Navi: Information, Eligibility Criteria, Interest Rates, Review & More

You can get Navi personal loan with minimal documentation. Furthermore, if your documentation and your Navi loan application are cleared, you will be able to get the loan even within a few minutes. You can get fast personal loans at 9.9% per annum onwards. This digital instant loan app of Navi gives you fast loans, and also at zero processing fees.

In this article, you will mainly learn about some of the essential features of Navi personal loans. Apart from that, you will also learn about the Navi personal loan interest rates, as well as eligibility criteria, documentation required, and more. Hence, to learn more about the Navi personal loans, read on through to the end of the article.

Navi Personal Loans – A Brief Overview

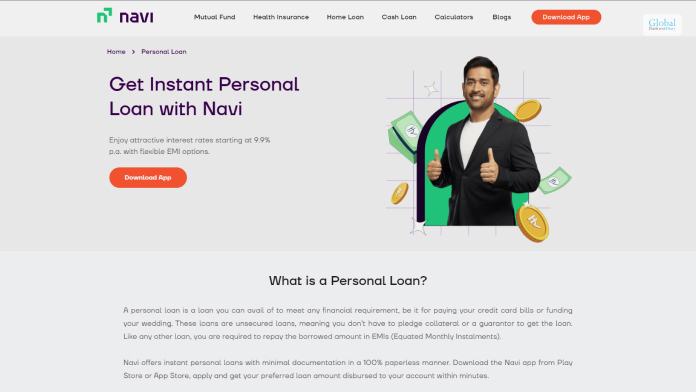

A personal loan is something that you need to meet any financial requirement if you somehow lack finances at the moment. The loan might be needed to pay your credit card bills, wedding, health expenses, buy something important, and many more reasons. Hence, you need a financial company like Navi to offer you personal loans. Navi is just like personal loan-offering companies like India Lends, CASHe, and others.

Navi, also known as Navi Finserv, offers personal loans up to ₹20 lakhs (INR). The borrower of the loan can get the amount through the Navi app, and also with zero processing fees. Apart from that, the loans are fully paperless and are available after you share your PAN and Aadhar number. Once your documents are verified, and your loan application is cleared, then you can get the loan in as fast as ten minutes.

According to the official website of Navi,

“Navi offers instant personal loans with minimal documentation in a 100% paperless manner. Download the Navi app from Play Store or App Store, apply and get your preferred loan amount disbursed to your account within minutes.”

One of the best things about Navi personal loans is that you will have access to unsecured loans. This means you will not offer any collateral for the loan, nor do you need a guarantor for the loan. Like just any other personal loan option, you will only need to repay the amount you have borrowed in Equated Monthly Instalments or EMIs.

Furthermore, if you want to get returns by investing in mutual funds, you can do that by looking for Navi mutual fund or Navi nifty 50 index fund. In addition to that, there is also Navi health insurance, which you can buy to purchase health insurance plans.

Navi Loan Interest Rate, And Other Loan Highlights

The following are some of the highlights of Navi personal loans that you will need to know about:

| Navi Personal Loan Highlights | |

|---|---|

| Rate of Interest | 9.9% to 45% of the principal amount |

| Available Loan Amount | Loans of up to ₹ 20 lakhs are available |

| Tenure of the Loan | The loan is available for up to 6 years |

| Preclosure fees of the loan | There is no preclosure fee for Navi Loans. (There is no disclosed amount. Contact the lender of the loan to know more.) |

You can see from here that the minimum rate of interest for Navi personal loans is 9.9%. However, the rate of interest can rise to 45% based on a variety of factors. These include – monthly income, age, job profile, loan repayment history, credit score, and many more.

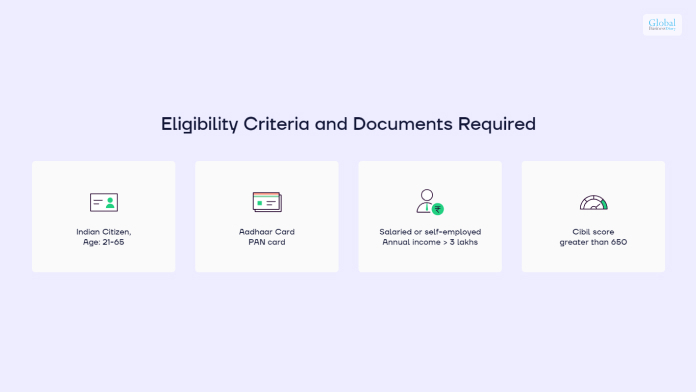

Navi Personal Loan Eligibility Criteria

The following are some of the essential eligibility criteria of the Navi personal loan that you need to clear if you want to avail of personal loans:

| Factors | Eligibility |

|---|---|

| Nationality | – Borrower must be a citizen of India |

| Occupation | It must be either of the two:- Salaried- Self-employed |

| Age | – The loan applicant must be aged between 18 to 65 years.- The minimum required age can be increased to 21, 23, or 25 years in special cases. |

| Credit Score | – To avail of the Navi personal loan, a borrower needs to have a minimum credit score of 650 (CIBIL score). |

| Documents Required | – PAN Card- Aadhar Card |

Navi Loan Minimum Salary

Every credit company has a base line salary criterion. But why?

This is mainly to ensure that you can pay back the loan you take.

How is it determined?

A threshold is considered. It is INR 15000 on most occasions. However, there are other factors that decide whether you will get a loan with INR 15000 salary.

Firstly, your creditworthiness matters. You are ineligible if you have an INR 15000 salary with a low credit score.

However, you can get a credit line from Navi if you have a minimum credit score of 650.

A person with credit score of 650 means two things:

- No or minimal credit repayment default cases

- Average credit worthiness, as evaluated by other credit companies earlier

The next threshold salary bar is INR 20000. It implies that your loan value will be greater as well.

However, the banks that grant INR 20000 as the threshold eligible salary for credit, will not consider INR 15000 as threshold.

For instance, IDFC First Bank gives loan against a minimum salary of INR 20000.

But there are no schemes that can get you a loan if you have INR 15000 salary.

Moreover, there are differences in credit worthiness of the two individuals. In simple terms:

- An individual with INR 15000 salary may get up to INR 1500000 as loan.

- An individual with INR 20000 salary may get up to INR 2500000 as loan.

Benefits of taking a navi loan minimum salary

The navi loan minimum salary is INR 15000. But it may be higher if your credit performance is not good. Ideally, you must have a credit score of 650 with a minimum salary of INR 15000.

If you wish to take loan against this threshold criteria, you may get the following benefits:

- No collateral against the credit line/loan that you get.

- The repayment tenure might span up to 5 years.

- You might have to pay slightly more interest, but you may get a favorable EMI breakdown.

- You can get your credit line from Navi, immediately approved.

- You can do KYC and documentation prior to approval online, in minutes.

- If your loan is around INR 15000, it will take almost no time to be disbursed.

- As there are no collaterals, there are no instances of validation, once KYC is done.

- You may get a small credit line against minimum salary, but you can pay back and get a higher credit line.

- No concealed charges are applicable, as you get to know the final repayment value, before you sign the disbursal letter.

Other miscellaneous eligibility criteria applicable

You must have a fixed salary from an acceptable source. However, you can be self-employed as well. For instance, you may run a coaching center. Mostly navi loan minimum salary comes with the criteria of 1-2 years of minimum work experience.

Lastly, navi loan minimum salary is INR 15000, only when you are 23 years of age at the least.

There are no hidden clauses. If you meet the two main criteria (min salary of 15000 and 650 credit score), you will get a loan easily.

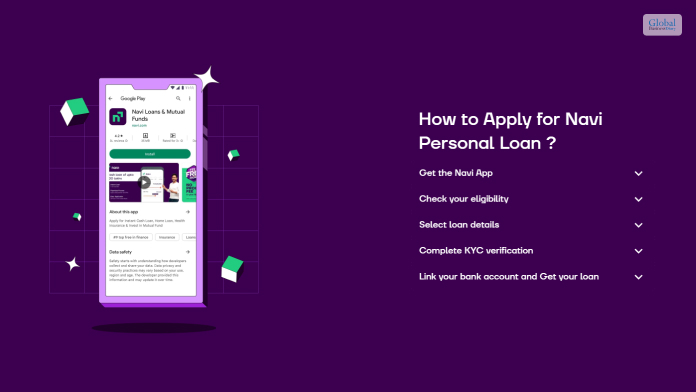

How To Apply For Navi Personal Loan? – Steps To Follow

Once you are okay with the essential features associated with Navi personal loans, you will need to apply for a personal loan from the Navi app. Here are the steps you need to follow to apply for a personal loan from Navi:

Step 1:

Go to Play Store or App Store, and download the Navi personal loan app. Install the app on your Android phone or iPhone.

