Instant Loan App: Top 25 Best Loan Apps Should You Know In 2023

With the rise in the level of digitization, there has been a simultaneous rise in the number of instant loan apps in the last few years. As per various sources, in the year 2022 itself, the demand for personal loans surged by 50% in the retail industry. However, a very interesting fact is that in the disbursement of personal loans, non-banking financial institutions were on top of banks.

In this article, we will mainly discuss the top twenty-five instant loan apps that offer personal loans in 2023. These are the best loan apps that will allow you to avail of loans fast. However, these apps come with different types of service options, and the time of disbursal changes with the app. Hence, to get fully informed, read on through to the end of the article.

The Best 25 Instant Loan Apps In 2023

The following are the best instant loan apps that you must look for before you try to avail yourself of personal loans fast in 2023:

1. Earnin

If you are qualified to get loans in this app, you can get an emergency loan from this app if you are confident to pay it back. The advances are large.

2. Chime

This is one of the best $50 Loan Instant Apps if you are looking for payday loans. However, lenders can still charge high interest.

3. Current

The best thing about this app is that there are no overdraft fees associated with it. Furthermore, you can get overdraft protection of $200.

4. MoneyLion

You can get an instant cash advance of up to $300 dollars, and you can also be able to access and improve your credit score.

5. Brigit

This is one of the best cash advance apps. If you are an eligible member, cash advances are available to you between #50 and $250.

6. Dave

This is one of the best $100 loan instant apps that you will come across. Cash advances start here at only $5, and there is also automatic overdraft protection.

7. Spotloan

Once you do a SpotLoan login, they will inform you, “It’s an installment loan, which means you pay down the balance with each on-time payment.” It means that it is not a payday loan app.

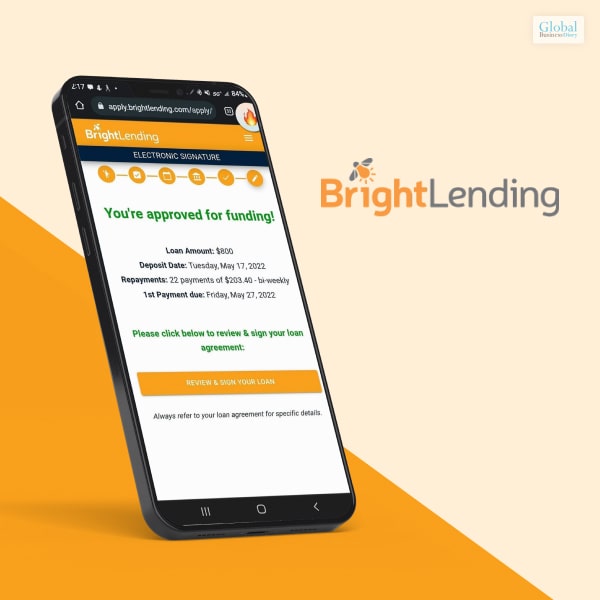

8. Bright Lending

You can get loans from $300 to $1000, but there are also triple-digit APRs, as well as short terms for repayment.

9. Cash App

How to borrow money from Cash App? The Cash App borrow loan services allow you to use the app and access loans from multiple devices using the tag “$cashtag”.

10. MoneyLion

With the help of Moneylion NYC, you will be able to avail of credit-builder loans without a credit check if you are a member.

11. SoFi

The best thing about this loan app is that you can get even $5000 to $100,000 loans and can get your funds on the same day.

12. PayActiv

You can get here early paycheck access, and also you will be able to get up to 50% of earned wages before your payday.

13. Even

If you are eligible, you can get up to 50% of your earned wages early, and you can get budgeting tools to track your spending as well.

14. Branch

Apart from getting 50% of your earned wages early, you will also benefit from no credit checks and zero-cost loans.

15. Grain

If you have low credit scores, then this is one of the best loan apps for you. This is also great if you have a short credit history.

16. Vola

If you are able to pay a monthly fee, with the help of Vola, you can permanently avoid overdraft fees with the help of instant cash advances.

17. Empower

Borrowing a small number of finances can be easy with the help of the Empower Loan App. Furthermore, there are budgeting tools to track expenses.

18. CLEO

The app uses AI to help you analyze your spending and help you by giving actionable insights as well. You can also avoid overdraft charges with the help of rewards and auto savings.

19. SoLo

Once you apply for a loan here, you will get a soft credit check, which will not affect your credit score. However, based on the credit check, lenders will have a better idea in regards to lending their money to you.

