Navi: Information, Eligibility Criteria, Interest Rates, Review & More

You can get Navi personal loan with minimal documentation. Furthermore, if your documentation and your Navi loan application are cleared, you will be able to get the loan even within a few minutes. You can get fast personal loans at 9.9% per annum onwards. This digital instant loan app of Navi gives you fast loans, and also at zero processing fees.

In this article, you will mainly learn about some of the essential features of Navi personal loans. Apart from that, you will also learn about the Navi personal loan interest rates, as well as eligibility criteria, documentation required, and more. Hence, to learn more about the Navi personal loans, read on through to the end of the article.

Navi Personal Loans – A Brief Overview

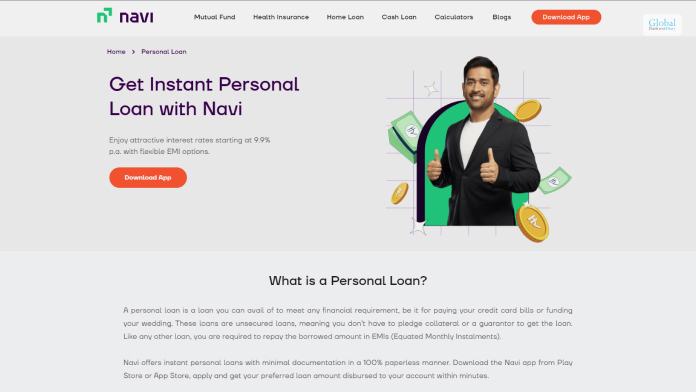

A personal loan is something that you need to meet any financial requirement if you somehow lack finances at the moment. The loan might be needed to pay your credit card bills, wedding, health expenses, buy something important, and many more reasons. Hence, you need a financial company like Navi to offer you personal loans. Navi is just like personal loan-offering companies like India Lends, CASHe, and others.

Navi, also known as Navi Finserv, offers personal loans up to ₹20 lakhs (INR). The borrower of the loan can get the amount through the Navi app, and also with zero processing fees. Apart from that, the loans are fully paperless and are available after you share your PAN and Aadhar number. Once your documents are verified, and your loan application is cleared, then you can get the loan in as fast as ten minutes.

According to the official website of Navi,

“Navi offers instant personal loans with minimal documentation in a 100% paperless manner. Download the Navi app from Play Store or App Store, apply and get your preferred loan amount disbursed to your account within minutes.”

One of the best things about Navi personal loans is that you will have access to unsecured loans. This means you will not offer any collateral for the loan, nor do you need a guarantor for the loan. Like just any other personal loan option, you will only need to repay the amount you have borrowed in Equated Monthly Instalments or EMIs.

Furthermore, if you want to get returns by investing in mutual funds, you can do that by looking for Navi mutual fund or Navi nifty 50 index fund. In addition to that, there is also Navi health insurance, which you can buy to purchase health insurance plans.

Navi Loan Interest Rate, And Other Loan Highlights

The following are some of the highlights of Navi personal loans that you will need to know about:

| Navi Personal Loan Highlights | |

|---|---|

| Rate of Interest | 9.9% to 45% of the principal amount |

| Available Loan Amount | Loans of up to ₹ 20 lakhs are available |

| Tenure of the Loan | The loan is available for up to 6 years |

| Preclosure fees of the loan | There is no preclosure fee for Navi Loans. (There is no disclosed amount. Contact the lender of the loan to know more.) |

You can see from here that the minimum rate of interest for Navi personal loans is 9.9%. However, the rate of interest can rise to 45% based on a variety of factors. These include – monthly income, age, job profile, loan repayment history, credit score, and many more.

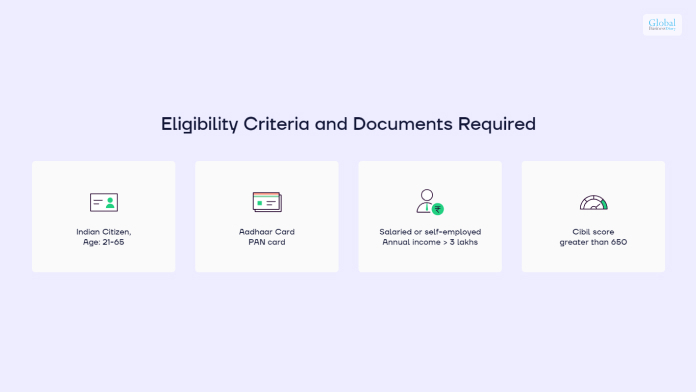

Navi Personal Loan Eligibility Criteria

The following are some of the essential eligibility criteria of the Navi personal loan that you need to clear if you want to avail of personal loans:

| Factors | Eligibility |

|---|---|

| Nationality | – Borrower must be a citizen of India |

| Occupation | It must be either of the two:- Salaried- Self-employed |

| Age | – The loan applicant must be aged between 18 to 65 years.- The minimum required age can be increased to 21, 23, or 25 years in special cases. |

| Credit Score | – To avail of the Navi personal loan, a borrower needs to have a minimum credit score of 650 (CIBIL score). |

| Documents Required | – PAN Card- Aadhar Card |

Navi Loan Minimum Salary

Every credit company has a base line salary criterion. But why?