Step 2:

Register your mobile number on the Navi server through your app.

Step 3:

Check the eligibility of the loan, and fill in your personal details through the app.

Step 4:

On the app, go to the next page, and select the loan amount and the EMI amount.

Step 5:

Once you have the amount, you need to complete the KYC process, where you need to produce your Aadhar and PAN numbers and upload a selfie of yourself.

Step 6:

Enter your bank account details which are needed for the transfer of money.

Step 7:

Apply for the loan. Once your loan is verified, you will get your loan fast. The money will be transferred to your amount within the time specified to you.

Is Navi Approved BY RBI?

Now many people ask whether Navi is approved by RBI or not. Then, in this case, the Navi official website claims,

“RBI does not approve digital lending apps. The Navi App is operated by Navi Technologies Limited. Navi Finserv Limited is an RBI registered Systemically Important Non-Deposit Taking NBFC (ND-SI) which lends through the Navi App. Navi Technologies is the digital lending partner of Navi Finserv.”

Frequently Asked Questions!!! (FAQ):

Ans: Navi offers personal loans for attractive interest rates that start from 9.9% with some flexible EMI options upto 72 months. You need to get through the right options that can assist you in attaining your requirements with complete ease.

Ans: NAVI loan is a legit application that offers you health insurance services as per your requirement. You have to get through the complete process that can make things easier for you to attain your requirements with complete clarity.

Ans: Yes!! Navi personal loan is approved by RBI. You have to get through the complete process that can make things easier and effective for your business in the correct order. You should follow the right process that can make things easier for you to get the loan on time.

Ans: If your age bracket is between 18-45 years then you are eligible for the Navi Loans. You have to get through the complete loan process can make things easier for you to get the loans on time. Try to figure out the reasons for getting or not getting the loans.

Ans: You need to be an Indian citizen within a period of 21-65 years. You cannot make your selection and choices in the incorrect end. You need to have 3 lakhs of money as your salary.

Summing Up

Hope this article was helpful for you in getting a comprehensive idea of what to expect from Navi personal loans. If you are looking for a quick personal loan, you can apply for one through the Navi app; however, as you have seen that the rate of interest can change as per the loan amount and the applicant’s details. Do you know of any other app that offers similar loan rates? Share your answers in the comments section below.

Read More:

Tags:

Recent

Due Diligence Decoded: Why Careful Evaluation Still Wins in Business

Jul 11, 2026

How Hydraulic System Design Impacts Equipment Performance

Jul 01, 2026

Startup Bootstrapped Fundraising Strategy: A Guide for SaaS and Tech Startups

Jun 21, 2026

Where Distributors Lose Profit Without Realizing It

Jun 20, 2026

Related Articles

10 Best Investment Apps For 2021 – Globalbusinessdiary

When I was undergoing a significant financial crisis a few years back, I looked for the best investment apps to get my economic life back on track. But, as there were no good articles on this topic, I faced a lot of trouble figuring out the best investment app. That’s why we decided to shed a bit of light on this topic. Now, the best investment apps can handle your daily financial tasks without much drama. They can also help you trade stocks quickly, keep track of your spending habit, and can help you learn about the market. So, if you are looking for these apps, you are already one step ahead in the game. What Are The Best Investment Apps For 2021? The best investment apps that we will recommend on this list are the best for beginners and professionals alike. So, let’s have a look. 1: Invstr From real-life investing to help beginners make their way in the stock, market-you can get everything on this app. It is best investment apps on this list. In addition, it has a fantasy stock game where you can guide people in managing a $200 billion portfolio. You can also get up to $1 million of virtual cash, and thus you will know to control your spending habits. But, if you manage to perform well in the fantasy game, you can also win some real cash. You can even buy fraction shares without any commission in this app. 2: Wealthbase Wealthbase best investment apps as a new entrant in the world of stock market games. There are several unique features in this app. You can even play fun games of picking stocks with friends. In addition, it has excellent incorporation with social media profiles, so you can get daily updates of stocks that your friends are picking. The best thing about this app is that it runs very smoothly without any hassle. Even if you are not interested in picking stocks, you can simply use this app for fun. The best way to learn about stock picking with friends and social colleagues is through this app. 3: Wealthfront One of the largest and best investment apps currently on the market today is Wealthfront. It uses a low-cost ETF to construct your portfolio and evaluates how much risk you will have in a single investment. When you deposit money here for the first time, it will start monitoring your account. But, you simply need to add money to your account, and the rest of the pressure, the app will handle itself. The cash management account here is also quite good. You can also manage your account for up to $5000 for free. You May Also Like: Top 7 Best Types Of Marketing On Which You Should Focus 4: Acorns It is the most popular investment app on this list and is undoubtedly one of the best investment apps. It will construct your portfolio for all your cash dealings up to your retirement. So, if you use this app, it will be for your lifetime. Of course, if you link your debit or credit card to this account, Acorns will help you manage that too. You will get some automatic investment options here without worrying about cash management. For example, you can get an FDIC-protected checking account without any extra fees. You can also get access to thousands of ATMs to withdraw your cash. 5: Betterment If you want to learn socially responsible investing, Betterment is best investment apps. It will make your portfolio and help you invest in socially responsible initiatives such as climate change or global warming. It is a good option for many people because it costs way less than other investment apps. If you want a professional financial portfolio without any effort and at a low cost, the Betterment app is your option. It will set goals for you, plan your retirement budget, and there’s even no restriction to minimum money disposal here. 6: Robinhood If you want an app with a smooth interface and without trading commission, RFobinhood is your best option. Best investment apps on our list, Robinhood lets you navigate the stock market easily. You can access the stock page from the search bar. As you navigate the market, you’ll be moving from screen to screen. The first time you deposit this account, you will get instant delivery of $1000. So, this app helps you to learn to trade almost instantly. It will show you the simplest way to navigate the market, and that’s why beginners seem to prefer it a lot. 7: Webull Commission-free trading options and allowing investors to trade stock for free are the best features of this app. But, this app won’t offer you any free trading option when it comes to cryptocurrencies. Unlike the other apps on this list, Webull lets you set up an IRA account and likea taxable account. Multiple asset classes are available on this app so that you can take them anytime you want. In addition, you only need to deposit a minimum of $50 to get started on the fantastic financial management journey. 8: Stockpile We call it best investment apps because of its neat presentation and organized outlook. You can purchase a fraction of the shares of other companies. You can also get some gift cards here that you can redeem for stocks. You can track your investment anytime and anywhere in the world with this app. If you like investing but don’t have enough budget, Stockpile should be your go-to option. You can also gift stocks to young relatives and help them learn the tricks of stock picking. 9: TD Ameritrade This electronic platform is the best when dealing with preferred stocks, common stocks, and futures contracts. Even it is one of the best investment apps for long-term investment planning and retirement planning. But, a minimum of $2000 deposit is required to open an account in this app and start operating. But, the option of commission-free trading services on ETF is also available on this app. It means you can hold on to an account and also get your broker for free if you have already made the $2000deposit. 10: SoFi If you are a SoFi member, you know why it is one of the best investment apps in the market today. There is a wide array of financial services, and most of those are exclusive to students. You can learn to manage loan refinance, mortgage, credit card management through this app. It is a user-friendly app that is optimized for both PCs and smartphones. So, even if you are outside, you can look at your cash management details from your phone. Its customer support is indeed praiseworthy. Conclusion If you are still reading, that means we have given you some good suggestions here for the best investment apps. So, if you are struggling to manage your personal finance, make sure you use one of these apps. You’ll never look back in life anymore and regret careless spending if you use these. Read More: The Amazon Store Card All You Need To Know About 5 Differences Between Mass-Market Paperback Vs. Paperback How To Build An Ecommerce Website To Boost Your Business