20. Upgrade Personal Loans

You can get fast loans with Upgrade, You can get loans up to $50,000. However, there is a high origination fee associated with the borrowing.

21. Varo

Apart from being a loan app, this is also a bank account, which gives you an account with a minimum balance with no monthly charges or overdraft. Furthermore, the credit card option is also secure.

22. Albert

According to Business Insider, “Albert is a financial app offering automatic savings tools, cash accounts, cash-back rewards, auto-investing, and much more.” However, you can get some customer service issues, as per complaints of borrowers.

23. LendJet

Although not a direct lender, you can get access to a variety of lenders through this platform. Hence, it will be easier to look for personal loans from various options.

24. ZippyLoan

Like the other platforms, ZippyLoan also offers you to choose from a variety of lenders. You can get loan amounts from $100 to $15,000.

25. Viva Payday loans

You can apply for loans in this app without having a credit history for yourself. The loans are hassle-free, and you will get fast approvals as well.

Summing Up

Hope this list is informative enough to give you a better idea of the best instant loan apps in 2023. If you are trying to avail of fast loans, then you must try one of these apps mentioned above to get the best services. However, we will still recommend you read all the information related to availing of loans.

This will give you a better idea of what services are offered by the loan app that you are taking a loan from. Which of the aforementioned loan apps do you think is the best option for you? Share your reviews with us in the comments section below.

Read Also About:

Tags:

Recent

How Hydraulic System Design Impacts Equipment Performance

Jul 01, 2026

Startup Bootstrapped Fundraising Strategy: A Guide for SaaS and Tech Startups

Jun 21, 2026

Where Distributors Lose Profit Without Realizing It

Jun 20, 2026

Building Better Warehouse Traffic Flow Through Operational Design

Jun 20, 2026

Related Articles

What Is IPO (Initial Public Offering) Stock And How To Buy It?