This is mainly to ensure that you can pay back the loan you take.

How is it determined?

A threshold is considered. It is INR 15000 on most occasions. However, there are other factors that decide whether you will get a loan with INR 15000 salary.

Firstly, your creditworthiness matters. You are ineligible if you have an INR 15000 salary with a low credit score.

However, you can get a credit line from Navi if you have a minimum credit score of 650.

A person with credit score of 650 means two things:

- No or minimal credit repayment default cases

- Average credit worthiness, as evaluated by other credit companies earlier

The next threshold salary bar is INR 20000. It implies that your loan value will be greater as well.

However, the banks that grant INR 20000 as the threshold eligible salary for credit, will not consider INR 15000 as threshold.

For instance, IDFC First Bank gives loan against a minimum salary of INR 20000.

But there are no schemes that can get you a loan if you have INR 15000 salary.

Moreover, there are differences in credit worthiness of the two individuals. In simple terms:

- An individual with INR 15000 salary may get up to INR 1500000 as loan.

- An individual with INR 20000 salary may get up to INR 2500000 as loan.

Benefits of taking a navi loan minimum salary

The navi loan minimum salary is INR 15000. But it may be higher if your credit performance is not good. Ideally, you must have a credit score of 650 with a minimum salary of INR 15000.

If you wish to take loan against this threshold criteria, you may get the following benefits:

- No collateral against the credit line/loan that you get.

- The repayment tenure might span up to 5 years.

- You might have to pay slightly more interest, but you may get a favorable EMI breakdown.

- You can get your credit line from Navi, immediately approved.

- You can do KYC and documentation prior to approval online, in minutes.

- If your loan is around INR 15000, it will take almost no time to be disbursed.

- As there are no collaterals, there are no instances of validation, once KYC is done.

- You may get a small credit line against minimum salary, but you can pay back and get a higher credit line.

- No concealed charges are applicable, as you get to know the final repayment value, before you sign the disbursal letter.

Other miscellaneous eligibility criteria applicable

You must have a fixed salary from an acceptable source. However, you can be self-employed as well. For instance, you may run a coaching center. Mostly navi loan minimum salary comes with the criteria of 1-2 years of minimum work experience.

Lastly, navi loan minimum salary is INR 15000, only when you are 23 years of age at the least.

There are no hidden clauses. If you meet the two main criteria (min salary of 15000 and 650 credit score), you will get a loan easily.

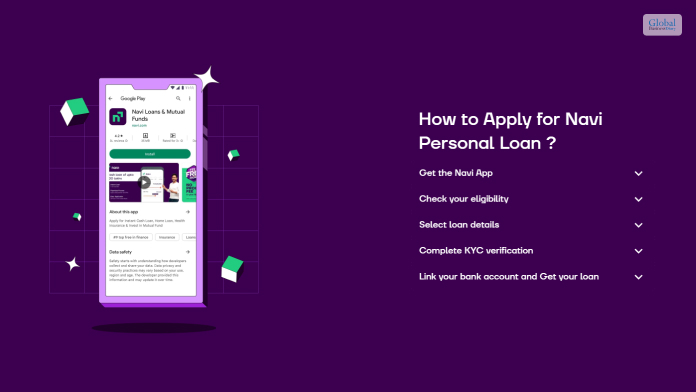

How To Apply For Navi Personal Loan? – Steps To Follow

Once you are okay with the essential features associated with Navi personal loans, you will need to apply for a personal loan from the Navi app. Here are the steps you need to follow to apply for a personal loan from Navi:

Step 1:

Go to Play Store or App Store, and download the Navi personal loan app. Install the app on your Android phone or iPhone.

Step 2:

Register your mobile number on the Navi server through your app.

Step 3:

Check the eligibility of the loan, and fill in your personal details through the app.

Step 4:

On the app, go to the next page, and select the loan amount and the EMI amount.

Step 5:

Once you have the amount, you need to complete the KYC process, where you need to produce your Aadhar and PAN numbers and upload a selfie of yourself.

Step 6:

Enter your bank account details which are needed for the transfer of money.

Step 7:

Apply for the loan. Once your loan is verified, you will get your loan fast. The money will be transferred to your amount within the time specified to you.

Is Navi Approved BY RBI?

Now many people ask whether Navi is approved by RBI or not. Then, in this case, the Navi official website claims,

“RBI does not approve digital lending apps. The Navi App is operated by Navi Technologies Limited. Navi Finserv Limited is an RBI registered Systemically Important Non-Deposit Taking NBFC (ND-SI) which lends through the Navi App. Navi Technologies is the digital lending partner of Navi Finserv.”