Sep 01, 2021

Wings Of Luxury: Exploring The World Of Jet Charter Within Your Budget

Commercial airlines have seen their service and reputation worsen in recent years. Nearly every week has seen more and more news stories about passengers being stranded at an airport or airline companies refusing to honor promises they gave their customers. Fliers have become stressed and are questioning their decision to choose to fly in the first place. As a result, private jets are becoming more attractive options for potential flyers. These jets help carry passengers hundreds or thousands of miles in the shortest amount of time possible. They are convenient and often provide much higher levels of customer support than traditional airlines. What determines private jet prices? Private jet flights are priced differently from traditional commercial aircraft. For commercial aircraft, people pay for individual seats on a large plane. Seats are more expensive based on legroom, amenities, and the level of comfort that they provide. So many individual tickets are sold that the various fees associated with maintaining the plane are all lumped into a single price for every flight. In exchange for relatively low costs, flyers have to deal with a wide variety of issues related to customer service, on-time flights, and a generally stressful flying experience. All of these factors are considerably different from private planes. The costs associated with private planes are more closely tied to the actual operations of the plane itself. Unlike commercial flyers, individual flyers have to worry directly about the airport they are headed to and the location of their flight crew. Planes taking off without conveniently located flight crews may have to pay an extra fee to bring in-flight crews from other locations. Private fliers also have to pay for basic airplane maintenance and treatments such as deicing. On the other hand, private fliers do not have to endure many of the indignities of commercial airplane travel. They are able to fly into smaller airports that often have shorter wait times than the nation's biggest airports. More locations may be available to them as they choose where they want to fly. All of the seats on a private jet are also the same and offer the same level of service in most instances. There is no discrepancy between different types of passengers. How to reduce costs The best way to reduce costs for a private jet flight is to be as flexible as possible. Changing times, dates, and airports can all impact the potential cost of a flight. A group of people can structure a flight to take the smallest possible jet and the smallest number of flights. Potential flyers can work with the owner of the plane to find a situation that is the most cost-effective for everyone involved. They can also set up frequent-flyer or share-buying programs for planes. These programs can reduce costs by securing flights and revenue for the plane owner. Use Of private jet cost estimator Anyone who is interested in reducing their private jet prices needs to see all of their options and all of the companies they may want to fly with. A private jet cost estimator can help with this process. They need to look at their finances and the wide variety of investments they may want to make in private flights. People with a large number of assets and a need to fly frequently should certainly consider the possibility of buying shares in a plane. Buying shares in a plane can result in lower costs per flight. There is also the potential for even making money in a handful of plane-sharing arrangements if the plane is rented out to other people when its owners are not using it. Finally, those interested in private flights need to contact a number of professionals in this field who have years of experience working with a wide variety of private flyers. There are some agents and other flyers who are happy to provide tips, advice, and suggestions for how to cut down on private flight costs. These people make up an exuberant community of private fliers who are happy to spread tips and ideas about this approach to flying. By taking these steps, potential private flyers can save as much money as possible on their flights. Read Also: International Flights Likely To Get Cheaper As India Signs Pact With 116 Countries What Training Courses Are Available For Boeing Aircraft? Profitable Business Ideas To Start In UAE

Sep 15, 2023

CASHe Personal Loan App: Information, Eligibility Criteria, Interest Rates, Review & More

