Matrix Organizational Structure – What Are Its Pros And Cons?

In a matrix organizational structure, the teams within an organization try to bring different roles within the team together. Doing so, unlike a traditional hierarchical structure, they develop a grid-like reporting structure. Basically, the organization combines two or more structures from within. Here, both the traditional hierarchy of management as well as inter-department management is combined.

In this article, you will learn in general about a matrix organizational structure and how it works within an organization. In addition to this, we will also discuss the major pros and cons of this organizational structure.

Apart from that, we will also discuss the major roles within a matrix organizational structure. Hence, to learn more about such an organizational structure, read through to the end of the article.

What Is A Matrix Organizational Structure?

The matrix organizational structure basically combines two or more kinds of organizational structure. For example, let’s say you combine project management and functional management.

According to Indeed.com,

“Additionally, the matrix structure is composed of both a traditional hierarchy of management, where employees are managed by a functional manager, as well as additional project managers who can manage employees across different departments. These two or more managerial systems intersect on a grid or matrix.”

In this organizational structure, different management styles are used – where the functional management as well as the divisional management are combined. Here, functional management consists of the traditional hierarchical structure based on the job function and the organization’s department. On the other hand, a divisional manager is the one who presides over the cross-functional team, which consists of representatives of both teams.

An organization with a matrix structure has team members reporting to different managers. There might be a hierarchical manager while the team members may also have to report to their project manager.

This type of structuring is important for companies trying to create new products without the hassle of realigning their teams.

The matrix organizational structure combines the functional and the divisional managers. This helps the work processes to be done faster.

According to the Wall Street Mojo website,

“In a matrix structure, team members provide information to a project leader and their department head. This management structure might assist businesses in developing new goods and services without reorganizing teams.”

The matrix organizational structure was started in the aerospace industry. This was the time when many firms wanted to get into a contract with US Government employees. They needed to create certain charts that show the structure of the project management team.

How Does A Matrix Organizational Structure Work?

This structure is best understood with the help of an example. According to ChartHop.com,

“At the simplest level, an example of an organization using a matrix structure would be one that has set functional teams (e.g. Marketing, Sales, Customer Success) as well as more divisional teams with members from different functional areas that work together on specific initiatives.”

A common example of a matric organizational structure is Nike. The company has teams that operate the functional management like merchandising and HR, as well as divisional teams that operate based on location, demographics, and product.

Companies and their employees can get a lot of advantages with the matrix structure, especially with the ways that they work within the organization. The teams can share knowledge with each other and can make more informed decisions. Apart from that, the best thing that they will have is better morale within themselves.

However, there are problems that you can find inside a matrix organizational structure, too. Some of them include conflict, slowdown of processes, lack of clarity, and more.

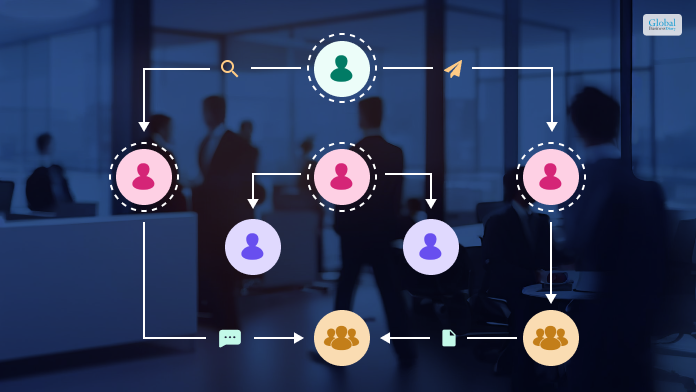

Here’s how a Matrix organizational structure works –

- The employees report to two managers simultaneously. A functional manager is responsible for their overall role in the department.

- Their project manager, on the other hand, is responsible for the overall role in the department.

- The project manager is also responsible for a specific role or a project.

- When team members report to two different managers, the organization automatically breaks down its structure in a different style.

What Are The Pros Of A Matrix Organizational Structure?

There are different pros and cons of using Matrix organizational structure. It offers flexibility, adaptability, and advantages when matching changing customer needs.

This type of organizational structure helps maintain work efficiency and matches market conditions and strategic goals. By creating cross-functional teams working on different projects, these companies can use the Matrix organizational structure to their advantage.