Frequently Asked Questions!!! (FAQ):

Ans: Navi offers personal loans for attractive interest rates that start from 9.9% with some flexible EMI options upto 72 months. You need to get through the right options that can assist you in attaining your requirements with complete ease.

Ans: NAVI loan is a legit application that offers you health insurance services as per your requirement. You have to get through the complete process that can make things easier for you to attain your requirements with complete clarity.

Ans: Yes!! Navi personal loan is approved by RBI. You have to get through the complete process that can make things easier and effective for your business in the correct order. You should follow the right process that can make things easier for you to get the loan on time.

Ans: If your age bracket is between 18-45 years then you are eligible for the Navi Loans. You have to get through the complete loan process can make things easier for you to get the loans on time. Try to figure out the reasons for getting or not getting the loans.

Ans: You need to be an Indian citizen within a period of 21-65 years. You cannot make your selection and choices in the incorrect end. You need to have 3 lakhs of money as your salary.

Summing Up

Hope this article was helpful for you in getting a comprehensive idea of what to expect from Navi personal loans. If you are looking for a quick personal loan, you can apply for one through the Navi app; however, as you have seen that the rate of interest can change as per the loan amount and the applicant’s details. Do you know of any other app that offers similar loan rates? Share your answers in the comments section below.

Read More:

Tags:

Recent

Corporate Software Inspector: The Simple Way to Keep Your Company Safe

Mar 02, 2026

Why Business Intelligence Exercises Are Important for Effective Data Analysis

Feb 22, 2026

The Hidden Cost of Dirty Curtains: More Than Just an Eyesore

Feb 20, 2026

Strategic M&A: Turning Opportunity Into Lasting Value

Jan 24, 2026

Related Articles

How To Choose The Right Stocks: Tips For New Investors

Fundamental and technical analysis are two common methods for identifying and picking stocks. Fundamental analysis examines a company's business and industry conditions to identify stocks with strong growth potential at a good price, typically used for longer-term trades. Technical analysis, on the other hand, identifies statistical patterns on stock charts to predict future price and volume moves, typically used for shorter-term trades. Beginners in the stock market can find it intimidating. However, understanding basic trading and understanding how to buy share online can make it easier. Various methods, like attending financial events or using online platforms, can help pick stocks. Therefore, investors with a long-term horizon have an advantage over Wall Street's short-term focus, making informed decisions. This article will help you with effective tips and strategies for selecting the best stocks. Tips To Choose The Right Stocks Here are some of the top tips that can help you pick the right stocks for your investment— 1. Finalize Your Goal Every investor comes with unique goals for their portfolios. However, most young investors aim to increase their portfolios over time. Older ones, on the other hand, focus on capital preservation as they near retirement. Also, some investors are more interested in generating regular income through dividends and distributions. Nevertheless, considering your goals when investing is important, as there are no rules. For income investors, look for stocks with good dividend yields and cash flow to support those dividends. Younger companies with promising revenue growth but unstable earnings are attractive to growth investors. For capital preservation investors, look for stalwart businesses with steady and predictable profits. Therefore, it's important to consider your age and goals when selecting companies to invest in. 2. Understand The Business Where You Invest When buying stock, you become a partial owner of a business. Therefore, without understanding the business, you risk failure. Trusting yourself to own a company fully means you need help understanding that more than appointing great management is necessary to ensure their performance. You can find competing companies everywhere, and they can impact you indirectly. For example, when you buy medicine at a pharmacy, you know who makes the equipment and who buys the spare parts. When you get a car fixed, you know who makes the spare parts and who makes the spare parts. Therefore, using these companies as a starting point for research and finding competitors in each industry can help you understand how a business makes money. If you need to understand how a business makes money fully, you may need to research or find a different company. 3. Evaluate The Market Before Investing Before adding a position, consider the broader market's movement, as 75% of stocks move with it. Moreover, buying stocks when the market is trending increases the chances of successful trades. The moving average of a major index, such as the S&P 500® Index, can show market momentum. Therefore, potential events like Federal Reserve policy meetings or earnings announcements should be considered. These events can affect your trading. Thus, following the market closely and investing when the market is trending up can increase your chances of success. 4. Determine A Fair Price Investors should consider various metrics to assess a stock's current price and value. These metrics include the following: Price-to-earnings ratio (PE). Price-to-sales ratio (PS). Discounted cash flow modeling. Dividend yield. The PE ratio is suitable for established companies with steady profits and growth, while the PS ratio is more suitable for growth stocks with unstable earnings. Historical averages can be a good guide, but future expectations should be considered. Next, discounted cash flow modeling involves estimating revenue growth, profit margin, and expenses for the next few years. Consequently, these factors are discounted by the required rate of return and divided by the number of outstanding shares. Dividend yield is also crucial, as an above-average yield may indicate a good stock price. Investors should avoid yield traps and develop their own dividend discount model. 5. Maintain Your Safety Margin To ensure successful stock picking, buying companies trading below your estimate for a fair price, known as your margin of safety, is crucial. This helps prevent losses if your valuation needs to be corrected. A 10% margin of safety is sufficient for stable earnings and a strong outlook. For growth stocks with less predictable earnings, a wider margin of safety of 15% to 30% is recommended. This ensures protection in unexpected events, such as a new challenge or a larger company entering the market. It is not necessary to get the lowest possible price for a stock; trust your research and take the price when it looks good. Building a diversified portfolio of stock picks across various sectors can lead to winning investments. Technical Signals When Selecting Stocks Technical analysis is a crucial tool for stock selection, consisting of three steps: Stock screening. Chart scanning. Setting up the trade. Stock screening involves identifying a list of 20-25 candidates using technical criteria narrowing it down to three or four candidates by scanning the charts. Moreover, the chosen candidate may be considered trading after a detailed chart analysis. To set up a screen, consider factors such as price and market capitalization, sectors and industries, and momentum. Long-term investors look for strong sectors and industry groups, while short-term investors should look for weak ones. Momentum traders typically identify strong, uptrending stocks for buys and weak, down-trending stocks for shorts. After compiling a list of candidates, look for those with good entry points, such as breakouts or pullbacks. The Virtual World Of Stocks Online investing is popular for many investors due to its ease of use, commission-free trading, and easy-to-use platforms. Moreover, opening a brokerage account with an online broker takes only a few minutes and requires basic personal information. Funding can be done through a check or electronic transfer. Online trading allows trading dividends, tech, and other stocks, with options available for a small fee. However, penny stocks, defined by the SEC as those selling for less than $5 per share, should be viewed with caution due to their volatility and potential for manipulation. It is essential to research the company's business before making a decision to invest in online trading. Read Also: Simple Tips To Diversify Your Stock Portfolio Backorder Vs Out Of Stock: Essential Things To Know About It