Are you looking for a quick personal loan? Then CASHe is a great option for you, where you will be able to get short-term loans at low-interest rates. This platform is specifically created to offer short-term loans to young-salaried and self-employed people. The loans are of instant disbursal. You can get personal loans, even if you do not have a credit history. In this article, you will basically learn more about CASHe loans and the major features of the CASHe app. Furthermore, we will also share some of the major reviews of CASHe, which can be beneficial for you to get an idea of the platform in general. CASHe – How Does It Work? CASHe is a personal loan app that uses a credit scoring mechanism called Social Loan Quotient, which is based on artificial intelligence. In this mechanism, the CASHe app leverages various alternative sources of data coming from smartphones, social media and others. Furthermore, monthly salary, education, career experience, and basic KYC experiences. This is mainly done to evaluate a loan borrower’s worthiness of credit. CASHe App: How To Download The CASHe Loan App? The following are the steps that you need to follow to download the CASHe app: Step 1: Go to Google Play Store on your smartphone. Step 2: Type " CASHe " on the search bar and tap on the search button. Step 3: Click on the app named " CASHe” Step 4: Download and install the app. You can also use the CASHe promo code to get good offers on loans, as well as various graces on the rate of interest. Apart from the app, you can also visit the CASHe official website to see various details of the loan. If you want to get yourself a loan, go to the instant personal loan section, and click on the “Get a Loan” button. You will need to fill up a form and choose the type of loan you need. Furthermore, you will need to upload scanned documents about your personal details. After all these documents get properly verified, you will get the loan in no time. You can also get the loan within the same day. CASHe Loan Details CASHe Personal Loan DetailsCASHe Interest Rate2.25%Loan Amount₹1000 to ₹4 lakhLoan Tenure3 months to 18 monthsMinimum Age of Loan18 yearsLoan Processing FeeUp to 3% of the loan amountMinimum Income (Monthly)₹12000CASHe Loan Websitehttps://www.cashe.co.in/instant-personal-loan/CASHe Complaints numberNot available on the website The CASHe interest rates range from 2.25% per month to 2.5% per month (or 27% per annum to 33% per annum), based on the repayment tenure that you have chosen in terms of your loan. Once you have chosen your loan type, you will only need to pay accordingly. What Are The Eligibility Criteria To Get CASHe Personal Loans? Here are the eligibility criteria you will need to fulfill to get an instant personal loan from CASHe: You need to be at least 18 years of age. Minors are not eligible to get loans from CASHe. Your maximum age should not be more than 58 years. You must be at least employed for three months in your current organization where you are employed. You should be able to provide valid income proof. Your monthly income should be at least ₹12000 per month. You can only get a loan where the loan to value is 30% to 200% of your monthly salary. However, it depends on the type of loan that you choose. You can make use of the cashe promo code to get the loans on time. What Are The Documents Required For Loan Application? There are several types of documents that are required for the loan application of the Cashe Loan. You must have the following documents with you that you should make use of the Cashe Loan documents while making the application of personal loan. Photo Identity Proof as well as PAN card. You have to show your latest salary slip and income proof. You must use the Aadhar Card or any identity proof. Permanent Address proof you have to show to get the loan. You need to show up the latest bank statement where your salary is credited. You need to be well aware of these above factors while you want to get the things done in perfect order. You should take care of the facts that can make things easier and effective for you in all possible manners. Types Of Personal Loans Available At CASHe There are various types of personal loans that you will be able to get through CASHe. Different types of loans include car loans, two-wheeler loans, medical loans, education loans, consumer loans, mobile loans, travel loans, and marriage loans. The following are the major types of personal loans options that you will be able to get through the CASHe app: CASHe 180 Tenure of the Loan6 monthsMinimum Salary required to be eligibleINR ₹22,000Minimum loan amountINR ₹25,000Maximum loan amountINR ₹2,10,000 CASHe 270 Tenure of the Loan9 monthsMinimum Salary required to be eligibleINR ₹25,000Minimum loan amountINR ₹50,000Maximum loan amountINR ₹2,58,000 CASHe 1 Year (360 Days) Tenure of the Loan12 monthsMinimum Salary required to be eligibleINR ₹40,000Minimum loan amountINR ₹75,000Maximum loan amountINR ₹3,00,000 CASHe 1.5 Year (540 Days) Tenure of the Loan18 monthsMinimum Salary required to be eligibleINR ₹50,000Minimum loan amountINR ₹1,25,000Maximum loan amountINR ₹4,00,000 Other Types Of Personal Cashe Loans Availaible Today There are different types of cashe Loans available today that you must be well aware off. You cannot just make your choices in gray. You need to follow some of the essential facts that can make use of the Personal Cashe loans available for you in all possible manner. Some of the key factors that you must be well aware of are as follows:- Instant personal loan. Travel loan . Two-wheeler loan. Mobile loan. Marriage loan. Home renovation loan. Education loan. Consumer durable loan. Car loan. Medical Loan You can make use of the Cashe Promo code to get some discounts on these mentioned above loans. You must make things work as per your requirements. It will help you to get the desired loans on time. Explore the best loan options that fits your budget and requirements. Otherwise, things can turn worse for you. Cashe offers personal loan based on the loan tenure within a particular point in time. The details of getting the loans and its procedures you can get from their sites of paisabazaar.com. It will offer you all the complete details how you can afford these types of loans as you need. Know Before You Borrow: Things to Consider When Choosing Quick Loan Apps Read about the factors that are considered when it comes to choosing the right app! If you plan to choose a quick loan app, you must check a few things first. It starts with the following factors: Easy Application Process When choosing an instant loan app, ensure the application process is simple and easy. The entire process has to be straightforward and user-friendly. Always avoid apps with complex application procedures and require too much paperwork. You should be able to complete your application process straight from the smartphone. Loan Eligibility & Amount Some of the apps are designed for professionals. On the other hand, when choosing an app, ensure it doesn’t put high bars for loan approvals. For example, many loan apps require a significantly maintained credit score. Some apps require a good credit score, age limit, etc. Interest Rate Always ensure you get a good interest rate when taking a loan from an instant loan platform. The interest rate decides the overall amount you have to repay throughout the entire lifecycle of your instant loan. Typical Repayment Options It’s best to have a flexible repayment option. The repayment option should suit your financial situation. While some of these instant loan providers offer shorter repayment options, others also offer a long tenure. If you want flexibility with your loan repayments, you should go for providers that allow an extension on your repayment. Fast Disbursement Instant loans are all about your loan getting disbursed as soon as possible. But that’s not always the case. Some instant loan providers often take a long time to disburse the loan amount. So, when choosing personal loans, ensure you’re getting it from a reliable platform that disburses the loan right after approval. When approved the money should get credited to your account. Customer Support In case you are struggling to get the loan approved or want assistance regarding repayment tenures and flexibility, there should be a customer support team helping you. Whether during your repayment tentures or during application, the customer support team of the loan platform should help you. So, always choose a platform with a reliable customer support team. CASHe 1.5 Year (540 Days) Reviews – CASHe Review, CASHe Loan Review, And CASHe App Review Let us go through the reviews that are significant in understanding the apps where you can get a loan. Here are some of the major CASHe loan reviews that you must look for: Review 1: Review Source Review 2: Review Source Review 3: Review Source Summing Up One of the things we do not like about CASHe is that there is no CASHe loan customer care number for any types of CASHe complaint. Here, the safety factor goes away completely. However, the reviews for the loan platform are mixed. So, check your loans properly, before you get a personal loan. Share with us in the comments section what you think about CASHe. Read Also: Maximizing Tax Refunds: Tips And Tricks For Canadians Speed Up Your Funding: A Quick Guide To Business Loans Starting A Business In The USA – 4 Tips To Kickstart Your Venture

