Fullerton India Review: Things To Know Before Taking A Loan!

Nowadays, if you are in need of money, whether it’s for personal uses or for your business, getting it instantly is a major convenience. Therefore, many new loan institutions are cropping up globally. One such company from India that I am going to discuss is Fullerton India Ltd.

To learn more about this Kolkata-based company, read this post till the end!

Fullerton India: Company Overview

Fullerton India credit company Ltd is a new finance company originating from Kolkata, India. With its headquarters in Park Street, they have managed to gain a lot of traction lately by providing instant loans to people and businesses.

One of the primary reasons they have become popular is because of how easy it is to get approved loans from Fullerton. Plus, their loan application processes are easy – you can do them entirely online if you wish to! In addition, you don’t need a Fullerton India credit company limited account!

Fullerton is similar to other Indian financial institutions like Navi, PayMe India, and LoanTap.

Fullerton India Personal Loans

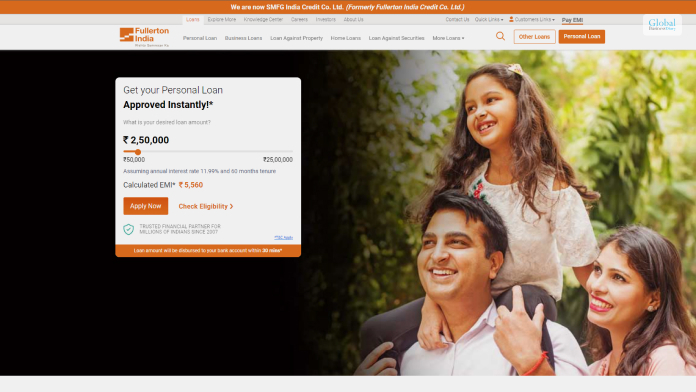

Fullerton India is widely renowned for providing personal loans to account holders at lower-than-average interest rates. As long as you are eligible for Fullerton India personal loans and you are a salaried employee, you will get such loans quickly.

All the procedures of this company are completely transparent to ensure that there are no hidden charges or secret terms and conditions in place. In addition, most of the Fullerton loan payment solutions can be customized by you to an extent.

| Maximum Loan Amount | Upto INR 25,00,000 |

| Repayment Tenure | Minimum 12 months, maximum 60 months |

| Interest Rate | Starting from 17% |

| Processing Fees | Upto 6% of the total loan amount |

| Prepayment Charges | Upto 7% of the total loan amount |

Why Should You Apply For Fullerton India Personal Loan?

Some of the benefits of applying for a Fullerton India personal loan are:

- The application process for this loan is 100% digital – no paperwork is required.

These personal loans are free of any collateral. - Repayment tenures for these personal loans are flexible.

- Since these are personal loans, the reasons for applying for this loan can be anything.

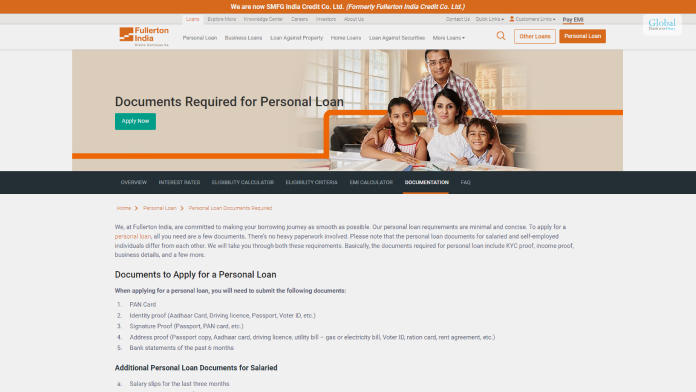

Required Documents

To apply for this loan, you need the following documents:

- A filled application form that is also digitally signed.

- Identity proof (should contain proof of your address, age, and citizenship)

- Salary Pay Slips for the last three months

- Bank statement for the last six months

- Form 16 Income Tax Returns report

- Other necessary financial statements and Proof of income (if you are self-employed)