According to LinkedIn.com,

“One of the main advantages of a matrix structure is that it allows for more flexibility and adaptability to changing customer needs, market conditions, and strategic goals. By creating cross-functional teams that work on specific projects or tasks, a matrix structure can leverage the diverse skills, knowledge, and perspectives of employees from different departments, and foster innovation and creativity.”

The intricacy of the matrix organizational structure is one of its main characteristics. You can see from the above sections that the employees are answerable to two managers – functional and project managers. This is because the allocation of resources is in such a way that the human resources are utilized at their highest.

The following are some of the major pros of a matrix organizational structure:

- The departments are able to coordinate better, as the structure brings highly competent team members from different departments to one place.

- One of the major characteristics of a matrix organizational structure is that it combines the operational and project management frameworks.

- The communication between two or more departments gets better with the implementation of the matrix organizational structure.

What Are The Cons Of A Matrix Organizational Structure?

Like most management structures, the matrix organizational structure also has its drawbacks. Here are some of the cons of the matrix organizational structure that you will need to be aware of:

- There is a continuous need for clarification for the managers regarding their positions, and there are ambiguities in some cases. Hence, there is always a need to define the power dynamics between managers.

- Apart from the managers, the teams also need clarification regarding their roles in the structure. The individual team members should have a good idea of what their role is at the functional level and what their role is at the project level. This helps in reducing miscommunication between the members.

- In some cases, due to the involvement of different teams and departments, the decision-making processes can get a bit longer. Apart from that, time is taken since decisions regarding processes need to be made through two different managers. Hence, processes such as quality assurance slow down due to the presence of multiple supervisors.

Read More: Entrepreneur : Who Coined The Term ‘Entrepreneur’?

Tips: Use Matrix Organizational Structure to its Fullest Potential

If you are planning to use the Matrix organizational structure, it’s best to start by outlining different roles within the project. Here are several tips to try when utilizing Matrix organization structure in an organization to its fullest potential.

Manage Expectations

While outlining the responsibilities of different roles within the project, the best approach would be to understand the expectations of each manager. A project manager might be expecting the performance of the overall project.

On the other hand, the marketing manager might only be concerned with campaign performance. It’s important to manage the expectations of different managers and work accordingly.

Keep People Accountable for Their Work

The best way to ensure efficient project delivery; it’s important to make people accountable for their work. Workplaces with systems in place to increase engagement in their work can boost accountability. Companies can have a weekly report template for the employees accountable for different tasks.

Communication Between Employees and Managers

It’s important to keep communication seamless and transparent between employees and managers. There can be a weekly chart outlining the completion of tasks. In addition, the managers should also provide employees with feedback. Companies can do it in person or through chat and communication apps used in the organization.

Inter-Department Relationships

Projects requiring co-dependencies from different departments often face operational hurdles. It can happen due to a lack of collaboration and inter-team communication. However, it’s important to deepen interdepartmental relationships to avoid misunderstanding during collaboration.

Wrapping Up

Hope this article was helpful for you in getting a better idea of what a matrix organizational structure is. This structure is best suited for large organizations or organizations that deal with multiple projects. Due to the multiple needs of the organization, the managers can shuffle teams and bring personnel from different departments to work together.

The matrix organizational structure helps in better coordination between departments and ensures a better quality of products and services. Do you have anything to add regarding this type of organizational structure? Share your thoughts and ideas with us in the comments section below.

Read More:

Tags:

Recent

Due Diligence Decoded: Why Careful Evaluation Still Wins in Business

Jul 11, 2026

How Hydraulic System Design Impacts Equipment Performance

Jul 01, 2026

Startup Bootstrapped Fundraising Strategy: A Guide for SaaS and Tech Startups

Jun 21, 2026

Where Distributors Lose Profit Without Realizing It

Jun 20, 2026

Related Articles

How To Build An Ecommerce Website To Boost Your Business

Making new Ecommerce websites are accessible nowadays. Those who have a business based on online media have these Ecommerce websites. It is just like a book of business. You have bought a pair of shoes, perfumes, dresses, etc. They have sent your ordered items to your doorsteps. It seems easy when you are looking at things from the view of a customer. But you will feel challenged when you feel you are the business owner, and you have to send the product to the customers’ doorsteps. However, serial entrepreneurs are doing the most demanding things and maintaining ecommerce websites. Benefits Of Using Ecommerce Websites Serial entrepreneurs always use ecommerce websites to boost their business. However, if you are also thinking of opening a new ecommerce website, you will get a series of benefits. First, ecommerce websites have an option to earn a considerable profit. Now make a website and get the benefits. Now, we will tell you the advantages of opening Ecommerce websites. Go through the book of business and learn the factors. 1. Fast Buy As the owner of the ecommerce website, make your customers satisfied. So, it is easy for them to purchase products in some time. It takes only a minute to buy the product. For example, suppose one of your customers finds a particular product if the person gets it by search and can order it in a single minute. In this way, you can get benefits from using Ecommerce websites. 2. Cost Reduction Process It is a book of business where you have to pay less. For example, if you are selling products in your store, spend money on decoration, electricity, lights, and all. But in the online store, you don’t have to pay for other things. You can follow the serial entrepreneurs. The process is simple and also easy to understand. You don’t have to think of negotiation. If you give a price, interested customers will buy it with that price. But sometimes in the shops, people want you to reduce the cost of the product. However, serial entrepreneurs use Ecommerce websites. Read More: Top 7 Part-Time Work From Home Jobs In 2021 3. Multi Selling Products Using the ecommerce website, you will have time to sell multi-products. For example, you can sell grocery items and also clothing items. The all-in-one facility is excellent and also appreciable. You can open a website and boost your business. Go through the book of business. You may need a designer, but you also do not have to pay extra for creating if you know how to design like it. You will get the best profit through the company. Therefore, make a new website and operate it. How To Build An Ecommerce Site Creating an Ecommerce website is a time-consuming process that may take almost a year to decorate appropriately. However, if you are going to make an ecommerce website for the first time, you may feel bored. Thus, you need to have patience for opening a website and also can see the book of business. Don’t lose patience. Wait for the day of getting a high profit. So, we will now see how to make an Ecommerce website. Design the website in the best way that you can. It is the best time to create an ecommerce website. Serial entrepreneurs always follow these steps. 1. Legal Domain Name When you make a perfect plan for creating an Ecommerce website, choose the niche that you will select. Then, when you locate the place, you will work. After that, you also need to have a name that will perfectly match your business content. Famous serial entrepreneurs always place a proper name as the domain name. With this name, everyone will search and will purchase. You may have to buy the domain name the first time. The official website name is always a registered process. However, pay for that. 2. Legal EIN Number For E-commerce Business When you pay for the domain name, ask to get the EIN. It is the process of Ecommerce website business. If you get a number, that means your business is legal. EIN is the employer identification number. Based on that identity number, pay tax to the online service authority. Visit the book of business and get the details there. The process is the same as the shops. Many websites do not have an EIN. That means the business that the owner is running is illegal. Anytime the owner can get rid of accessing the account. However, you must think of doing a permanent business. Therefore, you must apply for an EIN. 3. Business Permission And License To run a legal e-commerce business, get the license to tell you to have a legal E-commerce business. Then, you need to get permission from the authorities. So, apply for obtaining a permit and go to the next steps. However, wait for the response of the authority and then proceed. Then, in the book of business, it is appropriately mentioned. 4. Designing Designing is the last significant part of creating an Ecommerce website for running a business. When you get an echo from the authority, that means they want you to do the business. However, you go gentle and choose a platform through this, and you will operate the site. For designing, you may need to have a designer. Therefore, select a person who will design your website as you will want. Successful serial entrepreneurs always follow the steps and then open websites and earn money online. Read More: How To Endorse A Check- Step By Step Guide For The Beginners In 2021 The Last Lines These are the steps that serial entrepreneurs have to follow to boost their business through E-commerce. However, all the doubts that you could have been cleared. If you still have doubts, then watch a video and learn in more detail. But before going through the steps, research the market. In that, you will learn what the best niche is in demand. You can go with it, therefore. However, don’t waste your time and seriously have a look at the book of business. It is the best time for you, so go gentle towards your goal. Read More: What Is Network Marketing And How To Do It In 2021 How To Open A Small Restaurant With Less Budget?