Mar 23, 2024

Dhani Loans & Services Limited – Background And Services

When it comes to providing the best loans and other financial services to people, Dhani is one of the leading financial companies in India. They give people some of the best in class loans and financial assistance, along with having its own e-commerce shopping center rivaling the likes of Amazon for the Indian public. But how big is this company in 2023, and how many services do they provide? If you wish to learn more about this company, read this post until the end. Dhani - Overview Dhani was initially known as Indiabulls Ventures Limited since its inception in 1995 by Sameer Gehlaut. Soon, it established itself as a significant FinTech (Financial Technology) player in the Indian market as a financial software developer for various clients. Over time, it broadened its product and service portfolio when it launched a subsidiary named Indiabulls Consumer Finance Limited in 2017. This app-based India Bull personal loan money lending service targets the personal loans market in India. At the same time, it also launched another subsidiary named Indiabulls Securities Limited to become a major player in the Indian Stock Market. This subsidiary targeted India's stock trading consultation market, which was slowly rising. In 2020, Indiabnulls rebranded itself to Dhani. This changed the names of its subsidiaries as well. Indiabulls Consumer Finance Limited became Dhani Loans & Services Limited. In addition, Indiabulls Securities Limited became Dhani Stocks Limited. After this rebranding, the company dabbled into providing healthcare e-commerce services in the form of Dhani Healthcare Limited. This health tech (healthcare technology) subsidiary started selling medicines and healthcare consultancy online amidst the rise of the pandemic. This subsidiary soon extended its services to provide a full-fledged e-commerce platform where you can buy various products online, including food products, electronics, clothing, jewelry, and more. Benefits Of Dhani Loans And Services There are several types of Dhani Loans and services that you must know at your end. You must be well aware of the reality that can make things easier for you to reach your goals with ease. Some of the key factors that you must know at your end are as follows:- 1. Instant Personal Loans Dhani provides instant personal loans online, allowing quick access to funds for various purposes, such as medical emergencies, travel, or debt consolidation. It will help you to meet your goals with complete ease. Some of the crucial facts that you must know at your end to get the loans on time. 2. Digital Process The loan application and approval process is entirely digital, making it convenient for users to apply for loans from anywhere using their mobile devices. You need to get through the complete process that can make things perfect for you in reaching your goals with complete ease. Some of the core that can affect you are mentioned here. 3. Quick Disbursement Once approved, Dhani disburses the loan amount swiftly, often within minutes, directly into the borrower's bank account. You need to get through the complete process that can make things easier for you to attain your goals with ease. 4. Competitive Interest Rates Dhani offers competitive interest rates on its personal loans, making them more affordable for borrowers. Once you follow the correct solution, it can make things easier for you to reach your goals with complete ease. 5. Flexible Loan Amount Borrowers can typically access a range of loan amounts based on their eligibility and requirements. Once you follow the correct choices, things can become easier for you to attain your requirements with complete ease. 6. No Hidden Charges Dhani aims for transparency in its services, ensuring borrowers are aware of all associated fees and charges upfront. Dhani also provides a line of credit facility where borrowers can use funds as per their needs and pay interest only on the amount utilized. It's crucial to note that while these benefits make Dhani loans and services attractive, borrowers should review the terms and conditions, interest rates, fees, and repayment options before availing of any financial product or service to ensure it aligns with their financial goals and capabilities. Dhani Loans & Services Dhani Loans and Services has been popularized using Dhani OneFreedom. When you register for this service, you will receive a Dhani Freedom Card. With this card, you can avail various benefits like: Instant Money: With this application, you can apply for personal loans up to ₹5 lacs (around $6000) with no interest. All you need to do is be a verified user and connect your online banking account with Dhani OneFreedom Digital card. In addition, you also need to verify using your Aadhar Card. Three Interest-Free Payments: This app makes it very easy to pay