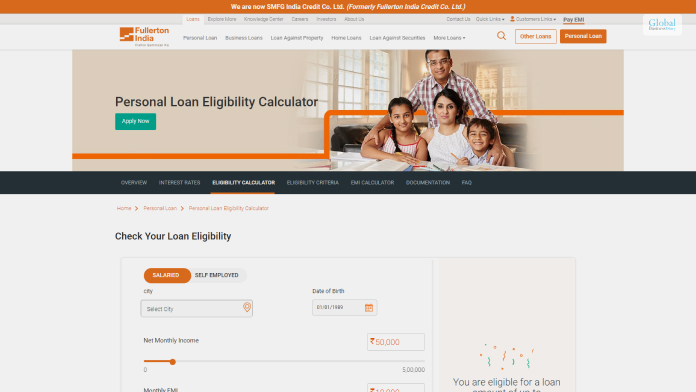

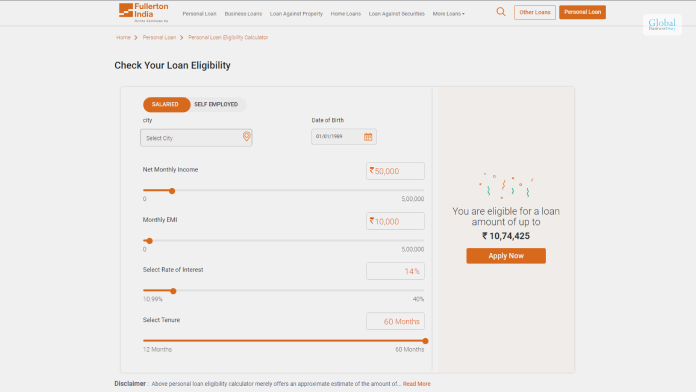

Personal Loan Eligibility Criteria

You will be eligible for Fullerton India personal loans by meeting these requirements:

| Age | Minimum 21, maximum 60 |

| Employment Status | Must be salaried or self-employed |

| Minimum Income | Minimum salary INR 25,000 |

| Credit Score | 750+ CIBIL score with a good credit history |

| Nationality | Indian |

| Work Experience | Minimum 1 year of work experience |

Fullerton India Business Loans

If you are an entrepreneur and you are in need of funds to expand your business, then contact Fullerton India. They have business loans for all types of businesses, both big and small.

Not only will these loans help you manage your business capital necessities, but they will also help you manage your capital needs for other purposes. This includes inventory purchases, workspace expansion, marketing, and any other additional payments.

| Maximum Loan Amount | Upto INR 50,00,000 |

| Repayment Tenure | Minimum 12 months, maximum 60 months |

| Interest Rate | Starting from 11.99% |

| Processing Fees | N/A |

| Prepayment Charges | N/A |

Why Should You Apply For Fullerton India Business Loan?

The primary benefits of applying for loans from Fullerton India home finance company limited are:

- All the loan facilities provided by the company are flexible since you have a loan repayment tenure of upto 48 months.

- Such business loans of upto INR 50 lakhs will be provided to you quickly within 24 hours after you apply.

- There are no collaterals for Fullerton business loans.

- You can access your loan account online pretty easily.

Required Documents

To apply for this loan, you will need these documents:

- A recently clicked photograph of you.

- Identity proof, like your PAN card.

- Address proof like your passport.

- Necessary bank statements

- Income Tax Report (ITR) files or GST Reports

- Income proof

- Business existence proof (like your business’s Certificate of Existence)

Business Loan Eligibility Criteria

You and your business will be eligible for these loans if you meet these requirements:

| Age | Minimum 25, maximum 65 |

| Business Status | Sole proprietorship or partnership |

| Minimum Turnover | Minimum INR 10,00,000 per annum, with INR 2,00,000 profit |

| Credit Score | 750+ CIBIL score with a good credit history |

| Nationality | Indian |

| Business Experience | Minimum 3 years of business life with profits in the last two years |

Other Types Of Fullerton India Loans

Apart from the two loans described above, which are the specialty of Fullerton India, they also provide other customizable loans like:

- Loan Against Property: If you have an immediate expense to clear out as soon as possible, then you can get a loan against your property as collateral instantly!

- Two-Wheeler Loans: These are short-term loans for purchasing your first two-wheeler!

- Home Loans: If you wish to purchase that dream house you have been eyeing for some time, you can apply for this loan!

- Commercial Vehicle Loans: If your business needs a commercial vehicle like trucks and other vehicles, you can apply for this loan!

How To Apply For Fullerton India Loans?

If you wish to apply for a Fullerton India loan, you have to follow a simple process, which I have described below:

- First, go to the Fullerton India official website.

- Here, click on the Apply Now button at the top of the page.

- Now, out of all the loan options, select the type of loan you wish to apply for.

- Depending on the type of loan you have chosen to apply for, an application form will open on your screen. Fill it up with all the required details.

- After you have filled up the application form, click on Next.

- An OTP will be sent to your registered email ID and phone number. Confirm them by following the on-screen procedures.

- Now, you must upload scanned copies of the necessary paper documents.

- After you are done uploading scanned copies, click on Submit.

After you hit the final Submit button, Fullerton India will get back to you if your loan is approved in the next 24 hours.

Conclusion

Fullerton India provides loans to people who are in dire need of them. All you need to do is meet their eligibility criteria and apply for their loans online! Plus, they provide many loans like personal loans, business loans, loans against property, two-wheeler loans, commercial vehicle loans, and home loans to apply for!