Jul 15, 2021

Disaster Recovery Vs Business Continuity – What Are The Differences?

Disaster recovery vs business continuity: Which one is important? - The short answer is “Both.” It depends on the situation you are dealing with. Most companies operate by assuming that their workplaces will maintain their consistent state with changing times. Hence, they try to find comfort in daily routines and rhythm of work. However, there are certain events when a business might face disruption. Hence, businesses need to have a disaster recovery plan and a business continuity plan in place to ensure that the business recovers faster when it comes across a negative situation. In this article, you will learn about disaster recovery and business continuity in general. However, the focus of the article will be on the differences between the two. Apart from those differences, we will also discuss the major similarities between them as well. In addition to this, we will, in brief, share with you how each of these works and how to implement them. Hence, to learn more, read on through to the end of the article. Disaster Recovery Vs Business Continuity – What Are They? If you want to prepare for disruptions in business, you will need to create various strategies and plans, following which you will be able to ensure that the core business functions are intact. This can help the business to come back faster from the uncertain negative consequences it just faced. What Is Disaster Recovery? Amazon Web Services defines disaster recovery as such - “Disaster recovery is the process by which an organization anticipates and addresses technology-related disasters. The process of preparing for and recovering from any event that prevents a workload or system from fulfilling its business objectives in its primary deployed location, such as power outages, natural events, or security issues.” To measure the targets of disaster recovery, two factors are taken - Recovery Point Objectives (RPO) and Recovery Time Objectives (RTO). The failures for which companies make disaster recovery plans are mostly larger-scale disaster events. The plan includes various procedures and policies for the company so that it can recover quickly from the disaster by following them. What Is Business Continuity? According to the Business Continuity Institute, “Business continuity is about having a plan to deal with difficult situations so your organization can continue to function with as little disruption as possible. Whether it’s a business, public sector organization, or charity, you need to know how you can keep going under any circumstances.” You will need a business continuity plan, too, in case of a disaster situation. However, the continuity plan is to deal with the disaster situation so that the organization is able to continue its functioning with little to no disruption. However, you will need to understand here that a business continuity plan does not work at times of a large program or a disaster, which affects the company a lot. It also does not work when a large number of people are associated with a single plan. Hence, many big companies make business continuity plans for each of their departments. This makes each department implement the plan as per its needs. Disaster Recovery Vs Business Continuity – Major Differences Disaster RecoveryBusiness ContinuityFocuses on restoring access to data and IT infrastructure after the impact of the disaster.Involves the creation of additional safety measures for employees. Here, the company creates safety drills and stays prepared with emergency supplies.Disaster recovery is created for disruptions of higher levels, especially when many personnel are involved.Involves the limitation of abnormal or inefficient functioning of the system.Ensures that the organization can return to full functionality following a disaster situation.Focuses on keeping the business operations running even during disasters.It consists of plans and procedures on how to continue business operations. The plans also include who should do what at the time of any disruption.Business continuity planning does not work in situations when many people are involved.Involves limitation of operational downtime.Ensures that all the communication methods of the organization continue working during a crisis. You can see from this table that both disaster recovery and business continuity are complementary to each other. Businesses need to combine both plans to ensure they are prepared for disastrous events. Disaster Recovery Vs Business Continuity – Major Similarities The following are some of the major similarities that you will find between disaster recovery and business continuity: Both are proactive strategies that enable a business to stay prepared for uncertain and disastrous events. Both plans allow the company to minimize the effects of the disaster before it actually occurs and affects the business. Both work quite well in situations of natural and man-made disasters. However, the result of their implementation depends on the situation. Professionals need to review both plans on a regular basis, and some of them need revision with the evolving situation of the organization. How Do Disaster Recovery And Business Continuity Work? According to the University of Central Florida, “Having business continuity and disaster recovery plans in place can help companies minimize the consequences of a catastrophic event. They can also provide peace of mind; employees and business owners alike may feel more comfortable in a work setting where there are clear policies for how to respond to disasters.” To implement these plans for the recovery of the business, the organization needs to create/hire crisis management professionals. These professionals will be responsible for developing and implementing such plans. Apart from that, they are also responsible for evaluating and revising them as per needs and training the employees of the organization to stay prepared. Final Thought Disaster recovery vs business continuity: Hope this article was helpful for you in getting a better idea of both of these terms and how they operate in the organizational setting. Disaster recovery works in situations when the disruption is big and many people are involved. On the other hand, business continuity planning is to ensure business operations are continued in disruptions. Do you have any more recommendations regarding when and how to implement a business continuity plan and a disaster recovery plan? Share your thoughts and ideas with us in the comments section below. Read More: Entrepreneur : Who Coined The Term ‘Entrepreneur’? Intrapreneurship – Definition, Importance, Duties, And Responsibilities What Is a Franchise, And How Does It Work? – Examples, Benefits & More