back your loans. No matter how much money you take as a loan, you must pay it back in three installments without additional interest. Bank Mandate Not Required: Since a bank mandate is unnecessary for this service, Dhani will never directly debit the money from your bank account. Therefore, there is no need to fear your money being debited without your consent! Dhani Store Offers: Once you become a member of Dhani OneFreedom, you can get your Dhani Physical Card for ₹99. You can use this card to avail various special offers with many partnered stores. In addition, you can also get discounts of up to 20% on groceries and household items from the Dhani Online Store. You also become eligible to receive 2% cash back on all purchases made from the online store! Plus, no extra processing fees are added to your purchases as well! Online Healthcare: With the Dhani Card, you can get online consultations from doctors through various online portals 24x7. Dhani Online Shopping Store Dhani has its own shopping store from where you can buy various products. While they initially started out as a provider of pharmaceutical products, they soon expanded to provide products like: Groceries Pharmaceutical Products Electronics Home and kitchen equipment Household products Personal care and beauty care products Baby care products Books and stationery items Healthcare products Pet care products Clothes and fashion accessories Toys and games Sports and fitness products Jewelry and fashion accessories Footwear Dhani Stocks Limited With Dhani Stocks Limited, you get access to stock trading on the Indian Stock market in the easiest way possible! There are various benefits of joining and trading in stocks using this platform. The most significant benefits are: Real-Time Stock Quotations: If you wish to buy stocks of a specific firm, you will get real-time updates regarding their stock prices. In-Depth Stock Market Analysis: Members will get various reports that will show metrics regarding the condition of the market and get predictions about rises and falls in stock prices of multiple companies. Customizable Watchlists: If you are interested in buying stocks of specific companies, you can create a watchlist to receive real-time stock price updates and news about them, tailor-made specifically for you! Trading Consultancy: If you are new to stock trading and want to invest most profitably, you can get trading consultancy using this app. Mobile Trading Platform: With the Dhani app, you get a platform to trade stocks from various platforms, which you can access anywhere, anytime. You can trade stocks using the app, website, and direct calls. Dhani Services Share Prices If you wish to invest in this company by buying Dhani shares, the current share price as of April 2023 is ₹67.75. Here is a share chart showing its fluctuating share prices in the last few months: Image Dhani Controversies In 2023, every company is flawed, even if they look to be. Every company faces its own set of issues, affecting customers and creating controversies. In this regard, Dhani has faced several controversies in the last few years. Some of the most prominent controversies that Dhani loan has faced so far are: The former non-executive Director of the company came close to doing so in 2019. That year, she and her husband possessed unpublished business information, which they used as part of an “insider trading plan” to raise Dhani stock prices. After being caught in this act, they were impounded for ₹87,20,000 ($106,781) by the Securities and Exchange Board of India. The company expressed an “inability to make a formal statement” when several women doctors were sexually harassed on their online doctor consultation forums amidst the Covid lockdowns of December 2020. A detailed report of this incident was published by the Times of India newspaper. A glitch in the Dhani Loan app confused many users when they received a message to pay for loans they had never taken in April 2021. The company issued a formal apology for this inconvenience later on. Dhani was accused of several data breaches and misuse of personal financial information by many users in February 2022. Here, users claimed that their personal account numbers were used by unknown third parties to get loans in their names. This act was done without the consent and permission of the users. Moreover, this caused the people's credit scores to significantly drop, for loans they never took as a defaulter. Conclusion Dhani is a well-established fintech and health tech company previously known as Indiabulls. It has become a significant presence in the Indian stock market, providing various services like a personal loan service and an e-commerce store. Explore More: HYIP Projects: Features Becoming A Landlord – What Should You Include In Your Budget? IPOE Stock – Present Price, Forecast, Statistics – Should You Invest In It