If you have any queries, please comment below!

Read Also:

Tags:

Recent

Time Matters: The Role of Early Hazard Detection in Industrial Safety

Jan 20, 2026

Hidden Ignition Risks in Industrial Environments

Jan 17, 2026

Critical Thinking Exercises in the Digital Age and Emotional Intelligence Integration

Jan 14, 2026

Why Strategic Partnerships Matter More Than Ever

Jan 13, 2026

Related Articles

Biggest Stock Market Crashes In The World History

The stock market is a triangle industry where a crash takes place when the market value drops in a series. It will be tough to provide a generalized definition of the stock market crash, but it may occur when the price drops more than natural. When the market price decreases and losses 10% from the current value, then people can consider this event as the “great depression.” In 1929, the marketing industry got 34%. A market crash takes place suddenly. But when it starts falling down, you may know that this is going to be cashed soon. Approximately 25% of workers lost their jobs due to this destruction in the market. If you are a stock market investor, the market crashing history can provide you with a primary imagination about the stock market. We will tell you how the whole industry flows to the veils in a short period of time. You will learn the history as well as the economy of the stock market world. It took 5 to 10 years naturally to get back to the previous stage. What Is The Stock Market Crash? As I have mentioned earlier, it is challenging to offer a generic definition of the stock market crash, but we can tell it is the rapid change of the price in the market. Before crashing a market, the stock market industry always reaches its peak, and from that point, it suddenly drops to the ground. Generally, stock market crashes happen in a short time period. For example, the price is normal today, and after nightfall, you may see the price drop down to 12%. This is how the market crashed. If you consider the whole system as a pyramid, you will see in a long time, the price is rising to the top and after reaching its catastrophic position, it suddenly drops. You, as an investor, can predict the market crash beforehand. When the price is increasing, you have to keep it in mind. However, it will go down all of a sudden. From the steady rising, it comes to the ultimate drop. This is a stock market crash. Also Read: Angel investors - Overview, pros and cons in 2021 Indications Of Stock Market Crash When you are a long-term investor, you have knowledge of the stock market. If you have ever followed, will see in a specific time, the market growth is going as a bounce. At this time, you can make an assumption about the market crash. There are more things about the market that you can follow. When you are in the stock market business, always stay alert and invest money after looking at all aspects. Therefore, let’s get started with the major indications. Drastic Speculations. Stagnant Market Value. Low-Interest Rates. Catastrophic Illusion. Slow Growth Rates. Exceptional Market value. These are all the things that you can follow through so that you can make an assumption. However, keep all these things in your mind and then step towards your goal. The Biggest Market Crashes In World History In world history, many times the market fails and for that thousands of people lose their jobs. You will be surprised to know that after the market crash in 1929, a total of 10% of people lost their jobs. Generally, there is always a balance between the economy and the stock market industry. When the stock market industry gets injured, it affects the economy on a large scale. Many times, many incidental cases happen in the stock market industry. For the time being, let’s get up to date with the large world history of stock market crashes. Black Tuesday Of 1929 One of the major stock market crashes began on 24th October 1929. Although there are some confusions about this theory. Some authorities have opined that the fall began on 18th October. The same condition went on till 29th October. Mass hysteria was created when a total of 12,894,650 shares were traded. When the price started falling, people tried to get their money out, and for this reason, chaos was also created. The market first opened with 11% lower than the average. At this time also, people never think that the market will crash. This happened in the next few days when it got more decreased. Before starting the black day, the market reached its last peak position on 3 September. The situation was not like the previous devastation. Though later it became like that, and mass curiosity was also one of the main reasons. Black Monday Of 1987 In the year 1987, the market started decreasing. After then, this became devastating for the stock market investors. At that point in time, Dow jones’s market value got decreased up to 22%. Still, now this situation is remarked as one of the major incidents in the world history of the stock market. From 19th October, the market value started decreasing, and it reached the lowest stage in November. The market lost its stock, and the market value also decreased 20% from the average value. It is said that there were many investors that could manage themselves to get out their stocks. Whenever this type of incident takes place, you may see the mass hysteria that makes the incident more ridiculous. The same thing happened in the 1987 market loss. This grand loss took years to get the scenario back. The professional marketers have said later that this incident took place because of the computing trading and as well as for the middle investors. Many of the investors do not even accept these things as the prime reasons, though. It never drops off, only for computing trading and for the trade deficit. Dot-Com Bubble Of 1999-2000 This dot-com bubble incident took place almost thirty years ago. This is why it is far away from the other types of incidents. You may know this incident from the NASDAQ composite