Do you want to buy the IPO shares & stocks to get better ROI from your investments? If yes, then you have to clear your fundamentals and some of the basic ideas about it. The basic rule of thumb is to make your concepts clear about the market trend to make your investments. You have to take care of some crucial aspects while making your investments in IPO( Initial Public Offering). First, you must be aware of the IPO's full form before making your investments in it. Before you invest your money in IPO stocks, you need to do certain things and plan to succeed. What Is An IPO? An IPO is an initial public offering where the private company becomes public while selling the shares to the stock exchange. In most cases, private companies work with investment banks for bringing their shares to the public. In most cases, it requires a tremendous amount of diligence and regulatory requirements. Importance Of IPO For Businesses? The application of an IPO helps to improve your business in the correct way. It can help you to develop your business to move to the next level. Some of the core importance of IPO are as follows:- It can help your business to gain the public's confidence. IPO helps your business to underwrite the shares and stocks for the business. This deal helps you negotiate with the investment banks. The red herring will give the investors the confidence to make their investments in the IPO. The success of the IPO is a very complicated journey. It can help your business to grow in the correct direction. IPO plays a critical role in developing your business in showcasing the business goals and future plans to its investors. It creates a legally binding contract between the insiders and underwriters. The IPO fixes the share prices of the company and the bid is based on the range of companies.These are some of the factors that you have to take care of while you want to develop the IPO of your business. Do not make your choices in the wrong way while developing your business. Try to achieve your goals in the best possible manner to make things work in your favor. Proper application of the IPO can help your business to grow in the right direction. Essential Factors You Need To Focus On While Investing In IPO There are certain key factors you need to put your focus on while investing your money in IPO. Some of them are as follows:- The financial health of the business where you want to invest. Market volatility rate of the company’s shares in global as well as in the domestic market. The growth potential of the company where you wish to make your IPO investments. Stability of the company in upcoming years in the global business world. Who are the core competitors of your company and from whom you are seeking the initial investments? These are some of the critical factors you need to focus on while making your investments in the initial public offerings. First, work out the plans well before executing them. What Is The Process Of IPO Allotment? There are certain crucial processes that you need to take care of while allotting the IPO shares. Some of the IPO allotment processes are as follows:- The total number of successful bids is less than and equal to the number of shares offered by the firm. The total number of successful bids can be more than the number of shares offered by the firm. specific What Is IPO Grey Market Premium? Grey market is an unofficial market where individuals buy and sell IPO shares before they are launched officially in the market. If you are trading for the stock exchange, then this factor will work well in your favor. However, one of the essential facts here is that you need to stay cautious before investing your money effectively. IPO Meaning And Its Importance In Today’s Business World IPO means initial public offering. The concept behind it is that a privately owned company first lists its shares on the stock exchange and allows the public to purchase its shares from the stock markets. This list of companies that had their ipo in 2018 could be a useful guide to see how trends are shaped after the initial launch. You need to be very careful while you make your investments in the IPO shares of your company. Importance Of IPO For A Company There are several advantages a company can gain while they list their shares in the stock exchange in the form of an IPO. Considerable importance of IPO is there for your business. Businesses can get more advantages while they make their investments in an IPO. You have to understand the different types of markets where the company works. Some of them are as follows:- 1. Fundraising The most often known advantage of the Initial Public Offering is money. From the year 2016, the first milestone that the IPO shares have hit was $94.5 million. Many companies have brought millions and hundreds of dollars from IPO offerings. You cannot get more advantages compared to this. You will get the new investment opportunities that are available for new capital. 2. Exit opportunity When any company lists its shares in the stock exchange, and more people buy their shares, the shareholders’ stakes become higher. Thus, every company has stakeholders who invest ample time, money, and resources that are left with them even after not getting any fair returns from their investments. Moreover, the IPO offers investors the opportunities to exit the market whenever they want, making the system more flexible. 