May 02, 2023

BNKU Stock: MicroSectors US Big Banks Index 3X Leveraged ETNs

In 2022, you can no longer avoid the necessity of investing in stocks, and BNKU stock are one of the many alternates that you might be considering. For people who are new in the world of stocks, BNKU stands for Big Banks Index Exchange Traded Notes. Issued by the Bank Of Montreal, these notes offer a lucrative return daily. The lucrative return is so much so that it is 300% of Solactive MicroSectors U.S. Big Banks Index. Moreover, the Index represents popular financial institutions of the United States and contains only ten elements. Since 2022 is being considered as the year for investing in stocks, any investor looking for an advantageous return must consider BNKU stock. About BNKU Stock: Before investing in the BNKU: ETF section, it’s best to find out more about the BNKU stock. It is an Exchange Traded Note or ETN, which is not something you can buy and hold before selling it off at the right time. Instead, these are best suited for short time periods used more often as a tool for speculation. In fact, the BNKU stock were on the rage and were up by 30% at the beginning of 2022. Even after the recent market changes, its performance failed, but the ETN still grew by 9%. However, you need to be careful with BNKU. This is because since it has a beneficial nature, the falls are always steep. For instance, during Covid, these stocks fell by more than 80%. Things are usually not very static in the stock market. For instance, if these stocks keep undergoing any major downfall, then anyone investing in these will stand to lose. But, just like any leveraged goods, for running into a loss, the actual issues do not need to default. In fact, the maturity date of the stock is 2039. If you think that the present market scenario will pass and there are going to be beneficial changes in the BNKU stock forecast, then you can start considering these stocks. Benefits Of Buying BNKU Stocks In 2024 There are several benefits you can seek from buying the BNKU stocks in 2024. You need to get through the details of this stock to have a better idea of it. Some of the essential benefits you can seek from these stocks are as follows:- 1. Company Performance Assess the company's financial reports, growth trajectory, management changes, product developments, and market position. Strong performance and positive news can positively influence stock value. The performance of the company matters a lot while you want to buy the BNKU stocks from your end. 2. Market Trends Analyze the broader market trends, sector performance, and industry outlook. Changes in consumer behavior, technological advancements, or regulatory shifts could affect the stock's performance. Try to follow the market trend that can make things easier for you to attain your goals with ease. 3. Economic Conditions Macroeconomic factors like inflation rates, interest rates, GDP growth, and geopolitical events can significantly impact stock markets. Try to consider the economic conditions of the current BNKU stocks to get better returns from your investments. 4. Competitive Landscape Evaluate how BNKU compares to its competitors. Innovations, market share changes, or disruptions within the industry could affect its performance. Once you follow the competitive landscape things can become easier for you in all possible manners. 5. Investor Sentiment Market sentiment and investor perception of the company can greatly impact its stock value. Positive news or sentiment can drive stock prices up. Try to keep things in perfect order while attaining your requirements with absolute clarity. When considering investing in stocks, especially in 2024 or any future year, it's essential to conduct thorough research, possibly consulting with financial advisors, and not rely solely on predictions or speculations. Diversification of investment and a long-term perspective often serve as sound strategies to manage risks associated with investing in individual stocks. ETN vs. ETF BNKU stock are Exchange Traded Note or ETN, and not an ETF which stands for Exchange Traded Fund. Now both are extremely similar concepts. The difference? The only difference between the two is in terms of bankruptcy chances. Well, ETNs are safer than ETFs, and we will tell you how. When you choose to invest in a bank ETF or even a bank stock ETF and start googling ‘big bank ETF,’ you fail to understand that by investing in a large bank ETF, you are investing in funds that will track and monitor all the assets it is holding. For example, your assets can be anything, ranging from stocks to bonds and gold. ETNs like the ones in the case of BNKU stock is debt note that has been issued by a financial institution and is characterized by a lack of security. As a result, it naturally comes with a maturity date. Moreover, it is always at a risk of running into a complete loss in case the organization issuing them goes bankrupt with no hope of recovery for the bond-holders. Also Check: What is BA Stockwits? Is BA Stockwits a good stock to buy BNKU Forecast For The Next 15 Days: As we discussed at the very beginning of the article, if you feel that the current market trends will pass without bringing the downfall of BNKU stock, only then is it relatively safe to start considering BNKU stock price for a change. But if you ask us now, we would say it’s best not to invest for the time being, especially if you are new in the game of stocks. We closely analyzed the upcoming forecast of BNKU stock and arrived at the following concluding points that will help you determine the market’s present state in the case of these stocks. Firstly, the BNKU stock quote goes up and down several times in the next two weeks. It starts at a minimum price of 53.019 dollars and a maximum of 58.863 dollars on 2nd March. By the 14th, both the rates decrease considerably to 43.527 dollars and 49.255 dollars, respectively. The difference in prices indicates the fluctuating situation of the BNKU stock now. It keeps reducing and increasing every alternate day. One day it’s more than the day before, and on the next day, it’s lower than both days. However, the changes are not significant initially but gain significance towards the end. The fluctuating market in the case of BNKU stock is also indicative of the lack of security that comes associated with the same. However, the question that you must ask yourself is whether, as an investor, you are willing to take the risk or not. Frequently Asked Questions!! (FAQs): 1. What Is The BNKU Stock Fund Price Today? Ans: The Microsectors U.S. Big Banks Index 3X leveraged ETNs fund price is 51.500. 2. Will Microsectors U.S. Big Banks Index 3x Leveraged Etns Fund Price Grow / Rise / Go Up? Ans: Yes, MicroSectors U.S. Big Banks Index 3X Leveraged ETNs fund price is forecasted to grow from 51.500 dollars to 61.593 dollars in a single year. 3. Is It Profitable To Invest In Microsectors U.S. Big Banks Index 3x Leveraged Etns Fund? Ans: Yes, it is profitable to invest in MicroSectors U.S. Big Banks Index 3X Leveraged ETNs fund since you can earn upto 19.60% in the long run. Verdict: To Invest Or Not To Invest? As repeatedly discussed throughout the article, we would ask you to take some time whether deciding to invest in BNKU stock even if the phrase ‘BNKU stock quote 3x’ or even ‘BNKU stock rex shares’ is everywhere. Yes, it is a leveraged product that gives the surety of significant gains usually, but since the pandemic hit us, stocks like everything have become unreliable. Stocks are already unreliable entities, and successful investors usually are fortunate risk-takers, but you cannot reach there on day one. However, after carefully analyzing the performance of BNKU stock in recent times, in our opinion, it is riskier than usual to invest in these stocks. We would recommend you wait for a few more months before going ahead with this. Disclaimer: Dear readers, all the above-mentioned data on BNKU Stock Price and other facts are assumptions. All the information mentioned above refers to data being present in the popular crypto market websites. The values are subject to change based on the situation. Please be aware that share/stock and crypto markets are subject to risks. More Resources: Is Twitch Stock Worth Buying Now? Everything You Should Know EUA Share Price Forecast: Everything You Should Know Is PHI Stock A Good Buy? Everything You Should Know