index. Many of the investors inculpated the online market agencies that created chaos among people. The technology-dominated services created mishaps, and that probably deals the case to the deeper loss. The surge was in 1995 approximately 100 that had increased upto 500 in 2000. From this point in time, the bubble started bursting. Behind the screen, there was a large lake that later came in front. The overvalued stock was also one of the main reasons for this dot-com bubble case—this time. People just hold their stocks. And when the market value decreased, they all started selling, and the mishap took place. If they sell the stock at the peak point, then may this incident never happen. This market value remained like that for a long time. It took years to get back to the previous stage of the stock market. The Stock market is sensitive, and that is why people need to manipulate the channel properly. When any mishap happens, the whole chain breaks off. Stock Market Crash Due To Covid-19 It is the most current stock market crash that happened, and even its effect is still going on the economy. From the country-based loss, it spread to the international loss. All countries got economic harm from this current market crash. At the present time, there has been an increase in the number of digital investors that are paying in this market chain through online facilities. From February onwards, the market started crashing, and that decreased upto 11% to 13% on average. You will be surprised to know from 1987 to the current time; it is the major drop in the history of the stock market. Before this, the situation never happened like this. The market plunged deeper day by day. Even in the present situation in 2021, the same thing is going on. The prior amounts and the investment were taken away, but the middle watts remained locked. In the stock market, people spend millions of dollars that the authority has driven out. But still, the mediocre investor's money got stuck. Due to the pandemic, this marketing scenario is a bit different from other creases. The prior reason behind this market falls in the unknowingness of people. The business investors and the dealers had no idea about the future going situation, and that is why they took back their stocks. This time, the market goes to the grand fall in a different manner than has a prior reason to fall back. The Dow declined 9.99% in March. Trillions of dollars are still stuck in the market. But it has no straightforward declaration of the market. We hope this situation will also be overcome at the end of the pandemic situation. Effects Of Stock Market Crashes When the stock market is running well, you will see the economy is also growing. In major cases, when the stock market gets stuck, the economy of the country also gets hampered. On the other hand, the stock market is a large industry where millions of people are investing; some are working on the online trading market. Those who are working on the stock market can lose their jobs when the whole industry breaks down. When you invest in the stock market, you have to keep in mind you are going to get a profit from the investment. If the market crashes, then you will never get your profit. The price drop means, in the literary sense the less revenue. And when the revenue is decreased, the investor will receive a bad impact. Through this, people get great depression. The depression situation took place in the previous years. You may take a look at these times. Also Read: How To Make Money Fast - 5 Strategy To Follow In 2021 Frequently Asked Questions (FAQs) You may have questions regarding stock market investment. So, let's get you covered with all aspects as well. Firstly, let’s tell you, when you are thinking of the stock market investment, you have to remove the negative thoughts. Now, take a look. Q1. Is It Worth Investing In The Stock market? Ans. Investment in the stock market is a good decision. If you are new in the industry, you may face difficulties. The stock market has an option of earning double the amount from the investment. Experienced investors generally get more profit from their investment. Don’t worry; you will get the same opportunity after learning more things about the stock market. Q2. Which App Is Best For The Stock Market? Ans. You can use NSE mobile software for trading. Except that you can go through the NDTV profit, IIFL markets, etc. You can also buy stocks online with trusted brands like eToro. It's easy to learn how to buy stocks on eToro by simply following their guides. Also Read: 10 Best Investment Apps For 2021 Q3. Is The Stock Market Safe To Invest In? Ans. It is difficult to answer properly. We can tell you that you have to be aware of the market when you will pay. So, start investing today and wait for the profit. If you find difficulties, you can go through the solutions as well. But never ever stop dreaming about getting the best profits. Q4. What Is The Best Stock Market To Invest In For Beginners? Ans. There are many investment options. Worldwide, there are many companies finding investors. You append your money there. You can spend money on Amazon, Alphabet, Apple, Facebook, Mastercard, etc. however, you have to start investing from today. The Bottom Lines These are all the relevant factors that you need to know before starting an investment in the stock market. Whenever you start investing, make sure that you will be serious about the market factors. The price can increase as well as decrease, so stay aware of the fact. In addition, we will tell you, try to think of the best things not following the backlogs. When you are doing a business, there is always a chance of loss, but you have to focus on the positive things. Only then will you be able to get the best fruit from trading. Read More: How to start a business in 2021 - Best Business Strategies Top 10 Successful Serial Entrepreneur Of All Time - 2021 Updates Top 10 Best B2B Marketing Strategies For The Entrepreneurs In 2021