Sep 11, 2023

Wholesale Hair Extensions: The Backbone Of Your Beauty Business

In beauty and fashion, hair extensions have emerged as a game-changer. They offer a quick and convenient way for people to transform their looks, experiment with different hairstyles, and boost their confidence. For entrepreneurs in the beauty industry, wholesale hair extensions have become the backbone of their business. This article will explore why wholesale artificial hair is essential for beauty businesses and how they can drive success. The Rising Demand For Hair Extensions The demand for hair extensions has been on a constant rise in recent years. Women and men of all ages are turning to hair extensions to achieve longer, thicker, and more luxurious hair. This surge in demand can be attributed to several factors, including the influence of celebrity endorsements, social media, and the desire for a quick hair makeover. Variety And Versatility One of the key advantages of hair extensions at wholesale is the incredible variety and versatility they offer. Beauty entrepreneurs can source extensions in various textures, lengths, and colors to cater to a wide range of client preferences. Wholesalers provide an extensive selection, whether it's straight, curly, wavy, or a specific shade of hair. Quality Assurance When purchasing hair extensions in bulk, beauty businesses can ensure quality control. Reputable wholesale suppliers often provide high-quality, ethically sourced hair that undergoes rigorous testing. This guarantees that the extensions will meet the expectations of your clients, helping you build trust and a loyal customer base. Cost Efficiency Buying hair extensions at wholesale prices allows beauty entrepreneurs to maximize their profit margins. Purchasing in bulk lowers the cost per unit significantly, enabling businesses to offer competitive prices while still enjoying healthy profits. This cost efficiency is a vital factor in the success of any beauty business. Meeting Client Demand Wholesale artificial hair enables beauty businesses to meet the growing demand for hair enhancement services. Whether you run a salon, a retail store, or an online shop, having a steady supply of high-quality extensions is essential to satisfy your clients' needs. Being well-stocked ensures that you can handle both regular appointments and last-minute requests. Building A Brand Identity In the beauty industry, having a unique brand identity is crucial for standing out in a competitive market. Hair extensions at wholesale provide an opportunity to create a signature line of products under your brand. You can customize the packaging, choose specific hair types, and even offer exclusive colors and textures that align with your brand's image. Customer Loyalty Consistency is key to building customer loyalty. Wholesale artificial hair extensions enable you to maintain a consistent supply of products, ensuring that your clients can rely on your services whenever needed. This reliability fosters trust and encourages repeat business, which is essential for the long-term success of your beauty venture. Diversifying Revenue Streams For beauty entrepreneurs looking to diversify their revenue streams, wholesale hair extensions offer an attractive option. You can sell extensions alongside your salon services or retail them through your online store. This diversification boosts your income and makes your business more resilient to market fluctuations. Educational Resources Many wholesale suppliers offer educational resources and support to their clients. This can include training on installing and maintaining hair extensions, marketing assistance, and access to product knowledge. Such resources are invaluable for beauty businesses, especially those looking to expand into the hair extension market. In conclusion, wholesale hair extensions have emerged as the backbone of the beauty industry. They offer beauty entrepreneurs a range of benefits, from cost efficiency and quality assurance to brand identity and marketing opportunities. By incorporating wholesale artificial hair extensions into your beauty business, you can meet the rising demand for hair enhancement services, diversify your revenue streams, and build customer loyalty. Ultimately, these extensions can be the key to the success and growth of your beauty venture in a competitive market. Read Also: why create a powerful business continuity plan? what is network marketing and how to do it in 2021 how to start a business in 2021 – best business strategies