Mar 09, 2022

FlexSalary: Information, Eligibility Criteria, Interest Rates, Review & More

The FlexSalary App is a loan app that is run by an Indian NBFC named Vivify India Finance Pvt. Ltd. The company is registered with the Reserve Bank of India. However, there are not many good reviews regarding the app. However, the app and the company seem legit. Hence, we have dived deep and reviewed the app in this article for you. This article will consist of a review of FlexSalary, which claim to be one of the "Best instant loan app in India without salary slip.” Furthermore, we will also give you details about the interest rates, eligibility, and other loan-related information. Finally, we have also added some useful customer reviews regarding Flex Salary. Hence, to get fully informed about FlexSalary, read on through to the end of the article. FlexSalary – What Does It Offer? FlexSalary is an app where you can get a loan if you are a salaried individual. According to the official website of the company, “FlexSalary is an instant salary advance credit line that covers emergency needs of Indians before they get paid. It aims to aid all individuals who face a mid-month crisis by providing short-term lines of credit loans until they receive their salaries. We offer instant loans from Rs. 4,000 to Rs. 2,00,000 with flexible repayment terms.” It basically offers a personal line of credit. Even if you do not have a credit history, you will be eligible to get a loan from FlexSalary. If there are people who cannot find any other way to get financing, FlexSalary offers an unsecured line of credit. Loan AspectsWhat FlexSalary Offers You?Loan Amount₹ 4000 - ₹ 2,00,000Loan Tenure10 months to 36 months (Based on the loan applied for)Rate Of Interest On loans10% to 12% per annumLoan Processing Fees₹ 650 only (One-time payable only upon Loan Disbursement)Collateral Or MortgageNo collateral requiredLoan Review TimeDepending upon the amount of the loan (may take from 5 minutes to 7 days)Late Payment Of The LoanUp to 5 %, depending on the type of loan applied for.Loan RepaymentLoan repayment is made automatically from the provided bank details as per the approved schedule. Repayment should be made through the mobile app of FlexSalary.FlexSalary Customer Care Number+91-40-4617-5151+919908935151+919100038349CIN NumberCIN U65923TG2016PTC110767AddressUnit A, 9th Floor, MJR Magnifique, Survey No 75 & 76, Khajaguda X Roads, Raidurgam, Hyderabad, Telangana – 500008. Is FlexSalary Safe? Yes. FlexSalary is fully legit and safe. The website is also safe to use as it is HTTPS-secured and SSL certified as well. However, regarding the customer service of the company, many borrowers of loans have complained. Despite that, as per our experience, we think the app works quite well and is legit. Furthermore, the company has a CIN number, and it is registered through the Reserve Bank of India. When Can Flex Salary Comes To Rescue? There are certain circumstances where flex salary comes to the rescue. You need to get through the possible solutions that can make things easier for you. You need to follow certain steps that can make things easier for you to attain your requirements with ease. 1. Don’t Have Collateral Flex salary will offer you unsecured lines of credit loans. You do not have to pledge to your assets if the collateral gets approved for your loan. You need to get through the complete process that can develop things in perfect order. 2. If Your CIBIL Score Is Low Flexsalary will not focus on your CIBIL score to provide you with the loan you need in times of crisis. If you have a low CIBIL score then you must go through the best flex salary options to meet your requirements with ease. 3. Need An Emergency Cash If you are facing a medical emergency and you need the loan on an immediate basis, then you must consider using Flex salary. You need to identify the perfect solution that can make things lucid for your business development. 4. Loan Is Rejected By Banks If you have low income, bad credit history, and banks have rejected your loans, then Flex salary can be the best option for you. Flex salary will offer you loans at times of crisis. You do not have to pay any kind of interest to get these loans. 5. Don’t Want To Pay Excess Interest If you are afraid of bearing the higher interest rates on your loan, then Flex interest loan amounts can be one of the best options for you. If you do not use money, you do not have to pay the interest. 