3. Credibility And Publicity If a company expects to develop its business, then the IPO will be the best option for them. Now, in a nutshell, let’s find out how a company can increase the credibility and publicity of its business with the help of IPO offerings:- It increases the thrusts and exposure of the company in the public spotlight. Analysts worldwide will provide the news through news channels about the latest public offerings to guide the clients on where to invest. This factor will increase the popularity of your brand as your IPO shares will become the hot topic for the news channels. Companies will not only enjoy a great deal of public attention, but they will also gain credibility from the market. For investing the money on the IPO of any company, shareholders and the general public will scrutinize every aspect of your brand; it will increase the brand awareness reliability in the market. You need to identify the IPO status from all aspects before making your investments. 4. Reduction In Overall Cost One of the significant obstacles for any company or the younger private companies is to arrange the cost of capital they invest in building their brand. However, the burden of the overall cost of capital will reduce when you release your IPO shares in the market. For running your business successfully, you need to make the arrangements of daily working capital. For example, when a startup business offers an IPO, they receive the required funds to develop their business from the initial level. 5. Make Use Of Stocks As A Means Of Payment Public companies make use of their stocks for trading, while private companies make use of the stocks for making the payments that are essential for them for making a favorable exit. So you have to make your choices of the stocks in the correct order in a short period. Public stock can offer you the payments on the market prices bought and sold in the market. So work out the best plans that can have a considerable impact on your business. Fortunately, the stock prices are those kinds of currency that can be traded in the market as and when required. So work out the best plans that will have a considerable impact on your business whenever any business uses IPO. What Are The Upcoming IPO In The USA? It is the best time to invest your money in this upcoming IPO in the USA to get better returns from your investment at the end of 2021. Company Name Proposed Symbol Exchange Price Range Shares Week off Austin Gold Aust NYSE American $4.0-$6.0300000015-11-2021Braze Brze Nasdaq $55-$60800000015-11-2021Iris Energy IREN Nasdaq $25-$27826923115-11-2021KinderCare Learning Company KLC NYSE $18-$2125,775,43415-11-2021Sono Group SEVNASDAQ$14-$1610,000,00015-11-2021Sweet Green SG NYSE $23-$2512,500,00015-11-2021 What Are The Upcoming IPO In India? A country with 130 crores of the population comprised of billions of shareholders will provide you with the best investment opportunity in 2021. Some of the essential Upcoming IPO In India are as follows:- Company Name Category Of Business IPO Size IPO Month Emcure Pharmaceuticals Pharmaceuticals Rs 4500 Crores Nov 2021Skanray Technologies Pharmaceuticals Rs 400 Crores+OFS Nov 2021 One 97-Communication (Paytm)Digital Plays Rs 18300 Crores Nov 2021PB Fintech Policy Bazaar Digital Plays Rs 5625 Crores Nov 2021Mobikwik Digital Plays Rs 1900 Crores Nov 2021Ixigo Digital Plays Rs 1600 Crores Nov 2021 All the names of the companies mentioned above will soon open up their IPO. You must stay tuned with my next article to get the complete details on it. Steps To Follow While Buying IPO In The USA There are specific simple steps you have to follow while making your investments in IPO in the USA. First, you need to know the ways before you make your investments in the IPO. Second, do not forget to follow the steps properly before making your investments. Even a tiny mistake can prove to be harmful in stock market investments. 1. Create An Online Account With The Broker Who Offers IPO Access In America, Brokers like TD Ameritrade and Robinhood offer IPO trading opportunities. You need to create an account there to start your trading business in IPO. You can create an account with them or with similar brokers to get started with your IPO trading. 2. Meet The Eligibility Requirements Only having an account is not enough for your IPO trading business. There are specific eligibility criteria you need to meet while you want to start your trading in IPO. The eligibility criteria for creating an account vary from one broker to another. The broker can hold some of your assets with them to provide you the trading opportunities in the world market. Therefore, you must have a certain amount of assets with you to become an active trader. For example, if you want to get a membership in TD Ameritrade to become a trader, then you must have $250000 in your account to start your trading. In addition, you need to have a record of trading for the past 30 times in the previous three months. 3. Request Shares Once you meet the eligibility requirements, you have to request the shares from the brokers. It is guaranteed that you will get the required shares because you ask them. Brokers will get the necessary shares, and the chances are that you do not receive any of the claims. You can place an order or any kind of conditional offer to buy. It will become an action unless the IPO is priced. You will have the chance to change the required order once the prices have been set the time when the window closes. You can’t buy new shares unless you make the price hike as per the indication of your order. 