take Entrepreneurship In Economics: What Role Do Entrepreneurs Play In Economics? Which Of The Following Is Not A Creative Thinking Exercise Entrepreneurs Use To Generate Ideas?

Sep 29, 2023

Consideration For Choosing Or Comparing Credit Cards

Choosing the right credit card, also known as charge plate or plastic money, is an important decision that can offer valuable perks, financial flexibility, and benefits. In this article we’re going to be assessing a number of factors with the aim of making the right decision while choosing the card. Consideration will be given to payment flexibility and terms, credit card types, network, and terms and conditions. Lastly, thoughts will also be given to its universality. Comparing Credit Card Payment Flexibility and Terms and Terms There is not an iota of doubt on the fact that credit cards have offered innumerable benefits to people. Amidst their different facilities, flexibility is undoubtedly one of them. It has undoubtedly provided the necessary convenience to people. We shall compare payment flexibility and terms associated with plastic money. To get information on comparing credit cards visit: https://moneywise.com/. Analyzing Payment Flexibility Options Across Credit Cards Some cards have a flexible due date that suits your financial situation and allows you flexibility in managing payments. We all know that the management of payments is indeed one of the biggest challenges entrepreneurs face in their day-to-day lives. Another form of control offered by other cards is the adjustment of minimum payment based on financial capacity. Other flexibility options on the block are the allowance to select how often you make payments such as monthly, bi-weekly, etc. Evaluating the Importance of Payment Terms The impact on payment scores positively influences your credit score, while late payment significantly affects your reputation. Payment terms influence interest accrual on the outstanding balance, so it shouldn’t be ignored. Fees and penalties are imposed based on payment terms; it’s why it is important to adhere to due dates. Responsible Credit Card Usage for Optimal Payment Terms Timely payments help in maintaining optimal payment terms that affect your financial standing positively. Also, note that if you maintain a low monetary utilization ratio by not exceeding your threshold, your payment management terms will be effectively enhanced. Related: Credit Card Frauds And What You Can Do To Avoid Them Comparing Credit Card Type and Network Plastic money, as a versatile financial tool, offers a variety of benefits depending on network affiliation and types. Understanding Credit Card Types Credit cards have undoubtedly revolutionized the entire payment system. They not only helped with the quick transfer of money but also facilitated business development. However, we understand the different types of credit cards in this section. · Secured: This card type is good for people rebuilding their credit card history. It requires a security deposit. · Unsecured: These are the most common types used to cater to a wide range of financial needs and require security deposit. · Reward: Rewards or incentives such as cashback, points, or miles depend on your spending pattern. You will find different reward offers from different providers. You should therefore choose one that suits your lifestyle. For example, you can compare Amex Gold vs Chase Sapphire Preferred to see what each offers before making a choice. · Student: These types are designed for students to help them establish their credit history. These card types have lower monetary limits. Analyzing Different Credit Card Networks Different types of plastic money are available in the financial market. The main ones are - · Visa: This option is versatile with extensive network offerings. It is widely accepted globally and caters to various consumer needs. · Mastercard: This option is also accepted globally and comes with different beneficial offers and perks that make it a popular choice among consumers. · American Express: This premium credit card type is favored by customers seeking rewards and luxury. The American Express is also known for its exceptional customer service. · Discover: Discover doesn’t have any annual fees and is good for individuals looking for straightforward rewards such as cash-back rewards. Comparing Terms and Conditions of Plastic Money Plastic money has ushered in a revolution in the entire circle of the payment system. However, we try to understand some of the ways through which the entire payment system. Different financial organizations have their own terms and conditions for their credit cards. Terms and conditions are laid out guidelines and rules governing the operations and responsibilities of both the issuer and cardholder. Key Comparison Factors Interest rates, credit limits and penalty charges are some of the critical terms and conditions to watch out for when signing up for the plastic. You should carefully note the penalties imposed for late payments, exceeding the threshold, or other infractions. Making Informed Decisions Based on Terms and Conditions Before committing to terms and conditions you’re encouraged to read it thoroughly. By comparing these terms with those across multiple offers, you’re likely to find the best suited for you. Assessing Credit Card Versatility: International Use Plastic money offers flexibility and convenience for transactions worldwide as a financial tool because of its ubiquity and its technological integration. They facilitate seamless currency conversion, allow for online transactions and, above all, enjoy global acceptance providing a comfortable payment option for travellers. Comparing Plastic Money Networks for Global Usability American Express, Visa, Mastercard and Discover are common monetary instruments that have gained extensive worldwide acceptance and used globally for transactions by travelers. This has made them the preferred choice for many individuals the world over. Merits and Demerits of Using Credit Cards Internationally Convenience, a secure way of making purchases and the accrual of rewards and benefits are some of its advantages. Drawbacks such as incurring foreign transaction fees and exchange rates, which may not be favourable may be applied by the plastic money companies. You can read this article to learn more about this international type of payment. Conclusion With comparison from the standpoint of information, one can make choices that best align with one's lifestyle and financial goals. However, a good understanding of its diverse landscape, terms, conditions, and other factors is crucial to making the right choice. The right card is the key to optimizing your financial experience while traveling or making international purchases. Read Also: The Amazon Store Card All You Need To Know About California No Credit Check Loans: A Solution For Those With Poor Credit Home Credit: Information, Eligibility Criteria, Interest Rates, Review & More