Sep 13, 2021

Debt-Service Coverage Ratio (DSCR): Meaning, Uses, Calculation, And More

With the help of the debt service coverage ratio (DSCR), one can calculate the ability of a company to manage its current debt obligations by making use of the available resources. By calculating the ratio, the stakeholders of the company can evaluate the financial state of the company. This can give an idea of whether the company is capable enough to repay its outstanding short-term and long-term debts. In this article, you will learn some of the general details about the debt service coverage ratio and the formula to calculate this ratio. Apart from that, you will also get an idea of how to calculate this ratio in a business situation, that is, having a knowledge of how to work. Finally, we will check the pros and cons of the debt service coverage ratio. Hence, to learn more, read on through to the end of the article. What Is The Debt Service Coverage Ratio (DSCR)? According to Wall Street Mojo, “Debt Service Coverage Ratio (DSCR) calculates the ability of companies to manage their current debt obligations using the available resources. The computation of this ratio allows stakeholders to assess the company’s financial state and check if it is capable enough to repay its outstanding long-term and short-term dues.” Basically, the debt service coverage ratio helps you to measure the available cash flow of the company to pay its current debt obligations. By calculating this ratio, investors and lenders can determine whether the company has enough income to pay off its debts or not. You can calculate this ratio once you divide the net operating income of the company by debt service, including principal and interest. When you find out the debt service coverage ratio of a company, you will be in a better position to decide whether to invest in a company or not. Or, if you are a lender, you will be able to decide whether to approve a particular company’s loan or not, provided the company’s current availability of resources. The higher the ratio for the company, the better the chances are for the company to get more loans, credits, and investments. Read More: Entrepreneur : Who Coined The Term ‘Entrepreneur’? What Is The Formula Of Debt Service Coverage Ratio (DSCR)? By determining the debt service coverage ratio of a company, you will be able to learn the financial health of the company. If the company has a lower ratio, it means that the company has a higher chance of defaulting on payments. According to Indeed.com, “To understand a company's financial health, a financial analyst compares it with other companies operating in the same industry. Comparing the DSCR ratio of an airline company, which uses larger debts, with a software company, which uses minimum debt and more equity financing, is inappropriate because both companies have different debt structures.” Here is the formula for the debt service coverage ratio (DSCR): Debt Service Coverage Ratio = Net Operating Income / Total Debt Service Here, Net Operating Income = Total Revenue - Certain Operating Expenses and Total Debt Service = Interest + Principal Payments + Lease Payments How Does The DSCR Work And What Are Its Uses? According to Investopedia, “The debt-service coverage ratio is a widely used indicator of a company's financial health, especially those who are highly leveraged with debt. Debt service refers to the cash needed to pay the required principal and interest of a loan during a given period. The ratio compares a company's total debt obligations to its operating income.” For a company to get loans, there is a minimum level the company must be able to match. Various lenders, stakeholders, and partners target the debt service coverage ratio metrics of the company, as well as terms and minimums related to it, before approving a loan. When it comes to corporate finance, the debt service coverage ratio of a company shows its ability to pay its debt. This value is really helpful for lenders and investors. On the other hand, when it comes to personal finance, the debt service coverage ratio helps the bank to find out its interest rate. In typical cases, banks, lenders, and financial institutions prefer a higher debt service coverage ratio for a company. Having a higher DSCR shows that the company has sufficient funds to pay off its debt obligations and the company can make payments faster. Pros And Cons Of The Debt Service Coverage Ratio (DSCR) The following are some of the major pros and cons of the debt service coverage ratio for determining the loan payoff ability of a company: Pros Of Debt Service Coverage Ratio Here are some of the major pros of the debt service coverage ratio formula: Monthly calculation of the debt service coverage ratio helps a company evaluate its average trend over some time and predict future ratios. It helps in budgeting and strategic planning. It helps in comparing and assessing the company in regard to its competitors. It helps to better assess the long-term financial health of the company. A truer representation of the operations of a company, as compared to other ratios. Cons Of Debt Service Coverage Ratio Here are a few cons of the debt service coverage ratio formula: Using operating income to calculate the debt service coverage ratio can overstate the company’s income since not all expenses are shown. With accrual-based accounting guidance, the debt service coverage ratio is partially calculated. Read More: What Is a Franchise, And How Does It Work? – Examples, Benefits & More Bottom Line Hope this article was helpful for you in getting a better idea of how the debt service coverage ratio (DSCR) works and how to calculate it using the formula. It basically shows you whether a given company has enough income or cash flow to pay its current debt obligations. This can give an idea to lenders and investors about a company’s ability to pay back loans. You can also find out the debt service coverage ratio by calculating the net operating income of the company and comparing it with the debt service, including principal and interest. Do you have any more suggestions on how to use this ratio to evaluate a business? Share your ideas and opinions with us in the comments section below. Read Also: Contribution Margin: What Is It, Overview, Examples, And More Business Risks – How To Identify, Manage, And Reduce Them? The Best Risk Mitigation Techniques For Your Business