4. Place an Order Whenever you go for a trade order, you can have a conditional offer for buying the shares. You will get the chance to confirm the change once the order’s pricing has been set before the windows close. You can buy more shares as you will be requested to buy more shares unless you pay the higher prices indicated in your order. Work out the plans that can help you deliver the higher prices as indicated in your order. Steps To Follow While Buying The IPO In India There are several steps you have to follow while you want to buy the IPO in India. Don’t miss any of the steps, as each step is crucial for your trading business and its future prosperity. 1. Read The Red Herring Prospectus A company that wants to sell their IPO’s in the market has to draft and file the Red Herring Prospectus to SEBI. This process a company has to follow while selling the company’s shares to the investors. DRHP ( Draft Red Herring Prospectus) this document elaborates where and how the company will use the money. Before investing in it, an investor must go through it. 2. Make Appropriate Utilization Of Proceeds You must become a cautious investor in IPO as you must understand where your IPO proceeds will be used. For example, if the company provides the declaration to repay the debts, it is not a reasonable choice to consider. But, on the other hand, if the company raises funds to partly pay the debt and use the rest amount in the expansion of business, it can be a reasonable choice for you to make investments in IPO. 3. Understand The Business Without understanding the nature of business, if you invest your money in the IPO of any company, it can be a significant setback for you. The capital stock of a company and its share values depend on its current demand and profit earning capacity. You have to understand these facts before investing your money in IPO. In addition, the market capture capacity of a company is also a crucial fact here. 4. Management Team And Promoter Background A cunning investor must go through some of the crucial factors while investing their money in the IPO of any company. Some of these core factors are as follows:- It is essential to know the strength of the management team that is running the company. Take a look at the managers and operators of the company who are associated with the company’s daily affairs. The average number of years top management have spent their time in the company. Work culture and the attrition rate of the company you must consider before making your investment. 5. Potential Of The Company In The Market You have to understand the potential of the company in the market before investing your money in it. Investors can quickly analyze the potential of the business in the market and its prospects. A company that performs well after raising the capital can be trusted by the investors. Investors will gain better returns from the investment if the business model is good and can sustain for a longer duration. So work out your plans well before making your investment. 6. Key Strategy And Strength Of The Company Investors can sort out the key strengths of the company by identifying the DHRP. The current position of the company can be traced to the industry where it operates. When you read more about the company, then you will have a clear idea about the positioning and the strategies of the business where its works on. Growth Of IPO And Market Size Trend Analysis Year On Year Basis Final Take Away Hence, these are the current IPO status in the world market as well as in India. You need to make the right investment strategies that can work well for your business. Work out the best plans that can help you to get better returns from your investments. Do not make your choices in the wrong direction while you plan the make the investments in the IPO of shares. Frequently Asked Questions(FAQ's) [su_accordion class=""] [su_spoiler title="1. Is Buying An IPO A Good Idea?" open="yes" style="default" icon="plus" anchor="" anchor_in_url="no" class=""]Depending on the market trend and market situations, you must start buying the IPO of a company.[/su_spoiler] [su_spoiler title="2. Is It Bad To Buy An IPO?" open="no" style="default" icon="plus" anchor="" anchor_in_url="no" class=""]Buying the IPO is not a bad idea but knowing the market status of the company and its share value projections is a bad idea to buy the IPO.[/su_spoiler] [su_spoiler title="3. What Are The Top 5 IPOs?" open="no" style="default" icon="plus" anchor="" anchor_in_url="no" class=""] The list of top 5 Ipo in the Upcoming months are as follows:- Bumble Instacart Nextdoor Petco Robinhood [/su_spoiler] [su_spoiler title="4. Does IPO Always Gives Profit?" open="no" style="default" icon="plus" anchor="" anchor_in_url="no" class=""]You can receive the dividends from the company when you sell the shares in the open market in an IPO. You need to track the market trend to earn a profit from IPO.[/su_spoiler] [/su_accordion] Read Also: Why Create A Powerful Business Continuity Plan? How To Start A Business In 2021 – Best Business Strategies Is Nykaa Going To Dominate The Market With Their Recent Launch?