Oct 20, 2023

Credit Card Frauds and What You Can Do to Avoid Them

As of 2021, the most common payment method out of all the fraud reports in the US was credit cards. In 2020, when the world was battling COVID-19, there were a total of 459,297 cases of such fraud. Most of these fraud victims were between the ages of 30 and 39, the target demographic for credit card issuers. As a result, theft by credit card fraud increased by almost 45% compared to 2019. Credit card fraud is one of the biggest threats today’s eCommerce industry faces. No one’s bank account is entirely safe from these perils, from credit card theft to credit card data breaches. A card issuer does their best to stop offline and online transactions from a stolen credit card whenever they suspect fraud. It’s also possible to recover funds from credit card fraud via a funds recovery company. These companies can easily back you up as long as you have sufficient evidence. However, you to be vigilant as well regarding this issue. So, here are a few things you can do to avoid credit card fraud. Never Save Your Credit Card Details In 2021, Google sent millions of users a chilling email when it told them their passwords had been compromised. The data breach exposed millions of users’ saved login and payment credentials. You often save your credit card information on various websites. The purpose is that you don’t have to re-enter the same details the next time you want to buy something from them. However, hackers can access your information when they manage to breach the website’s security measures. As a result, your credit card information is no longer safe. It might already be too late by the time you get to know it. Scan Your Computer and Phone for Virus and Malware The number of online transactions reaches the million mark almost every day. Most of these are credit card transactions, where people are buying stuff online. Since you’re either using your mobile or PC for this, you must make sure no one is snooping on you and your credit card information. Scan your PC and smartphone for viruses and malware. Hackers and scammers can access confidential information on your devices by planting a backdoor. At the same time, you should be careful while installing third-party software on your devices. Read : What Is Stockinvest? Is It Legit And Working In 2022? Use Stronger and More Secure Security Measures Not saving your login credentials and credit card information will go a long way in protecting you from fraud. However, you can still do more to protect yourself from credit card fraud. Using a secure password should be your priority. Use a mix of alphabets, symbols, and special characters to compose the password. Never use guessable passwords like your birthdate or pet name. Look into other ways of securing your devices. Biometric authentication is a highly efficient way of doing so. After all, it won’t be easy to replicate your eyes, face, or fingerprints. Don’t Use Your Credit Card On an Insecure Website Never purchase anything using your credit card on a website without an SSL certificate. The SSL certification verifies that the website encrypts sensitive information passed between the user and the server. No SSL certificate means that anyone can snoop on that information. When you wish to install an SSL certificate make sure it is from a reputed CA like RapidSSL, GlobalSign, DigiCert, etc. A few well-known certs are popular among developers including RapidSSL wildcard Certificate for subdomains, comodo multi domain SSL, and Thawte SSL for a single domain. A site owner can choose as per the site's requirements. When using your credit card online, you send your card number and security pin to the receiver’s server. Anyone with the right tools and brains can snoop on these exchanges and steal your credit card information. That is even worse than when someone steals your credit card. With credit card theft, you’ll at least know that someone stole it. There’s no easy way to tell if someone stole your credit card information during the transaction process. Be Careful While Using Your Card When using your credit card, keep the following points in mind. Make sure the card reader at the ATM is not loose. Cover your pin as you enter it into the machine. Never let anyone use your credit card. At the same time, never tell your credit card pin to those at the payment terminal or counter of the store. Immediately call your card issuer and block the card if you lose it. Read more : PooCoin Stock Forecast: Everything You Should Know. Be Aware of Unauthorized Transactions Always keep your credit card bills in check. When you spot an unauthorized or suspicious transaction, notify the credit card company. Don’t risk keeping your card active at that stage. Your credit card issuer will also notify you when it sees that you’re trying to make a transaction to a suspicious or blacklisted website. Listen to their reasons for the notification and possible transaction block. Avoid using your credit card on those sites if possible. Credit card fraud will continue as long as people are not careful about how they use it. So, your best bet to avoid these frauds is to ensure you stay extra cautious all the time.

Apr 22, 2022