Sep 29, 2023

LazyPay: Information, Eligibility Criteria, Interest Rates, Review & More

LazyPay is a loan app that claims to offer instant personal loans to salaried professionals and self-employed individuals. The LazyPay app is run by PayU Finance and offers borrowers access to credit and pay later options. The credit options from LazyPay range from ₹10,000 to ₹5,00,000. Hence, to know more about LazyPay, consider reading through to the end of the article. In this article, we will mainly give you an overview and a review of LazyPay. Furthermore, we will also give you details about the loan options that you will get once you use LazyPay. Later on, you will also learn about the loan eligibility of LazyPay and various other factors. Therefore, to get fully informed, read the upcoming sections of the article. What Is LazyPay? LazyPay is an app that offers two types of services – namely, pay later options, where you can shop now and pay late, and also personal loan options. With pay-later services, LazyPay offers you to settle your amounts every fifteen days. The auto-repayment feature with LazyPay’s pay later deducts the amount every fifteen days. On the other hand, LazyPay also offers instant personal loans. You can borrow personal loans up to 5 lakhs INR, depending on your credit score and various factors, including age, salary, job, etc. The loan app claims to give you Flexible EMI options, fast application of loans, and quick approvals of those loans. Is LazyPay Safe? With various loan options and pay later related information on their official website, LazyPay seems legit to us. However, due to a variety of complaints from loan borrowers and other customers, LazyPay does not have a good review on the Internet. Even there are many complaints against LazyPay in the Indian Consumer Forum. The Ministry of Electronics and Information Technology of India has blocked LazyPay on various platforms. They are charged with the misuse of the data of the consumer, which is considered important for national security and integrity. According to TechCrunch.com, “The LazyPay website has been blocked by several internet service providers in the country. A message on the Prosus-owned website says the action was taken in compliance with the IT Ministry’s order.” LazyPay Payment – What Does It Offer? Loan AspectsWhat LazyPay offers you?Loan Amount₹ 10,000 - ₹ 5,00,000Loan Tenure90 days to 720 daysRate of interest on loans0.05% per dayLoan Processing fee2% of the loan amountLoan review timeDepending upon the amount of the loan (may take from 5 minutes to 7 days)Late payment of the loan- Application of Penalties every day based on the overdue loan- Updating the credit score as default with credit rating agencies (CIBIL, CRIF High Mark, etc.)Loan RepaymentLoan repayment is made automatically from the provided bank details as per the approved schedule. Once you open the app, you will get a variety of loan options to choose from from different LazyPay Merchants available to offer you loans through the app. However, different merchants have different viewing mechanisms, and depending on the merchant you choose, you can get your loan accordingly. LazyPay Loan App – Eligibility The following is the major eligibility-related information that you will need to know before you avail of loans from LazyPay: Loan RequirementsEligibilityAge of the borrower22 to 55 years oldLazyPay credit scoreDepends on the type of loan applied for.Type of EmploymentSalaried professionals and self-employed individuals.Minimum monthly incomeAny monthly income is eligible to take loansWork ExperienceWork experience requirements change with the amount of the loan demanded. Required Documents1. Salaried Employees- Need to fill out KYC- Verification of KYC- Need to submit bank details- Bank account number & IFSC- Net banking required for auto-repayment 2. Self-Employed Individuals- PAN card required- Address proof (Voter ID or Passport)- Aadhar Card- Bank account number & IFSC- Net banking required for auto-repayment How To Delete LazyPay Account? After LazyPay Bill Payment in LazyPay pays later, you will have the option to delete your LazyPay card permanently. According to LazyPay, “A permanent block deletes your card details and cannot be reversed. Keep in mind that this step will deactivate your virtual card number as well. If you suspect your card or card details have been stolen or compromised in any way, we urge you to permanently block your card as soon as possible.” Go to your LazyPay account, and find the “Manage Card” section. Scroll down, and you will see an option that lets you permanently delete it. LazyPay Customer Care If you are finding problems with any of the LazyPay services, be it pay later or instant personal loan, you can call LazyPay Customer Care no at +91 8069081111 from 9 am to 9 pm any day. You can also go to this page to get help with various issues: https://lazypay.in/needhelp. LazyPay Reviews Praveenthomascook: Image Source Krishnasingadi: Image Source Merrview: Image Source Summing Up Hope this article was helpful for you to get a better idea of the services offered by LazyPay, and various details related to eligibility for loans and pay later options in the platform. Regarding safety, hope you have enough information from the reviews of the customers, and also the safety issues pointed out by the Government of India. We would recommend you be careful and get the information fully before you borrow loans from LazyPay. Do you know of any people facing problems with LazyPay? Share with us some information about that in the comments section. Read Also About: How To Get Personal Loan On Bajaj Markets Speed Up Your Funding: A Quick Guide To Business Loans What You Should Know Before Committing To A Cash Buyer