Nov 15, 2021

5 Most Common Human Errors In Crypto Accounting

Crypto accounting is a complex and challenging task that requires a deep understanding of how the emerging market of cryptocurrencies works. While traditional accounting is straightforward, experienced accountants struggle to comprehend how risk interplays with crypto's market and how underlying technologies protect investors. This makes it difficult for regulators to make informed decisions and entrepreneurs to manage risk in their projects. However, most of the challenges in crypto accounting arise from simple human errors, and everyone in the crypto world could use some help to manage their accounting better. One way to minimize these errors is by using crypto accounting software, which simplifies tracking and managing crypto transactions for individuals and businesses. 5 Common Mistakes to Avoid in Crypto Accounting 1. Incorrect Cost-Basis Calculations If you've engaged in crypto transactions, it's crucial to understand the impact they may have on your taxes. One common mistake to avoid is miscalculating your cost basis and capital gains. The cost basis is the total amount paid to acquire the crypto, including transaction fees, while capital gains refer to the proceeds from the sale minus the cost basis. To calculate the cost basis and capital gains, you'll need to use specific formulas. In a simple example, if you bought crypto for $10,000 (including $35 in transaction fees) and later sold it for $50,000, your capital gains would be $40,000 since you'll have to face a $10,000 fee. However, if you traded one crypto for another, such as selling bitcoin to purchase ether, this counts as two separate transactions, and the cost basis of your ETH would be the amount paid, including fees. It's essential to keep accurate records and avoid mistakes that could result in penalties or interest on underpaid taxes. 2. Incorrect Spreadsheet Formulas Even the most intelligent individuals can make simple errors, which can result in significant consequences. For example, TransAlta lost 10% of its annual profits due to a spreadsheet mistake. Although it is challenging to identify spreadsheet errors in traditional accounting, it is even more difficult in the world of crypto accounting, where the complexity of the data can make it difficult to recognize an error until it is too late. To avoid spreadsheet mistakes, it is crucial to be extremely careful when using spreadsheets and, if possible, utilize more advanced tools. Finding a platform or service where you can reconcile your calculations and results to ensure accuracy is also recommended. Reducing reliance on human accuracy can further help to avoid spreadsheet errors. By taking these measures, individuals can significantly reduce the chances of spreadsheet mistakes and their resulting consequences. 3. Uncategorized Transactions Keeping accurate records of financial transactions is essential for any business to succeed. However, categorizing these transactions systematically can be a challenge. A proper categorization system ensures that your bookkeeping is error-free and that you can easily identify similar transactions using categories or memos. Invoices must be correctly linked to transactions, and it is crucial to ensure that all events associated with a transaction are accounted for separately. Let's take the example of a Cardano transaction, which can trigger multiple events, including a transfer of Cardano, a gas fee paid to execute the transaction, and a gain/loss associated with the transaction. By accurately categorizing and reporting any losses associated with these transactions, you may be eligible for a tax write-off, or even minimize your crypto taxes which could save you money. Therefore, it is essential to have a robust categorization system in place to keep track of your finances and to make informed decisions that can benefit your business in the long run. 4. Susceptible Security Crypto accounting is crucial for companies handling crypto assets, but it can be tricky to navigate. One of the biggest challenges is avoiding common mistakes that can compromise the security of sensitive information. Human error is one of the biggest culprits, as employees may inadvertently click on unfamiliar links or enter personal information into fake accounts. To prevent these types of mistakes, it's important to implement best practices such as ensuring employees are properly trained on security protocols and regularly reminding them to remain vigilant. Additionally, utilizing secure networks and limiting access to sensitive information can help reduce the risk of cybercrime. By avoiding these common mistakes, companies can better protect their crypto assets and ensure their accounting practices remain secure. 5. Bad Calculations Based on Inaccurate Exchange Fees Crypto accounting can be a challenging task due to the complexities of the technology and the lack of standardization across different exchanges. One common mistake is relying on information from one exchange to make calculations about another, which can quickly lead to errors and require significant effort to correct. Additionally, manually calculating exchange fees can result in mistakes, so it's recommended to use automated tools to keep track of fees and calculations. With the help of technology, such as automated software, crypto accounting can be made more efficient and accurate. It's important to exercise caution and remain vigilant to avoid making mistakes in crypto accounting and maintain accurate records. Final Thoughts Crypto accounting can be a challenging task due to the unique characteristics of crypto, such as its cryptographic and anonymized nature. Even experts in traditional accounting may make basic mistakes when dealing with crypto accounting, especially when trying to navigate the additional complexities of crypto. The lack of established crypto accounting standards adds to the challenge as well. To ensure accuracy and efficiency in crypto accounting, it's important to exercise extreme caution and use specialized crypto accounting software that can help streamline the process. With the help of accounting software, companies can avoid common mistakes and keep their books organized and accurate. Read Also: How Blockchain Infrastructure Is Revolutionizing Businesses What You Need To Know About Software Testing In Blockchain ACTC Stock – Present Price, Forecast, Statistics – Should You Invest In It In 2022?