6. If You Need A Loan For A Lifetime Flex salary personal line of credit you can receive for a lifetime. Your credit limit gets filled up once you pay back the withdrawn amount. It works almost like that of a credit card. You need to identify the perfect solution that can make things easier for you. Can You Get An Instant Personal Loan For Your Marriage From Flex Salary? Yes!! You can receive an instant personal loan for your marriage when you opt for the flex salary. If you have an urgent need for cash in order to meet your marriage-related expenses, then Flex salary can be of great help to you. You will get the help for money within a few hours. It can help you to get the desired amount of money for a personal loan when you need it the most from your endpoints. How To Do FlexSalary Login? – Steps To Follow The following are the steps through which you can apply for a loan through FlexSalary: Step 1: Visit their official website and click on "Apply for an Instant Loan." Step 2: You will get a form on the next page, which you will need to fill out and add information into. Add all the documents required to get a loan from the FlexSalary platform. Step 3: There are various verification processes available. You can either apply for Net Banking Verification or you can upload the documents on your own. Once you upload the documents, they will verify your credentials and will tell you what you are eligible for. Through the app, it is almost the same. All you need here is to download the app and register your account with it. FlexSalary – Eligibility Of The Loan Loan RequirementsEligibilityAge Of the Borrower22 to 60FlexSalary Credit ScoreDepends on the type of loan applied for.Type of EmploymentSalaried professionals only.Minimum Monthly Income₹ 8000 (However, it can change depending on the loan amount applied for)Work ExperienceWork experience requirements depend on loan terms and amounts. Required Documents1. Salaried Employees- Identity Proof (Aadhaar / Driving License / Passport / Voter ID) - PAN card - Address Proof (Driving License / Utility Bills / Aadhaar / Passport / Bank Statements / Voter ID) - Last three months Pay Slips - Photo with the applicant’s face clearly visible. (The applicant will be prompted to take a selfie or upload a photo while applying for a loan through the FlexSalary mobile app) - Net banking verification to validate the bank account and salary information of the applicant 2. Self-Employed Individuals- No loan is allowed for self-employed- The applicant must have an employment FlexSalary Reviews From Customers The following are some of the useful customer reviews regarding FlexSalary that you can benefit from: Syed Abrar: “I'm very happy much satisfied with the service Uma Maheshwari are very nice she was helped me through out the process I got the loan amount as soon as the documents were collected best app.” Manjeera Dhfm: “My credit limit was activated in 1day. But I was not able to withdraw amount,due to my account issue, then customer support team interacted with me continuously and solved the problem. Thank you team. They are well mannered employee's who have patience to listen the issue and resolve it quickly.” Selva Raj: “Last month urgently required some amount, one of my friend referred me Flexsalary and they had treat me as a friend and pay me the amount with very minimum documents. Thank you Flexsalary very fast, very effective good customer service really appreciate your overall performance.” Summing Up Hope this article was helpful for you in getting a better idea of the FlexSalary platform. If you are hoping to get a loan from this platform, you need to download the app and register your account. Furthermore, you need to upload all the necessary documents. They will verify and give you the loan within one to five days if you are eligible for it. Do you know of any better loan app, which is registered by the Reserve Bank of India, and offers instant personal loans? Share some of them with us in the comments section below. Explore More: The Amazon Store Card All You Need To Know About BNKU Stock: MicroSectors US Big Banks Index 3X Leveraged ETNs IPOE Stock – Present Price, Forecast, Statistics – Should You Invest In It In 2022?

Apr 28, 2023