Oct 11, 2023

12 Passive Income Ideas To Get You Rich In 2023

Some of the major passive income ideas include investing, side hustle, creative work, and more. A passive income is an income that you do not earn, and you generate differently. Passive income puts money in your pocket even when you are not working. You will not need to do active work while you are income passively, unlike the case where you are a traditional employee or a full-time entrepreneur. In this article, we will discuss different ways to make passive income in 2023 as we give you the twelve best passive income ideas. Along with the passive income ideas, we will also give you a brief explanation of how you can implement the idea for yourself. Hence, to learn about these extra income ideas, read on through to the end of the article. Passive Income In 2023 – A General Overview To earn passive income, you will not need to spend a lot of time, money, and resources. According to Forbes.com, “Passive income helps you earn a little extra. Every penny earned matters, and you can deploy the funds to build an emergency fund, start a systematic investment plan in mutual funds, etc.” In passive income, you can earn money by doing projects and making products with little work and essentially no maintenance. This is the money that you are earning from the assets that you control. However, you must note here that it requires some effort at the start, but as you progress, you will have little to no effort. Furthermore, with progress, you will not need to invest a lot of your time. According to an article in Time Magazine, "The cash stream from sources of passive income requires some upfront work, but once established, takes little to no time to maintain. While it can take some time to see the fruits of your labor pay off with passive income, earning money without regular work is possible.” Passive income helps to raise your income level by providing you with extra income options. Although there is a small investment in some cases, it is only one-time. You will not need to participate and devote a dedicated number of hours to the work. However, there is a need for maintenance in passive income, which is not a requirement in any regular income. On a side note, check out some of the best lead management software systems available in 2023 if you are into marketing and sales. The Best Passive Income Ideas For You In 2023 Here are some of the best passive income strategies that you can tryout if you are looking to start with a passive income in 2023: 1. Dropshipping Business Although one requires a little cash, you don't need a lot to start a dropshipping business. Here, to sell a product to a particular customer, you do not need to manage products physically. 2. Blogging It is the most tried and tested passive income that many people tried and got successful. However, it has a lot of competition. So, if you want success, try to be unique and simple. 3. Printing On-Demand If you are creative or understand designs, you can start an on-demand print store, as you can monetize your creativity by printing T-shirts, posters, backpacks, mugs, papers, and more. 4. Online Tutorial If you have knowledge of any subject or skill, you can start an online tutorial regarding the same. You can create video tutorials and create a package for learners to learn from. 5. Selling Digital Products To sell digital products, you will have to create your assets (digital products) once, and then you can sell the product to as many people as you want with your online business. 6. Dealing With Rental Property This is an ancient way of having a passive income. However, you will need to have the capital to buy properties that you will rent to others. The income level is also high. 7. Investment In Businesses And Stocks The most popular source of passive income is investments in stocks and business-related investments. However, investing in stocks requires heavy speculation skills, which you will need to develop. Off-topic: Are you looking to start a startup? Once you open a startup, you will need to consider having your startup insured. To check the best startup insurance options, click on the given link. 8. Affiliate Marketing According to Shopify.com, “a great source of passive income because you earn a commission whenever someone uses your referral link to buy the recommended product or service.” All you need is to recommend the product. 9. Social Media Influencer If you are good at social media, and have the confidence to influence a many audiences with your social media content, then this idea can do wonders for you. 10. Starting A YouTube Channel You can start a YouTube channel about anything that you know. Some of the best ideas, in this case, include – tech reviews, gaming videos, entertainment, tutorials, and many more. 11. Create A Digital Guide A digital guide can be about anything, from travel guides, tutorials, University suggestions, and more. You can create a digital guide once, and you can sell it to as many people as you like. 12. Design And Sell Websites If you are a website designer, then you can sell your designs to companies to earn. Furthermore, if you can code, then you can make full-working websites and sell them to customers. Summing Up One of the most underrated things about passive income is that it is the result of hard work and repeatedly working on the same thing. The more you work, the better returns it will offer you in the future. Once you add one of these passive incomes to your life, you will have better flexibility in work, more freedom, and better earning. Choose the one that suits your character and skills, and work on it consistently, to ensure future results. Do you have any other passive income ideas that you think can work amazingly in 2023? Share some of them with us in the comments section below.

Jul 11, 2023