Mar 23, 2023

Is FLNT Stock A Good Bid To Purchase? Everything You Should Know

Are you planning to buy the flnt Stock? If yes, you must know some of the crucial facts that can help you earn more returns from your investment. Before you invest in Flnt Stock, you must know about the company’s background to make a better investment decision. Well-informed decisions can help you to earn more from your investments. Fluent stock prices have been rising for the past few months and are expected to grow further in the upcoming fiscal year. Work out the plans that can help you to make better investment decisions. Brief History On Fluent Inc Fluent Inc is one of the most renowned digital marketing Advertising agencies in the USA. It was founded by Matt Conlin and Ryan Schulke in 2010 with a fiery ambition to become the most successful digital marketing company globally. Fluent Stock prices are now growing in the market at a rapid pace. Smarter technology can make things easier for you to grow and evolve faster. Now, before you make your investments in any company, you must know about the financial strength of this company with all the detailed records with it. They are now partnering with the 500+ clients with fortune 500 + brands. Some Of The Core Services That FlNT Inc Provides Are As Follows:- It specializes in making consumer engagement for a longer duration. Ensures better data collection for better market mapping. Increases the chances of customer acquisition with the help of innovative digital marketing techniques to develop your brand image. It serves the customers in the USA for better market acquisition. Reasons To Invest In Fluent Stock There are several reasons to invest in Fluent Stocks. You will get the complete details of it if you read my entire article about the viability of making investments in Fluent stock. Some of the core reasons are as follows:- 1. Better ROI Expected In The Upcoming Years According to the stock market experts, a better ROI is expected from the Flnt Stock in the upcoming years. The Fluent Turns in a good Q3 which beats more revenue and non-GAAP earnings. After the Post Pandemic, the share prices of the flnt stock have risen to a great extent. The inclination of people towards digital technologies has created a wide variety of demands for digital products in the market. As a result, the flnt stock forecast is quite bright in the upcoming years. The year-on-year growth margin of the Flnt stocks is 21%, and it is expected to grow further in the future. The growth rate of this company is 167% which is far more than expected. 2. Strong Monetization Of Platforms The Flnt Stock prices are experiencing 21% growth in 2021 and year-on-year. It is expected to grow further with the growing acceptance of digital products. Although the company has faced a tough quarter in the previous year, the demand for the digital development of Flint stock prices is increasing upward. Flint Stock prices will encounter a decisive breakthrough. The post-breakthrough and consolidation pattern suggests a bullish trend in the stock market. Work out your plans that can work well in your favor. The valuation of the stock will continue to rise in the upcoming years. 3. Bullish Pattern Of Stock Markets The Fluent Stock prices are now experiencing a bullish trend in the stock market. With the advent of digital technology, the demand for digital products and E-commerce services has increased in the stock market. The stocks of this company have experienced a vital breakthrough over the past few years. First, you have to understand the facts that can help you achieve your goals in the best possible manner. Then, work out the plans that can help you achieve your goals in a better way. Finally, it suggests more bullish action take place. 4. Digital Transformation Increasing The Demand For Flnt Stocks With the advent of the digital transformation, there has been a considerable increase in the Flnt stock prices. People are more interested in investing more time and money in digital platforms than offline platforms. The Fluent Stock Forecast in 2025 is quite commendable in the years to come. The main reason behind it is that the revenue growth of this company is expected to grow by 167%. In addition, the company has achieved improved financial performance over the past few years. Due to its high-end digital products, it has grown its revenue by 15% CAGR. So work out the plans that can help you achieve your goals in the best possible manner. 5. Risks And Uncertainties Are Low The chances of the risk and uncertainties are pretty less in the case of the FLNT stocks. Let's understand the facts before making your investments in any stocks. You have to understand the world market economics before making your investments in stocks. You must know the Flnt Stock news before you make your investments. So make a proper investment in the stocks before making your grey choices. Do not mess while you want to develop your earning potential by investing in stocks. 6. Ensures Better Return From Your Investments Fluent Inc is a digital marketing agency, and the chances of the growth potential of this company are very high. If you have invested in the Stock flnt then you have made the right choice at your end. In a world where the chances of digital transformation have increased a lot here investing your money in the stocks of a digital marketing agency will not be a bad idea. You have the scope to earn more in a short period with maximum output. FLNT Stock Price News 2021-2022 Experts believe that FLNT stock will experience an incredible month of December in 2021. It will show stock breaking out of a 52-week high. The stock prices are pretty volatile and appear more stable consolidation pattern. It will reflect more bullish action in the years to come. Stay tuned with my next article to get more exciting news on the Fluent stock prices. FLNT stock can help you to achieve your more ROI in 2022 as the price index is showing upward trend. Final Take Away Experts think that the flnt stock prices will rise beyond the limits in the upcoming fiscal quarter. Therefore, it can help your business to grow further at a faster pace in a short period. Work out the plans that can help you to achieve your goals in the best possible ways. It is one of the best companies to increase the chances of your stock trading business prospects for the future. Frequently Asked Questions(FAQs) 1. What Does Fluent Inc Do? It provides advertising and marketing services to its clients all over the world. It is specialized in digital consumer engagement for acquisition, targeting, data collection, and other related solutions. 2. When Was This Company Founded? Fluent was founded in 2010. It has now become the most successful advertising agency in all possible manner. Work out the plans that can have a long-term impact on your investment. 3. How Many Employees Does Fluent Have? It has currently, 225 total employees and $310.72 million USD total networth from where you can earn the maximum revenue. Work out the plans that can help you to earn more from it. 4. Who Owns The Fluent Dispensary? Consortium owns the fluent dispensary for their business. Work out the best strategy that can help you to achieve your goals. Read Also: Why Create A Powerful Business Continuity Plan? How To Transfer Stocks From Robinhood To Webull? Is Nykaa Going To Dominate The Market With Their Recent Launch?