Apr 19, 2023

Chime Financials: Essential Things To Know About It

Chime Financials is now one of the leading Fintech companies in the world to deliver quality banking services. Most of the time, its services are helpful, easy, and free to use. You need to find the best solutions that can assist you in reaching your goals with ease. The best part of Chime Financial is that it tries to bridge the gap between what is good for banks and what is good for consumers. Approach of Chime Financials is to make a profit through overall growth, not through individual profitability. Today, Chime Financial is one of the most loved banking apps to download by apps in America. They are a financial technology company that partners with some of the country's renowned national banks. Although they are one of the best Fintech Companies to know more about them. What Are The Benefits Of Chime Financial Services? There are several crucial benefits of Chime Financial services that you must know at your end while attaining your requirements. You need to know the details to have a better idea of it. Without knowing the facts, things can become critical for you. 1. No Hidden Fees Chime is known for its fee-free banking. There are no monthly fees, overdraft fees, foreign transaction fees, or minimum balance requirements. You need to take care of the realities that can assist you in reaching your needs with ease. Although its services are not absolutely free of cost, there are some charges you need to pay to get quality services. It will be better for you if you do proper research from your end before seeking their Fintech services. Additionally, do not forget to keep your priorities in mind. 2. Early Direct Deposit Is Possible Here Chime allows you to get paid up to two days early with direct deposit, which can help you access your money sooner. You can get the easy access to your money. This can help you in attaining your opportunities with ease. Getting direct access to your money without any third-party hindrances will be possible for you with help of this app. Ensure that you know the facts well when you want to make use of this app. The evolution of Fintech starts from here. 3. Ensures Automatic Savings Chime offers an automatic savings feature that rounds up your money-transferring process to the closest dollar and saves the spare change for you. It can provide you the option to put your focus on saving money. Thus, you can seek the help of this app to get things done in perfect order. Ensure that you follow the right choices from your endpoints that can make things easier for you. Thus, it can help you in reaching your objectives. 4. Fee Free Overdraft Chime offers an option known as SpotMe that allows you to overdraft your account up to a certain limit without any fees. A fee-free overdraft can make it easier for you to attain your goals with ease. Try to follow the right choices from your endpoints that can make it easier for you to attain your requirements. 5. High Yield Savings Account Chime offers a high-yield savings account with competitive interest rates to help you grow your savings faster. Once you make use of the high-yield savings account, things can become easier for you in all possible manner. Ensure that you know the process that can create a long-term impact in the long run. Select the best global fintech companies that can boost your earnings chances. 6. Simple User Friendly Interface Chime's app and website are designed to be user-friendly, making it easy to manage your finances with complete ease. Plan out the solutions that can assist you in reaching your objectives with absolute ease. The simple, user-friendly interface can make things lucid for you to attain your goals with ease. 7. Security Features Chime uses encryption and other security measures to protect your personal and financial information. Try to keep the security features in place that can assist you in meeting your needs with ease. Security features can make things work well in your favor within a specific time frame. Ensure that you follow the correct solutions from your counterpart. Chime Financial takes care of your secure transaction to keep things in proper shape. What Are The Core Services Of Chime Financials? There are several core services of Chime Financials that you must know from your end before seeking it from your counterpart. Some of the core services of Chime financials that you should know from your end. 1. Checking Accounts Chime offers fee-free checking accounts with no minimum balance requirements. There are no monthly fees and access to a network of over 38,000 fee-free ATMs. You must ensure that you maintain the correct solution from your endpoints while seeking Chime Financials's services. Try out the best options that can assist you in getting the best solutions within a specific time frame. 2. Maintaining Savings Accounts Chime provides high-yield savings accounts with competitive interest rates to help customers grow their savings faster. Although Chime Financials offers the scope for maintaining high-yielding savings accounts, things can become easier for you. Once you have the correct savings account in place, things can become easier for you to reach your goals. 3. Debit Cards Chime offers a Visa debit card that can be used for purchases online and in stores to withdraw cash from ATMs. You can seek these types of facilities from the Chime financials to meet your financial goals with ease. However, you need to follow the process that can make things easier for you to attain your options with ease. Try to make use of the debit cards that can assist you in meeting your needs with ease. 4. Direct Deposit Chime provides users the option to set up direct deposit for their paychecks, enabling them to get paid up to two days early. Direct deposits can assist you in meeting your financial needs with complete clarity. You will be paid two days early if you make the direct deposits of the fund and the money from your end. It can become the Future of Money. 5. Use Of Mobile Banking App Chime's mobile app allows customers to manage their accounts, deposit checks, transfer money, pay bills, and more. You can do it all from your mobile devices. Once you make use of the best mobile banking apps, things can become easier for you in the long run. Effective processes can boost the chances of your mobile banking earnings to a greater level. 