Mar 24, 2023

Becoming A Landlord – What Should You Include In Your Budget?

While landlords continue to benefit from high levels of private demand in light of sky-high property prices, there’s no doubt that those who operate individually can find it harder to achieve a sustainable profit than organizations. One of the main reasons for this is that 43% of landlords own just one rental property, with this representing some 20% of tenancies. Of course, owning just a single property can be challenging due to many of the different costs and factors involved. But what are the key considerations that you should factor into your budget? 1. The Mandatory Requirements Let’s start with the basics; as your first step should be to budget for the mandatory requirements that you’ll have to address as a landlord. For example, you’ll need to fund a number of checks and inspections each year, in order to ensure that the property is safe and liveable. For example, you’ll have to ensure that gas and electrical safety checks are carried out by qualified tradespeople, while you also have to inspect any appliances that you left installed on the property. EPC checks are also required to evaluate a property’s energy efficiency and performance, based on factors such as insulation and how much it costs to heat the interior. Similarly, you’ll need qualified electricians to check all smoke and carbon monoxide alarms installed within the property, as these must remain functional at all times. 2. Circumstantial Costs As a landlord, you’ll also have to consider various circumstantial costs, each of which helps you to manage your property and provide a financial safeguard in the event of your property being damaged or vandalized. One of the most apparent circumstantial costs is lettings agency fees, which you’ll need to pay when listing your property for rent. If you also want an agency to manage your property and tenancy agreements, you’ll also have to pay a premium for this service. While it may be considered an additional cost, we’d argue that landlord insurance is an incredibly important expense. In fact, this should be seen as an investment, as it protects your property and provides coverage in the event of structural damage being incurred. 3. Are There Any Other Potential Costs Before we go, it’s important to consider any other costs that may be required when owning property as a private landlord. For example, if you don’t employ the services of a property maintenance firm, you’ll be physically and financially liable for all maintenance and repairs carried out at the properties that you own. You may also have to cover the cost of utilities (depending on the nature of your tenants and individual contracts), so this may need to be incorporated into your budget. In between tenancy agreements, you may have to redecorate your properties and have them professionally cleaned. This will depend in part of the state property is in at the end of the previous tenancy, but some level of cleaning and refurbishment may be required as a matter of course. Read Also: How To Sell Off Plan Property In Dubai? How Sustainability Sets Up Real Estate Developers For Success Maximizing Home Insurance Coverage For Your At-Home Business With Riders

Feb 20, 2023