Dec 11, 2021

Stakeholder Vs Shareholder: Differences, Functions, Importance, And More

Stakeholder vs shareholder: What is the difference? - You will come across both these terms in the world of investing. There are stakeholders and shareholders in a corporation. While their names might look similar, their functions within a company are not. All shareholders of a company are its stakeholders, while all stakeholders are not necessarily shareholders. Shareholders own stock, while all stakeholders do not own stock. In this article, you will learn about the differences between shareholders and stakeholders. However, before that, we will give you a general overview of both these terms and their significance in the context of investing. Apart from that, we will also discuss the importance of both these roles in a business, as well as the major functions that these roles require. Hence, to learn more, read on through to the end of the article. Stakeholder Vs Shareholder: A General Overview According to Investopedia, “A stakeholder is a party that has an interest in a company and can either affect or be affected by the business. The primary stakeholders in a typical corporation are its investors, employees, customers, and suppliers. However, with the increasing attention on corporate social responsibility, the concept has been extended to include communities, governments, and trade associations.” In general, stakeholders have a vested interest in a company’s performance. Stakeholders can affect or can be affected by the performance of a corporation. Stakeholders include investors, shareholders, employees, suppliers, customers, governments, trade associations, or communities. Hence, you can see that the stakeholders of a business can be both inside and outside of the organization. On the other hand, according to Squareup.com, “The dictionary definition of a shareholder, also known as a stockholder, is a person who holds at least one share in a company. They’re not the same as a stakeholder though – this is someone who has an interest but doesn’t necessarily hold shares. Being a shareholder confers certain rights and responsibilities such as voting rights and the right to receive dividends if the company makes a profit.” You can see from the aforementioned definition that a shareholder owns a part of a public company through shares of stock. A shareholder is a stakeholder, but a stakeholder is not always a shareholder. A shareholder is not part of the day-to-day operations of the business, as these functions are the responsibilities of the directors, management, and employees of the company. [N.B.: If a shareholder owns more than 50% of the stock of a corporation, then he is a majority shareholder. However, if the shareholder owns less than 50% of the stock of a corporation, he becomes a minority shareholder.] The Importance And Functions Of Stakeholders According to the Corporate Finance Institute, “A stakeholder is a party that has an interest in the company’s success or failure. A stakeholder can affect or be affected by the company’s policies and objectives. Stakeholders can either be internal or external. Internal stakeholders have a direct relationship with the company either through employment, ownership, or investment.” Stakeholders are basically those people who affect the company, or the company affects them. These people have a “stake” in the company’s success and failure. A shareholder can also be a stakeholder. However, a stakeholder is not always a shareholder. Here are some common examples of stakeholders of a company: ● The employees of the company ● Customers of the company that rely on the company’s ability to provide services ● Shareholders of the company. ● Suppliers and vendors of the company ● Community members who feel the impact of the company’s decisions ● Other promotional activities of the company, including partners in events, promotions, etc. The Importance And Functions Of Shareholders A shareholder is an institution, company, or individual that owns at least one share of the company. The company’s growth offers profit to the shareholders. Hence, shareholders are also stakeholders by default. The success of the business interests shareholders since they want to receive the greatest possible return on their investment. When the company performs well, the stock prices and dividends go up, which increases the value of the shareholder’s stocks. Shareholders also have the right to exercise a vote and affect the company’s management. These people are the company’s owners and are not liable for the debts of the company, as the company is a corporation. To have shareholders, a company or a business venture needs to become a corporation by filing articles of incorporation. Stakeholder Vs Shareholder: Major Differences The following are some of the key differences between a stakeholder and a shareholder: StakeholderShareholderThey are bound to the company for the long term and are interested in the actions and success of the company.They might not have a long-term need for the company.A stakeholder can have an ownership stake in the company.Shareholders can own a part of the company by purchasing stock.The day-to-day decisions of the company impact stakeholders. The actions of the stakeholders also impact the company’s growth.The day-to-day decisions of the company might not impact shareholders. Depending on their relationship with the company, shareholders and stakeholders might have competing interests. For example, shareholders might want a company to maximize its profits by keeping its wages low or using less expensive manufacturing processes. However, this is not good news for employees and the customers of the company. Both stakeholders and shareholders are important for a corporation. However, if business ownership and management are ethical, they understand that a shareholder’s short-term profit goals might not be a good thing for the company in the long run. Hence, they resort to the Stakeholder Theory. Wrapping Stakeholder vs shareholder - Hope this article was helpful to make you understand the differences between these two terms. You can see from the article that all shareholders of a company are stakeholders. However, all stakeholders are not necessarily shareholders. When a company is public, shareholders own stock of the company through shares. On the other hand, a stakeholder just wants to see the company grow and prosper in the market. Other than stock performance, a stakeholder can also have other reasons to see the company grow. In most cases, stakeholders are often part of a company for a long time. Do you have more points to add? Share them with us in the comments below. #Disclaimer: The information provided on this blog is for educational and informational purposes only and should not be construed as financial advice. I am not a licensed financial advisor. Any investment decision you make is at your own risk, and you should consult with a qualified financial advisor before making any investment decisions. This site may contain affiliate links, and I may earn a commission at no additional cost to you. Get High With Business Articles Let's Check Out!! What Is a Bear Hug? Let’s Discuss The Benefits Capital Expenditures – Definition, Types, Examples, And More What Is An Endowment? – Working, Purpose, Types, And More

Nov 27, 2023