6. Ensures Automatic Savings Chime Financials offers an automatic savings feature that rounds up transactions to the nearest dollar and saves the spare change. Plan out the best options that can ensure automatic savings for your finances. Ensure that you follow the best process that can help you multiply your savings in the correct order. Without knowing the right techniques, things can become more complex for you in the long run. Their services are similar to the Ant group. 7. Fee Free Overdraft Chime's SpotMe feature allows customers to overdraft their accounts up to a certain limit without incurring fees. Ensure that you make things work in perfect order while attaining your needs and requirements with ease. Follow the right process that can assist you in meeting your needs with ease. Missions Of Chime Financials There are certain core missions of Chime financials that you must know from your end while you want to seek their services. Some of their core missions that you must know from your end are as follows:- 1. Fee Free Banking Chime aims to eliminate the traditional fees associated with banking, such as monthly fees, overdraft fees, and foreign transaction fees. Thus, it helps make banking more affordable for everyone. Once you follow the right process, things can become easier for you to reach your goals with complete ease. Without the correct application process, things can turn worse for you in the long run. 2. Early Access To Paychecks Chime's mission includes providing customers with early access to their paychecks. Thus allowing them to access their money sooner and manage their finances more effectively. They are planning to get access to the paychecks. That can make it easier for you to get things done in the best way. Without knowing the facts, things can turn worse for you in the long run. Try to keep things in perfect order while attaining your requirements with complete clarity. 3. Financial Education Chime Financials is committed to helping its customers improve their financial literacy and make more informed decisions about their money. The company provides educational resources and tools to help customers achieve their financial goals. However, without proper financial education, you cannot prosper in the long run. Once you follow the correct process, things can become easier for you in the long run. Try to make your selection on the correct end while attaining your needs with ease. 4. Inclusion & Accessibility Chime's mission is to make banking more inclusive and accessible to everyone. Thus including those who may have been underserved or overlooked by traditional banks. You need to find out the best options that can make things easier for you to reach your goals with ease. Once you make use of the inclusion of Chime Financials, things can become easier for you to attain your goals with ease. Ensure that you make the correct choices from your counterpart. You must be well aware of the facts that can help you to manage your finances with ease. 5. Simplicity & Convenience It strives to make banking simpler and more convenient for its customers by offering a user-friendly mobile app. Thus, it is an easy-to-understand product and offers helpful customer support. Ensure that you make the right choices from your endpoints when you want to make things happen in your favor. Chime Financial's ultimate goal is to offer you the best solutions at a reasonable rate. How Do You Open An Account With Chime Online? There are certain steps you need to follow when you want to open your account in Chime online. Some of the key factors that you must know at your end while attaining your requirements with absolute ease. Let’s find out some of the key factors that you must know from your end while attaining your needs with ease. Go to the Chime website (www.chime.com) using a web browser on your computer or mobile device. Look for the "Get Started" or "Open an Account" button on the homepage and click on it to begin the account opening process. You will be asked to provide some basic information, such as your name, address, date of birth, and Social Security number. This information is used to verify your identity. Create a username and password that you will use to log in to your Chime account. Make sure to choose a strong password to protect your account. Read through Chime's terms and conditions, privacy policy, and other disclosures, and agree to them to proceed with opening your account. Follow the on-screen instructions to set up your account, including choosing the type of account you want (checking, savings, or both) and funding your account. You may be asked to verify your identity using a photo ID or other documentation. Follow the instructions provided by Chime to complete this step. Once your account is approved, you will receive a Chime Visa debit card in the mail, which you can use to access your funds. To manage your account and access Chime's features, download the Chime mobile app from the App Store (for iOS devices) or Google Play Store (for Android). Final Take Away Hence, if you want to get the right solutions to your problems, then the mentioned factors can be of great help. Chime financials can make things easier for you if you want to seek assistance from the best Fintech company. You can share your opinions and views in the comment box. This will help us to know your take on this matter. Once you follow the correct solution, things can become easier for you in the long run. Chime's mission is centered around providing a better banking experience for its customers, one that is more affordable, inclusive, and empowering. You need to get through the best process from your counterpart. #Disclaimer: The information provided on this blog is for educational and informational purposes only and should not be construed as financial advice. I am not a licensed financial advisor. Any investment decision you make is at your own risk, and you should consult with a qualified financial advisor before making any investment decisions. This site may contain affiliate links, and I may earn a commission at no additional cost to you. Continue Reading: Revolut Makes Your Financial Management Journey Easy Stripe A Leading Fintech Company: Essential Things To Know About It 5 Myths About Digital Selling In 2024

Mar 06, 2024